Do Fundamentals Have Any Role To Play In Driving Getty Realty Corp.'s (NYSE:GTY) Stock Up Recently?

Getty Realty's (NYSE:GTY) stock is up by 2.1% over the past three months. Given that stock prices are usually aligned with a company's financial performance in the long-term, we decided to investigate if the company's decent financials had a hand to play in the recent price move. In this article, we decided to focus on Getty Realty's ROE.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

Check out our latest analysis for Getty Realty

How Do You Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Getty Realty is:

8.0% = US$49m ÷ US$618m (Based on the trailing twelve months to September 2020).

The 'return' is the amount earned after tax over the last twelve months. One way to conceptualize this is that for each $1 of shareholders' capital it has, the company made $0.08 in profit.

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

Getty Realty's Earnings Growth And 8.0% ROE

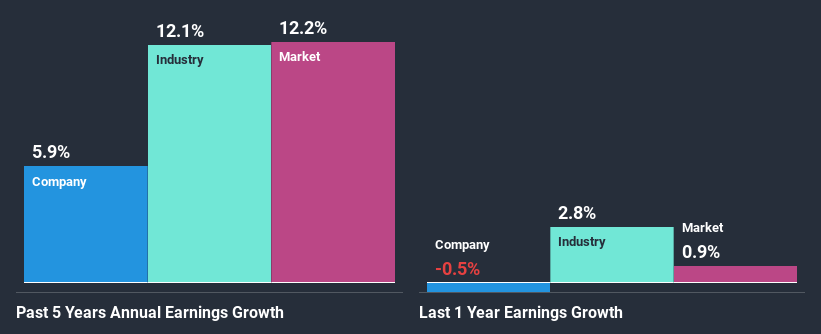

On the face of it, Getty Realty's ROE is not much to talk about. Although a closer study shows that the company's ROE is higher than the industry average of 5.6% which we definitely can't overlook. This certainly adds some context to Getty Realty's moderate 5.9% net income growth seen over the past five years. Bear in mind, the company does have a moderately low ROE. It is just that the industry ROE is lower. Therefore, the growth in earnings could also be the result of other factors. E.g the company has a low payout ratio or could belong to a high growth industry.

Next, on comparing with the industry net income growth, we found that Getty Realty's reported growth was lower than the industry growth of 12% in the same period, which is not something we like to see.

Earnings growth is an important metric to consider when valuing a stock. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. Is Getty Realty fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Getty Realty Making Efficient Use Of Its Profits?

Getty Realty has a high three-year median payout ratio of 71%. This means that it has only 29% of its income left to reinvest into its business. However, it's not unusual to see a REIT with such a high payout ratio mainly due to statutory requirements. In spite of this, the company was able to grow its earnings by a fair bit, as we saw above.

Moreover, Getty Realty is determined to keep sharing its profits with shareholders which we infer from its long history of paying a dividend for at least ten years. Based on the latest analysts' estimates, we found that the company's future payout ratio over the next three years is expected to hold steady at 80%. Therefore, the company's future ROE is also not expected to change by much with analysts predicting an ROE of 9.5%.

Conclusion

Overall, we feel that Getty Realty certainly does have some positive factors to consider. True, the company has posted a respectable growth in earnings. However, the earnings growth number could have been even higher, had the company been reinvesting more of its earnings and paying out less dividends. With that said, the latest industry analyst forecasts reveal that the company's earnings are expected to accelerate. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.