Fundamentals Support Low Volatility, Tight Spreads (Capital Market Research) (Weekly Market Outlook)

WEEKLY

MARKET OUTLOOK

APRIL 29, 2021

CAPI TAL MARKETS RESEARCH

Moody’s Analytics markets and distributes all Moody’s Capital Markets Research, Inc. materials. Moody’s Capital Markets Research, Inc. is a subsidiary of Moody’s Corporation. Moody’s

Analytics does not provide investment advisory services or products. For further detail, please see the last page.

Fundamentals Support Low Volatility, Tight

Spreads

Credit Markets Review and Outlook

by Ryan Sweet

»

FULL STORY PAGE 2

The Week Ahead

We preview economic reports and forecasts from the U.S. , Europe and Asia/Pacific regions.

»

FULL STORY PAGE 5

The Long View

Full updated stories and

key credit market metrics:

High-yield corporate bond

issuance is on track to

have another strong

month.

»

FULL STORY PAGE 10

Ratings Round-Up

Upgrades for 10 of 11 U.S. Changes; Europe Activity Shows Improvement

»

FULL STORY PAGE 13

Market Data

Credit spreads, CDS movers, issuance.

»

FULL STORY PAGE 16

Moody’s Capital Markets Research

recent publications

Links to commentaries on: Leverage, stimulus, inflation, GDP, Treasury yields, rising prices,

core profits, yield spreads, virus, Congress , misery, issuance boom, default rate, volatility,

credit quality, record savings rates, demographic change, high tech, complacency, Fed

intervention, speculation, risk, credit stress, optimism, corporate credit, VIX.

»

FULL STORY PAGE 20

Credit

Spreads

Investment Grade: Year-end 2021’s average investment grade

bond spread may be near its recent 97 basis points. High Yield:

Even with a booming economy, a composite high-yield spread

could be slightly higher than its recent 326 bp by year-end

2021.

Defaults

US HY default rate: According to Moody's Investors Service,

the U.S. ' trailing 12-month high-yield default rate jumped

from March 2020’s 4.9% to March 2021’s 7.5% but may

average only 4.1% for 2021’s final quarter.

Issuance

For 2019’s

offerings of US$-denominated corporate bonds,

IG bond issuance rose 2.6% to $1.309 trillion , while high-

yield bond issuance surged by 58% to $440 billion .

In 2020, US$-denominated corporate bond issuance soared

54% for IG to a record $2.012 trillion , while high-yield

advanced 30% to a record-high $570 billion .

For 2021, US$-denominated corporate bond offerings may

decline 16% (to $1.684 trillion ) for IG and increase 7% (to

$607 billion ) for high-yield, where both forecasts top their

respective annual averages for the five years ended 2020 of

$1.494 trillion for IG and $410 billion for high-yield.

Moody’s

Analytics Research

Contributors:

Lead Author

Ryan Sweet

Senior Director-Economic Research

610-235-5213

Ryan.Sweet@Moodys.com

Asia-Pacific

Katrina Ell

Economist

Shahana Mukherjee

Economist

Europe

Ross Cioffi

Economist

U.S.

Adam Kamins

Economist

Michael Ferlez

Economist

Ryan Kelly

Data Specialist

Editor

Reid Kanaley

Click here for

Moody’s Credit

Outlook, our sister publication

containing Moody’s rating

agency analysis of recent news

events, summaries of recent

rating changes, and summaries

of recent research.

Contact:

CAPI TAL MARKETS RESEARCH

2

APRIL 29, 2021

CAPITAL MARKETS RESEARCH / MARKET OUTLOOK / MOODYS.COM

Credit Markets

Review and Outlook

Credit Markets Review and Outlook

By Ryan Sweet, Senior Director-Economic Research

Fundamentals Support Low Volatility, Tight Spreads

Tight U.S. high-yield corporate bond spreads could stick around until the economy begins to cool or volatility

in the equity market increases. The VIX is currently trading around 18, below its historical average of 19.5 and

below the 20 to 30 range it was trading in since the second half of last year. Volatility could return as a debt-

ceiling fight could brew this summer, potential for the Fed altering its forward guidance around its monthly

asset purchases, and proposed capital gains tax hikes, which could ding the stock market later this year.

For now, volatility isn’t out of line with economic fundamentals. To estimate the level of the VIX consistent

with fundamentals, we model the monthly average of the VIX using an ordinary least squares regression.

Independent variables include the GDP-weighted average of the ISM surveys, the TED spread, a dummy

variable for recessions, and U.S. economic policy uncertainty. The TED spread is the difference between the

three-month T-bill rate and the three-month Libor.

The results were in line with our a priori, as all the coefficients had the expected sign. All were statistically

significant and had an adjusted R-squared of 0.6. The regression was re-estimated, but we replaced U.S.

economic policy uncertainty with global policy uncertainty. The assumption is that uncertainty abroad would

affect volatility in U.S. equity markets. However, the results showed this explained less of the variation in the

VIX than U.S. policy uncertainty.

Overall, the VIX isn’t out of line with fundamentals, thus the tight spreads for high-yield corporate bonds seem

reasonable. To highlight this, we modeled the high-yield corporate bond spread in terms of the average

expected default frequency metric of U.S. /Canadian high-yield issuers, the VIX, and the moving three-month

average of the Chicago Fed’s national activity index. This suggests that the high-yield corporate bond spread is

a little too narrow, but nothing that raises a red flag.

High-yield corporate bond issuance is on track to have another strong month. Also, returns in high-yield have

been solid. Year-to-date returns by quality distribution show that among the biggest gains are in high-yield.

For example, year-to-date returns for Caa is 4.7% while Ca is over 15%.

Q1 GDP Is Even Better than It Appears

U.S. real

rose 6.4% at an annualized rate in the first quarter, a little lighter than our forecast for a 7.1%

gain. The economy is about to close the output gap, a small milestone on the road to fully recovering from the

recession. The output gap, or the difference between actual GDP and potential output as a share of GDP, was -

2.5% in the first quarter of this year. The output gap could close in the next quarter or two. This is a rapid

closing of the output gap, which was -10% in the teeth of the recession. Aggressive fiscal and monetary policy

stimulus played a critical role.

CAPI TAL MARKETS RESEARCH

3

APRIL 29, 2021

CAPITAL MARKETS RESEARCH / MARKET OUTLOOK / MOODYS.COM

Credit Markets

Review and Outlook

Fiscal stimulus impact is all over first quarter GDP. Real consumer spending jumped 10.7% at an annualized

rate, compared with the 2.3% gain in the prior three months. This is among the largest increases since the

1960s. The strength in consumer spending isn’t surprising because of the 61.3% annualized gain in disposable

income in the first quarter. Disposable income got a big boost from government transfer payments, including

economic impact payments that boosted incomes by $1.929 trillion at an annualized rate. Expanded

unemployment programs also added $275 billion at an annualized rate.

Though economic impact payments will fade, consumers are sitting on an enormous amount of savings that

will decline as restrictions continue to be relaxed. The amount of saving that households have done since the

pandemic began, using the Bureau of Economic Analysis measure of saving, compared with what would have

been saved at pre-pandemic saving rates, suggests excess saving of about $1.6 trillion as of the end of last year

and probably well over $2 trillion today given two rounds of stimulus checks distributed this year. We will

update our estimate of excess savings Friday after the release of March personal income.

Real business fixed investment increased 10.1% at an annualized rate after rising 18.6% in the fourth quarter of

last year. Nonresidential structures investment continues to decline, having fallen each quarter since the

recession began. Real equipment spending was up 16.7% at an annualized rate in the first quarter, a solid gain

even though it trails the 25.4% in the final three months of last year. There was good news on the future

productivity growth front as intellectual property investment rose 10.1% at an annualized rate, exceeding 10%

for the second consecutive quarter.

Still, it will take time to reap all the benefits. A Granger causality test found evidence that growth in

intellectual property causes changes in productivity with a 16-quarter lag. Therefore, if the relationship

between investment in intellectual property and productivity holds, productivity growth should reaccelerate

over the next couple of years.

Real residential investment increased 10.8% at an annualized rate. Homebuilders haven’t been able to keep up

with demand. Demand should remain strong as more millennials are moving into their first-time homebuyer

years.

Inventories subtracted 2.6 percentage points from first quarter GDP. Some of this is likely attributed to supply

chain disruptions and the global semiconductor shortage. As this fades, businesses will need to replenish

inventories, which will be a positive for manufacturing and GDP.

The monetary policy implications of first-quarter GDP are not significant. The Fed continues to stress that the

economy is still far away from its objectives. We may need to raise our forecast for GDP growth this year. The

April baseline had GDP rising 6.4% this year but could exceed our forecast given the amount of excess savings

and need to replenish inventories GDP.

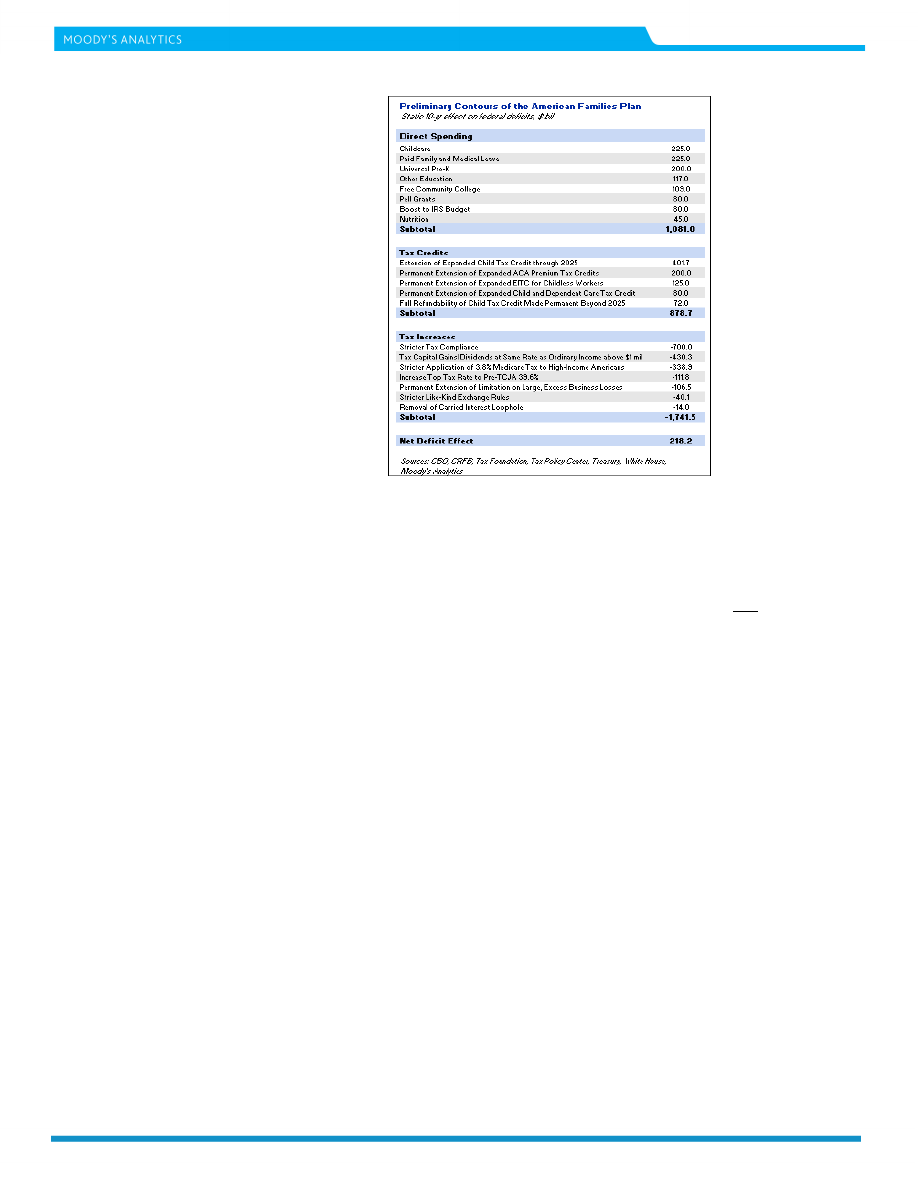

First Take on the American Families Plan

We have come up with a preliminary cost estimate of the AFP, based on the fact sheet provided by the White

House and other sources.

CAPI TAL MARKETS RESEARCH

4

APRIL 29, 2021

CAPITAL MARKETS RESEARCH / MARKET OUTLOOK / MOODYS.COM

Credit Markets

Review and Outlook

The AFP contains $1.1 trillion in direct federal outlays over the next 10 years. Half of this amount is attributable

to education spending, namely: universal pre-K, free community college, and an increase to the maximum Pell

Grant award, among others. The other half would go toward a variety of ends such as childcare, paid family

and medical leave, and expanded nutrition assistance to children.

The other source of fiscal support under the AFP would be about $900 billion in additional tax expenditures

over the next decade. The AFP would extend the expansions that the American Rescue Plan temporarily made

to a handful of tax credits. For the 2021 tax year, the ARP increased the Child Tax Credit from $2,000 to a fully

refundable $3,600 per child 5 years old and younger and to $3,000 per child between 6 and 17 years old. The

AFP would extend this CTC expansion through 2025 but would make the full refundability of the CTC

permanent, costing nearly $500 billion over the next 10 years. The ARP also expanded the premium tax credit,

which lowers out-of-pocket premiums for lower-income individuals acquiring health insurance through the

marketplaces established by the Affordable Care Act. The AFP would make the expansion of the premium tax

credit permanent. Temporary expansions to the Earned Income Tax Credit and the Child and Dependent Care

Tax Credit under the ARP would also be made permanent.

Finally, the AFP calls for an estimated $1.7 trillion in higher taxes on well-to-do households. Of this amount,

the White House assumes $700 billion would come from greater tax compliance by the wealthiest taxpayers.

This estimate seems to be based on recent research by economists Natasha Sarin and Larry Summers, who

argue that greater tax compliance efforts by the IRS could generate more than $1 trillion in revenue over the

next decade. In addition, the AFP would raise the top marginal tax rate on individuals to 39.6% from 37% and

would tax capital gains and dividends as the same rate as ordinary income for households making more than

$1 million . It would also end a handful of loopholes and tax breaks that disproportionately benefit the

wealthiest taxpayers.

All told, the AFP would increase the deficit by a net $200 billion over the next 10 years but would be fully paid

for over 15 years.

The Week Ahead

CAPI TAL MARKETS RESEARCH

5

APRIL 29, 2021

CAPITAL MARKETS RESEARCH / MARKET OUTLOOK / MOODYS.COM

The Week Ahead – U.S., Europe, Asia-Pacific

THE U.S.

By Adam Kamins of Moody’s Analytics

Vaccine Uptake Is Showing Its Positive Effects

Robust payroll gains nationally in March translated into encouraging figures for the vast majority of

U.S. states and metro areas. In fact, all but one state added jobs over the course of last month and

about 90% of metro economies moved in the right direction over the same period.

A deeper dive into these figures, provides an encouraging window into a set of regional recoveries that

is growing more uniform as herd immunity draws closer and reopenings become more widespread. But

there remain some regional differences, and variation across states reveals the degree to which

incidence still matters. Still, subtle shifts are also noticeable when looking at March figures, perhaps

representing one more sign that the pandemic has entered a new phase.

Digging into the state data

One of the more noticeable aspects of the March payroll data is the fact that few regions actually

stand out. For the first time since July, all but one state (Alaska) experienced job gains. But this time,

that was achieved while U.S. employment increased by about half as many jobs as it did in the early

summer months.

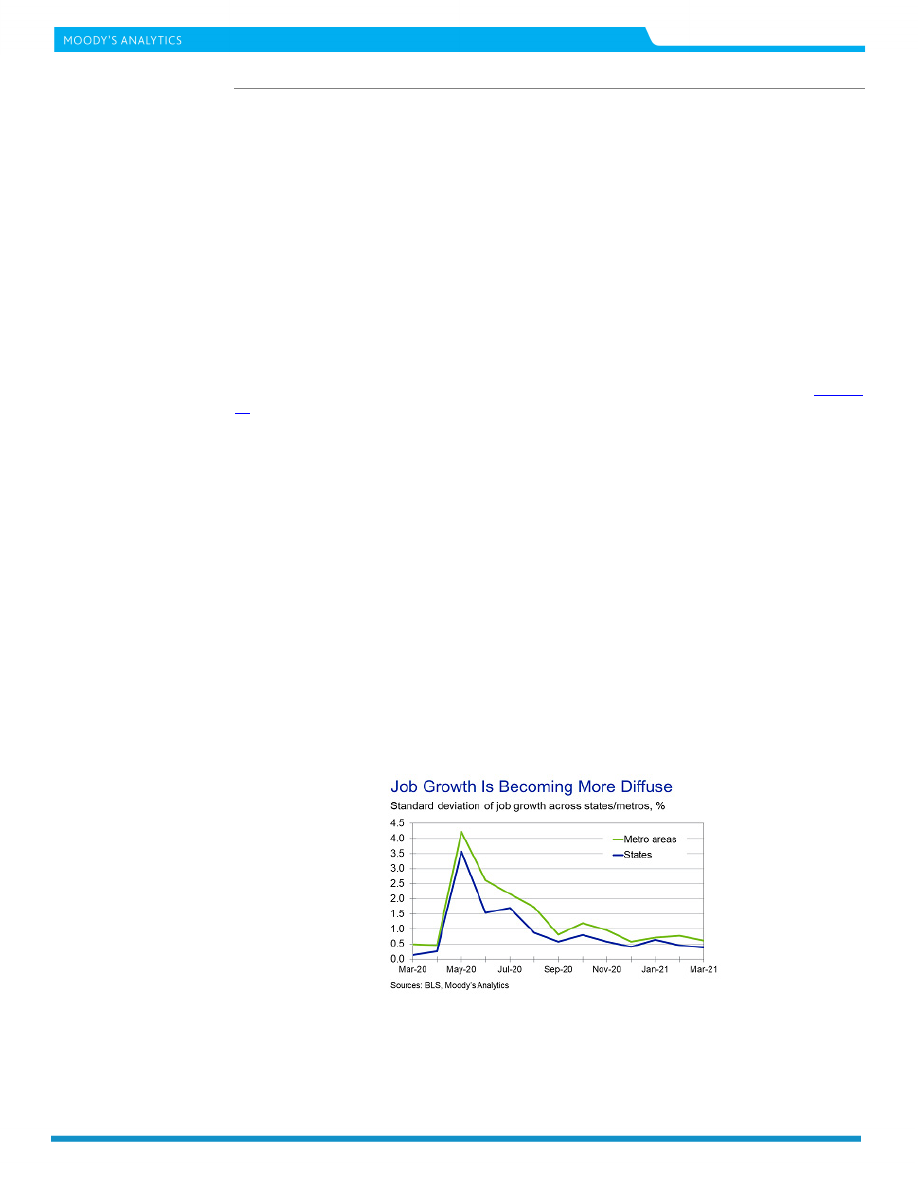

Put it together and it signals that variation across state and metro area economies is diminishing. With

each state generally making a small contribution to overall growth in March, the national economy

increasingly appears to reflect the case of a rising tide lifting all boats. This is also evident when

calculating the standard deviation of job growth across states, which is easily its lowest since March

2020, when the effects of COVID-19 were only starting to trickle into the data.

The trend is even more pronounced at a metro area level. The standard deviation of growth across

metros is not only its lowest of the past year, but below February 2020’s figure. In other words, job

growth is now occurring more evenly across metro area economies than it was even in the last

“normal” month before the pandemic.

Still, within that context, some trends stand out. Oregon and New Mexico led the way from February

to March, a notable turnaround for two states that enacted some of the earliest and most stringent

autumn lockdowns. To some extent, this likely reflects a lower base, but the decisive move in the right

direction also signals that their mitigation measures have been at least partially effective.

The Week Ahead

CAPI TAL MARKETS RESEARCH

6

APRIL 29, 2021

CAPITAL MARKETS RESEARCH / MARKET OUTLOOK / MOODYS.COM

Generally, states that have ramped up their vaccination efforts seem to be picking up the pace a bit

more dramatically. New York and New Jersey in particular improved as more businesses reopened,

residents grew more comfortable, and spending increased. Of course, the March data largely reflect the

re-entry of priority groups such as healthcare workers, seniors, and those with risk factors into the

economy. This may set the stage for continued gains in the months ahead in places where demand for

the vaccine is sufficient to confer something close to herd immunity.

Still, COVID-19 has the potential to wreak havoc. Nowhere is this more pronounced than in Michigan,

where job growth from February to March was subpar and the decline in last month’s growth rate from

the average over the preceding two months was steeper than in any other metro area. This coincides

with a surge in new cases, two factors that are undoubtedly related.

Understanding the drivers

Anecdotally, it seems clear that reopenings, vaccinations, and new COVID-19 cases all made a

difference in March. So in order to more precisely quantify what was behind last month’s numbers, a

series of regressions were run.

The regressions used standardized z-scores (based on each state’s relative distance from the mean) to

account for February to March job growth, the increase in per capita COVID-19 cases, and new

vaccinations per resident. In addition, structural factors such as growth in prior months and the depth

of the initial decline in employment were considered.

The case count was based on the average over the first two weeks of the month, to account for a slight

lag between an outbreak and the reaction from businesses and consumers. And the vaccination rate

considered the share of residents who were fully vaccinated on average over the first week of March

compared with a month earlier.

Based on a sample of 50 states plus Washington DC, and using variables to control for both the

previous month’s job growth and the decline from March to May of last year, the only relationship that

even came close to statistical significance was between job growth and new cases. This was somewhat

surprising based on the importance of both recent performance and early job losses in each state’s

monthly performance. But it reinforces the notion that COVID-19 remains central to the economic

narrative, albeit far less than it did for most of last year.

A surprising vaccine finding

Replacing the vaccination rate variable with a measure that looks at the share of residents who received

their first vaccine dose, as opposed to both doses, changes the results noticeably. The change in the

percentage who received their first shot displayed a positive, statistically significant relationship with

February to March growth despite the fact that only one inoculation does not provide immunity for the

two most widely distributed vaccines.

The Week Ahead

CAPI TAL MARKETS RESEARCH

7

APRIL 29, 2021

CAPITAL MARKETS RESEARCH / MARKET OUTLOOK / MOODYS.COM

There are a few possible explanations for this surprising result. Of course, it could simply represent

statistical noise, reflecting the fact that states that were closed for longer but had more success

vaccinating residents performed better. But the fact that the coefficient on the January to February and

spring 2020 employment changes are generally insignificant at least lends some credence to the notion

that there is something else underlying this result.

Other explanations could entail residents beginning to venture out with one vaccine. Even if they are

not yet fully immune, some may feel a level of protection and begin to re-engage—albeit cautiously—

by spending more on leisure, doing things like going out to eat again, or enrolling children in activities

that increase parents’ productivity and provide a local economic boost.

Similarly, businesses may interpret rising vaccination rates as an encouraging sign. We are already

seeing some evidence of this in several survey-based measures of forward-looking sentiment. With the

end of the pandemic starting to come into view, firms may be starting to hire a bit more aggressively,

especially in hard-hit consumer industries. This could also be contributing to payroll gains that are

stronger in states with more first doses.

Finally, pandemic fatigue could be playing a role. While restrictions were largely lifted in much of the

country early this year, more cautious states and cities have been awaiting evidence of reduced

infections. While cases have not fallen sharply yet, new positive tests have plateaued in most of the

nation, which may be enough to embolden otherwise-cautious elected officials to relent.

In all likelihood, these results reflect a combination of multiple effects. Combine this with the reality

that it is exceedingly difficult for leaders and individuals to put the proverbial genie back in the bottle

once residents have a taste of normalcy and the idea of payrolls backtracking again in the months

ahead seems increasingly far-fetched as lockdowns become a thing of the past.

Evolving drivers

Of course, the relationship among these drivers has evolved over the past year. Early on, the course of

the disease overwhelmed any other factor, and by mid-summer rank orders had largely reversed with

more severe declines giving way to somewhat more robust rebounds in harder-hit states. By autumn,

outbreaks in the upper Midwest were not as economically damaging given many states’ defiance of

medical guidelines, but most evidence suggested that new cases still made a dent in growth.

Early this year, new cases still mattered, with the January to February change showing the same type of

borderline-significant negative relationship that exists in the February to March period. But some

rebound pressures mattered as well, with the March to May 2020 decline a significant predictor of the

one-month delta in employment in February before its relevancy faded last month.

Not surprisingly, early in the rollout the vaccines were not having much impact, either with respect to

share of residents who received one or both doses. It was only in March that the vaccine effect showed

evidence of supplanting the bounce associated with rebounding from a lower trough.

This noticeable shift from one month to the next means that the April job growth figures will bear close

watching. Theoretically, vaccination rates should hold the key to stronger growth in the months ahead.

One can expect that this relationship will solidify further in the months to come—but with hesitancy

taking a toll and new variants raging, that story has yet to be written.

Next Week

The employment report for April, due next Friday, will garner a lot of attention on the heals of March

job gains, and as the recovery continues to takes hold. March saw employment surge 916,000 as the

unemployment rate fell. Recent improvement in initial jobless claims continued in the latest period as

applications for benefits fell for a third consecutive week. April new-vehicle sales should reflect

continued strength. Other key data will include construction spending, factory orders and wholesale

trade.

The Week Ahead

CAPI TAL MARKETS RESEARCH

8

APRIL 29, 2021

CAPITAL MARKETS RESEARCH / MARKET OUTLOOK / MOODYS.COM

EUROPE

By Ross Cioffi of Moody’s Analytics

Industrial Production on the Rise

Retail and industrial production in March are at the center of attention in next week’s important

releases. The Bank of England will also announce its monetary policy decision for May. Euro zone retail

sales likely increased just 0.2% m/m in March after a 3% jump in February. March’s sales were likely

weighed down as lockdowns tightened across the bloc to deal with a new wave of COVID-19

infections. Sales will recoil after the temporary rebound in February, but food sales likely sustained the

growth rate.

We expect industrial production picked up again in March in Germany, France and Spain. As producers

restocked, they were able to start production again. We are forecasting a 1.7% m/m increase in

Germany and a 2% rise in France. However, base effects will start weighing heavily in year-ago

calculations, since the first wave of the pandemic hit this time last year. As a result, we are expecting a

7.5% y/y increase in Spain’s industrial production. Although we are expecting a return to growth in

March, supply shortages remain an issue, so we aren’t betting on a massive rebound just yet. Downside

risks are prevalent. Further, the ongoing supply disruptions throughout March, culminating in the

blockage at the Suez Canal promise an underwhelming April release.

Finally, Russia’s consumer price index will likely rise 5.7% for April. Rising commodity prices and a weak

ruble are keeping price pressures high. The Central Bank of Russia is in a difficult position. It wants to

keep financial conditions accommodative but needs to fight the rise in inflation. The CBR hiked the

interest rate 50 basis points to 5% at its April meeting.

Key indicators

Units

Moody's Analytics

Last

Mon @ 8:00 a.m.

Germany: Retail Sales for March

% change

0.3

1.2

Thur @ 11:00 a.m.

Euro Zone: Retail Sales for March

% change

0.2

3.0

Thur @ 1:00 p.m.

U.K.: Monetary Policy and Minutes for May

%

0.1

0.1

Fri @ 8:00 a.m.

Germany: Industrial Production for March

% change

1.7

-1.6

Fri @ 8:45 a.m.

France: Industrial Production for March

% change

2.0

-4.7

Fri @ 9:00 a.m.

Spain: Industrial Production for March

% change yr ago

7.5

-2.1

Fri @ 10:00 a.m.

Italy: Retail Sales for March

% change

-0.5

6.6

Fri @ 5:00 p.m.

Russia: Consumer Price Index for April

% change yr ago

5.7

5.8

The Week Ahead

CAPI TAL MARKETS RESEARCH

9

APRIL 29, 2021

CAPITAL MARKETS RESEARCH / MARKET OUTLOOK / MOODYS.COM

Asia-Pacific

By Katrina Ell of Moody’s Analytics

Japan raises GDP estimate despite COVID-19 surge

The Bank of Japan expectedly kept the short-term interest rate target steady at -0.1% in April and the

10-year bond yield target at around 0%. What was surprising, was that the central bank struck a

slightly more optimistic tone at its April policy meeting. GDP growth for fiscal 2021, which began on 1

April, was upwardly revised to 4%, from the prior 3.9% estimate. This is astonishing given that the

country's largest prefectures reintroduced emergency restrictions on 25 April following a spike in local

COVID-19 infections.

From 25 April to 11 May, restaurants and bars will be closed and large sporting events will be held

without spectators. This will further hurt the dented consumption and service sectors, with the

restrictions set to occur during Golden Week, when a spike in retail trade usually occurs. These

prefectures represent almost 25% of Japan’s population of 126 million. Japan had been out of its prior

state of emergency for only a month. It has struggled to contain local infections, and its vaccination

drive has been relatively slow, with only 0.7% of the population having received both shots.

This puts added pressure on Japan's export-facing sectors to pick up the slack left by the larger-than-

anticipated dent to domestic demand that will eventuate in the June quarter. Although exports have

performed well of late, export demand is not enough to completely offset the renewed weakness at

home. Seasonally adjusted exports rebounded in March with a 4.5% expansion, following the 4.8%

contraction in February. Japan's export engine performed well in the final months of 2020, and that

was a key driver of its better-than-expected December-quarter GDP data.

The Bank of Japan's inflation forecast for fiscal 2021 was released as 0.1% year over year, down from

0.5% for fiscal 2020. This confirms that the Bank of Japan's 2% target for stable prices will not be

achieved in the foreseeable future, meaning that the elusive goal of creating an environment where

prices, wages and spending are rising remains out of reach.

Key indicators

Units

Moody's Analytics Confidence Risk

Last

Tues @ 9:00 a.m.

South Korea CPI for April

% change yr ago

2.0

2

1.5

Tues @ 11:30 a.m.

Australia Foreign Trade for March

A$ bil

5.3

3

7.5

Tues @ 2:30 p.m.

Australia Monetary Policy for May

%

0.1

4

0.1

Wed @ 2:00 p.m.

Indonesia GDP for Q1

% change yr ago

1.9

2

-2.2

Wed @ 5:05 p.m.

Thailand Monetary Policy for May

%

0.5

4

0.5

Fri @ 1:00 p.m.

China Foreign Trade for April

US$ bil

22.9

3

13.8

Fri @ 6:00 p.m.

Taiwan Foreign Trade for April

US$ bil

3.4

2

3.7

10

APRIL 29, 2021

CAPITAL MARKETS RESEARCH / MARKET OUTLOOK / MOODYS.COM

CAPI TAL MARKETS RESEARCH

The Long View

d

The Long View

High-yield corporate bond issuance is on track to have another strong

month.

By Ryan Sweet, Senior Director-Economic Research

April 29, 2021

CREDIT SPREADS

As measured by Moody's long-term average corporate bond yield, the recent investment grade corporate

bond yield spread of 97 basis points, down 1 basis point from last week. This is below its high over the past 12

months of 179 bp and a hair above its low of 95 bp. Still, the investment grade corporate bond yield is lower

than its 116 bp median of the 30 years ended 2019. This spread may be no wider than 112 bp by year-end

2021.

The recent composite high-yield bond spread of 326 bp approximates what is suggested by the

accompanying long-term Baa industrial company bond yield spread of 136 bp but is narrower than what

might be inferred from the recent VIX of 18 points.

DEFAULTS

March 2021’s U.S. high-yield default rate of 7.5% was up from March 2020’s 4.9%. The recent average high-

yield EDF metric of 1.9% portend a less-than-3% default rate by 2021’s final quarter.

U.S. CORPORATE BOND ISSUANCE

First-quarter 2020’s worldwide offerings of corporate bonds revealed annual advances of 14% for IG and 19%

for high-yield, wherein US$-denominated offerings increased 45% for IG and grew 12% for high yield.

Second-quarter 2020’s worldwide offerings of corporate bonds revealed annual surges of 69% for IG and

32% for high-yield, wherein US$-denominated offerings increased 142% for IG and grew 45% for high yield.

Third-quarter 2020’s worldwide offerings of corporate bonds revealed an annual decline of 6% for IG and an

annual advance of 44% for high-yield, wherein US$-denominated offerings increased 12% for IG and soared

upward 56% for high yield.

Fourth-quarter 2020’s worldwide offerings of corporate bonds revealed an annual decline of 3% for IG and an

annual advance of 8% for high-yield, wherein US$-denominated offerings increased 16% for IG and 11% for

high yield.

First-quarter 2021’s worldwide offerings of corporate bonds revealed an annual decline of 4% for IG and an

annual advance of 57% for high-yield, wherein US$-denominated offerings sank 9% for IG and advanced 64%

for high yield.

U.S. ECONOMIC OUTLOOK

We expect real GDP to rise 6.4% this year, compared with the 5.7% in our March and 4.9% in our February

baselines. We have been consistently revising our forecast higher for GDP this year because of changes to our

fiscal policy assumptions. GDP is expected to rise 5.3% next year, weaker than the 5.7% in the February baseline.

The higher corporate tax rate will bite a little bit into the economy next year, but its drag is in basis points, not

percentage points.

The unemployment rate is expected to average 4.55% in the fourth quarter of this year, compared with 5% in

the March baseline. The unemployment rate averages 3.9% in the fourth quarter of next year, 30 bp lower than

in the prior baseline.

The 10-year Treasury is now expected to average 2% in the fourth quarter of this year, compared with the

1.77% in the March baseline.

11

APRIL 29, 2021

CAPITAL MARKETS RESEARCH / MARKET OUTLOOK / MOODYS.COM

CAPI TAL MARKETS RESEARCH

The Long View

d

Europe

By Ross Cioffi of Moody’s Analytics

April 29, 2021

SWEDEN

’s economy surpassed expectations, growing by 1.1% q/q in the first quarter of 2021. This is only a

preliminary estimate, but it is in line with the upbeat releases of the country’s main macro series. There is still no

decomposition, but we suspect that net exports and private consumption contributed substantially to quarterly

growth. GDP in March drove the quarter’s increase, speeding ahead by 2.1% m/m after a more modest

performance in January and February.

Thanks to the global recovery, external demand was strong during the first quarter, spurring Sweden’s large

manufacturing sector. The view from the domestic economy was also encouraging. Judging by retail sales, the

consumer economy was able to tread water, even if the services side remained painfully stifled by social distancing

practices. Despite the increase in Sweden’s GDP, our expectations for the euro zone release, due out tomorrow, are

more subdued. Sweden benefited from its lack of lockdown and its sectoral make-up: Consumer-facing services

contribute less to total gross value added, while export-oriented capital and intermediate goods producers play

larger roles.

Although the year-on-year growth rate was unchanged in the first quarter, implying that GDP recovered to its year-

ago level, we are not celebrating a full recovery just yet. There are still downside risks looking ahead to the second

quarter. Supply channels have been hard pressed in 2021, as global demand recovers but butts up against global

productive and transport capacity, which are still curbed by the pandemic. Such supply-side disruptions are driving

up producers’ costs and postponing deliveries of inputs. This will delay production schedules and could show up in

the spring accounts as weaker output. That said, when these disruptions ease, a period of make-up growth will

follow. The net effect will be to shift growth from the second to the third and fourth quarters.

EURO ZONE

Loan growth in the euro zone was still on an upward trend in March. During the month, loans to households

increased by 3.3% y/y, speeding up from 3% growth in February. Loans to companies increased by 5.3%, slowing

from 7% growth in the month before. Consensus expectations were for a stronger year-on-year growth rate to

companies, but we are not worried about the slower growth rate, as it is not a sign that monetary conditions are

tightening. Base effects are behind the slowdown. And considering how large the increase in corporate lending was

in March, April and May of 2020, a 5.3% growth rate, which is still well above pre-pandemic trends, is a testament

to how accommodative financing conditions still are.

On a similar note, the M3 money supply increased by 10.1% y/y in March to €14.7 trillion. The growth rate slowed

from 13.3% y/y in February but was considerably higher than the 5% average growth registered in 2019.

GERMANY

German consumers lost confidence heading into May, according to the GfK consumer confidence index, which slid

to -8.8 from -6.1. The loss of confidence comes as lockdown measures were tightened in Germany amidst the third

wave of the COVID-19 pandemic. Whereas in April hopes ran high that lockdowns would be ending soon, the fact

that daily infections are still swelling, making a speedy loosening of restrictions unlikely, discouraged German

consumers.

Income expectations tumbled heading into May. This was due to the retail sector in particular, which continues to

see its reopening pushed back. The good news, however, is that the indicator reflecting individuals’ propensity to

buy increased. Lockdowns may have been extended, but pent-up consumer demand continues to build. Fiscal

policies such as short-time work schemes are keeping a floor under incomes and adding job security. Meanwhile,

the manufacturing sector continues to recover, bolstering incomes and jobs. All this means that even as the general

view on the economy remains grim, consumers will be able to spend once shops reopen. It is this post-lockdown

spending spree that will kickstart the recovery.

12

APRIL 29, 2021

CAPITAL MARKETS RESEARCH / MARKET OUTLOOK / MOODYS.COM

CAPI TAL MARKETS RESEARCH

The Long View

d

Asia Pacific

By Katrina Ell of Moody’s Analytics

April 29, 2021

CHINA

’s foreign trade surplus likely widened in April, after narrowing to US$13.8 billion in March. China’s

exports will remain elevated in year-over-year terms due to low base effects as the pandemic wreaked havoc

on foreign demand. But beyond that, pent-up foreign demand is expected to ease over the year, particularly

for audio and video equipment and parts, lighting devices, and furniture. Factories have reopened in many

major economies, and their domestic manufacturing is picking up speed, squeezing demand on China’s

exports. The domestic market will play a more important role in digesting and supporting production this

year, backing import growth and likely keeping the trade balance relatively narrow.

The surge in China’s imports in March was largely due to rising prices. The import volume of refined oil and

pharmaceutical products slipped compared with December, but their import value soared by more than 35%.

This is common across most import products, creating further evidence of global inflation.

AUSTRALIA

On the policy front, the Reserve Bank of Australia will keep all monetary settings on hold in May. Now is not

the time to scale back the unprecedented level of monetary support that was introduced at the height of the

COVID-19 outbreak last year. While the economy is certainly on the path to recovery, it is far from being back

at pre-pandemic levels. We can observe this most clearly in the labour market, where underemployment

remains relatively high and wage growth subdued. The RBA does not expect to see inflation back in the 2% to

3% range along with wage growth being substantially higher until 2024 at the earliest.

The property market is a growing area of concern for the central bank, specifically concerned about ensuring

that lending standards are maintained in this sustained low interest rate environment. If the housing market

continues to heat up, we will see action from the regulator, likely via targeted measures such as loan-to-value

restrictions, to ensure that lending standards are not wavering with the cheap availability of money.

In the near term, there are risks to Australia's still-fragile economic recovery. A key risk is via the withdrawal of

the wage subsidy scheme, JobKeeper, at the end of March, which could trigger a temporary pullback in

spending in the second quarter and weaken the pace of the labour market revival. The magnitude of the

pullback is unlikely to be severe, though it will add to near-term labour market slackness.

13

APRIL 29, 2021

CAPITAL MARKETS RESEARCH / MARKET OUTLOOK / MOODYS.COM

CAPI TAL MARKETS RESEARCH

Ratings Round-Up

Ratings Round-Up

Upgrades for 10 of 11 U.S. Changes; Europe Activity Shows Improvement

By Michael Ferlez

April 29, 2021

U.S. corporate credit quality remained strong last week. For the period ending April 27, upgrades accounted

for ten of the eleven changes and all the affected debt. Rating changes were spread across numerous

industries, with speculative-grade companies accounting for the bulk of rating changes. The period’s most

notable upgrade was made to Caterpillar Inc. On April 21, Moody’s Investors Service upgraded the long-term

and short-term ratings of Caterpillar Inc., Caterpillar Financial Services Corporation, and their supported

affiliates to A2 and Prime-1 respectively. In their rating action, Moody Investors Service cited higher returns

CAT will generate throughout the business cycle. Moody’s also said it anticipates that CAT’s core operation

should be able to maintain EBITA margins over 10% during downturns.

Both the European rating change activity and the composition of changes improved from the prior period.

Upgrades accounted for six of the nine changes and roughly 86% of affected debt. The United Kingdom led

with three rating changes. The period’s largest upgrade was made to HeidelbergCement AG, which saw its

long-term issuer rating and senior unsecured rating upgraded to Baa2 and its senior unsecured medium-term

note program upgraded to (P)Baa2. In addition, Moody’s Investors Service upgraded the several ratings

related to HeidelbergCement Finance Luxembourg S.A. In the rating action, Vitali Morgovski, a Moody's

assistant vice president-analyst and lead analyst for HeidelbergCement AG, was cited saying, "Our decision to

upgrade HC's ratings reflects its resilient performance throughout 2020 with stronger than anticipated credit

metrics at the end of the year that are well commensurate with the Baa2 rating requirements. We believe the

ongoing economic recovery with a healthy level of construction activity together with HeidelbergCement

AG's focus on cash flow generation will allow sustaining these levels in coming years. The group's more

conservative financial policy including reduced leverage target with a focus on predominantly organic growth

objectives provides further comfort.” The rating change affected $9.2 billion in debt.

.

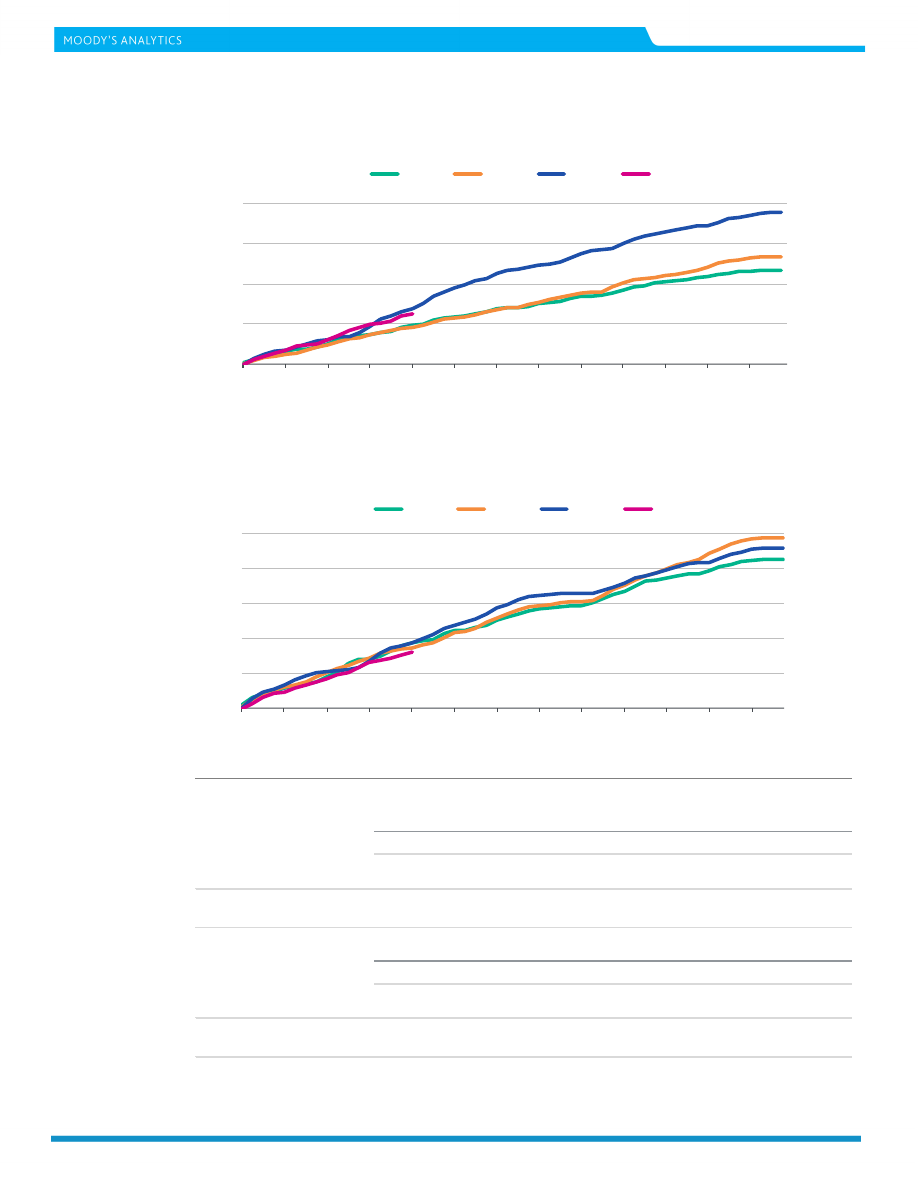

FIGURE 1

Rating Changes - US Corporate & Financial Institutions: Favorable as % of Total Actions

0.0

0.2

0.4

0.6

0.8

1.0

0.0

0.2

0.4

0.6

0.8

1.0

Feb02

Apr05

Jun08

Aug11

Oct14

Dec17

Feb21

By Count of Actions

By Amount of Debt Affected

* Trailing 3-month average

Source: Moody's

14

APRIL 29, 2021

CAPITAL MARKETS RESEARCH / MARKET OUTLOOK / MOODYS.COM

CAPI TAL MARKETS RESEARCH

Ratings Round-Up

FIGURE 2

Rating Key

BCF

Bank Credit Facility Rating

MM

Money-Market

CFR

Corporate Family Rating

MTN

MTN Program Rating

CP

Commercial Paper Rating

Notes

Notes

FSR

Bank Financial Strength Rating

PDR

Probability of Default Rating

IFS

Insurance Financial Strength Rating

PS

Preferred Stock Rating

IR

Issuer Rating

SGLR

Speculative-Grade Liquidity Rating

JrSub

Junior Subordinated Rating

SLTD

Short- and Long-Term Deposit Rating

LGD

Loss Given Default Rating

SrSec

Senior Secured Rating

LTCF

Long-Term Corporate Family Rating

SrUnsec

Senior Unsecured Rating

LTD

Long-Term Deposit Rating

SrSub

Senior Subordinated

LTIR

Long-Term Issuer Rating

STD

Short-Term Deposit Rating

FIGURE 3

Rating Changes: Corporate & Financial Institutions – US

Date

Company

Sector

Rating

Amount

($

Million)

Up/

Down

Old LTD

Rating

New

LTD

Rating

O

l

d

S

IG/S

G

4/21/21 CATERPILLAR INC.

Industrial

SrUnsec/LTIR/MTN/

CP

35,340

U

A3

A2

IG

4/21/21 OLD DOMINION ELECTRIC COOPERATIVE

Utility

SrSec

550

U

A2

A1

IG

4/21/21 ALLIED UNIVERSAL HOLDCO LLC

Industrial

SrSec/SrUnsec/SrSec

/BCF/LTCFR/PDR

2,990

U

B3

B2

SG

4/21/21 MEDICAL DEPOT HOLDINGS, INC.

Industrial

SrSec/BCF/LTCFR/P

DR

U

Caa2

Caa1

SG

4/22/21

ALLETE, INC.-SUPERIOR WATER, LIGHT AND POWER

COMPANY

Industrial

LTIR

D

A3

Baa1

IG

4/22/21 POPULAR, INC.

Financial SrUnsec/LTIR/STD/L

TD/MTN/PS

1,567

U

B1

Ba3

SG

4/22/21 CONN'S, INC.

Industrial

LTCFR

U

B2

B1

SG

4/22/21 EXCEL FITNESS HOLDINGS, INC.

Industrial SrSec/BCF/LTCFR/P

DR

U

Caa1

B3

SG

4/23/21

PENN NATIONAL GAMING, INC. (OLD)-PENN

NATIONAL GAMING, INC.

Industrial

SrSec/BCF

400

U

B1

Ba3

SG

4/26/21 APPLIED MATERIALS INC.

Industrial

SrUnsec/CP

5,500

U

A3

A2

IG

4/26/21 UNIVAR N.V. -UNIVAR SOLUTIONS INC.

Industrial

SrUnsec/SrSec/BCF/

LTCFR/PDR

500

U

Ba3

Ba2

SG

Source: Moody's

15

APRIL 29, 2021

CAPITAL MARKETS RESEARCH / MARKET OUTLOOK / MOODYS.COM

CAPI TAL MARKETS RESEARCH

Ratings Round-Up

FIGURE 4

Rating Changes: Corporate & Financial Institutions – Europe

Date

Company

Sector

Rating

Amount

($ Million)

Up/

Down

Old LTD

Rating

New

LTD

Rating

Country

4/21/2021 HEIDELBERGCEMENT AG

Industrial SrUnsec/LTIR/

9,217.9

U

Baa3

Baa2

GERMANY

4/21/2021 POLYUS GOLD INTERNATIONAL LIMITED-

POLYUS FINANCE PLC

Industrial SrUnsec

1,757.9

U

Ba1

Baa3

UNITED KINGDOM

4/21/2021 BFF BANK S.P.A.

Financial SrUnsec/LTIR/

361.5

D

Ba1

Ba2

ITALY

4/23/2021

CODERE S.A. -CODERE FINANCE 2

(LUXEMBOURG) S.A.

Industrial SrSec/LTCFR/

1,203.7

D

Caa3

Ca

LUXEMBOURG

4/23/2021

EAGLE SUPER GLOBAL HOLDING B.V .-

EAGLE INTERMEDIATE GLOBAL HOLDING

B.V.

Industrial SrSec/LTCFR/

991.2

U

Caa2

Caa1

NETHERLANDS

4/26/2021 DAKAR FINANCE S.A.-PARTS EUROPE S.A. Industrial SrSec/LTCFR/

1,065.2

U

Caa1

B3

FRANCE

4/26/2021 FERROGLOBE PLC

Industrial PDR

U

Ca

Caa1

UNITED KINGDOM

4/27/2021

CENTRAL NOTTINGHAMSHIRE

HOSPITALS PLC

Industrial SrSec

487.0

D

Baa3

Ba1

UNITED KINGDOM

4/27/2021 VERALLIA S.A.

Industrial LTCFR

U

Ba3

Ba2

FRANCE

Source: Moody's

16

APRIL 29, 2021

CAPITAL MARKETS RESEARCH / MARKET OUTLOOK / MOODYS.COM

CAPI TAL MARKETS RESEARCH

Market Data

Market Data

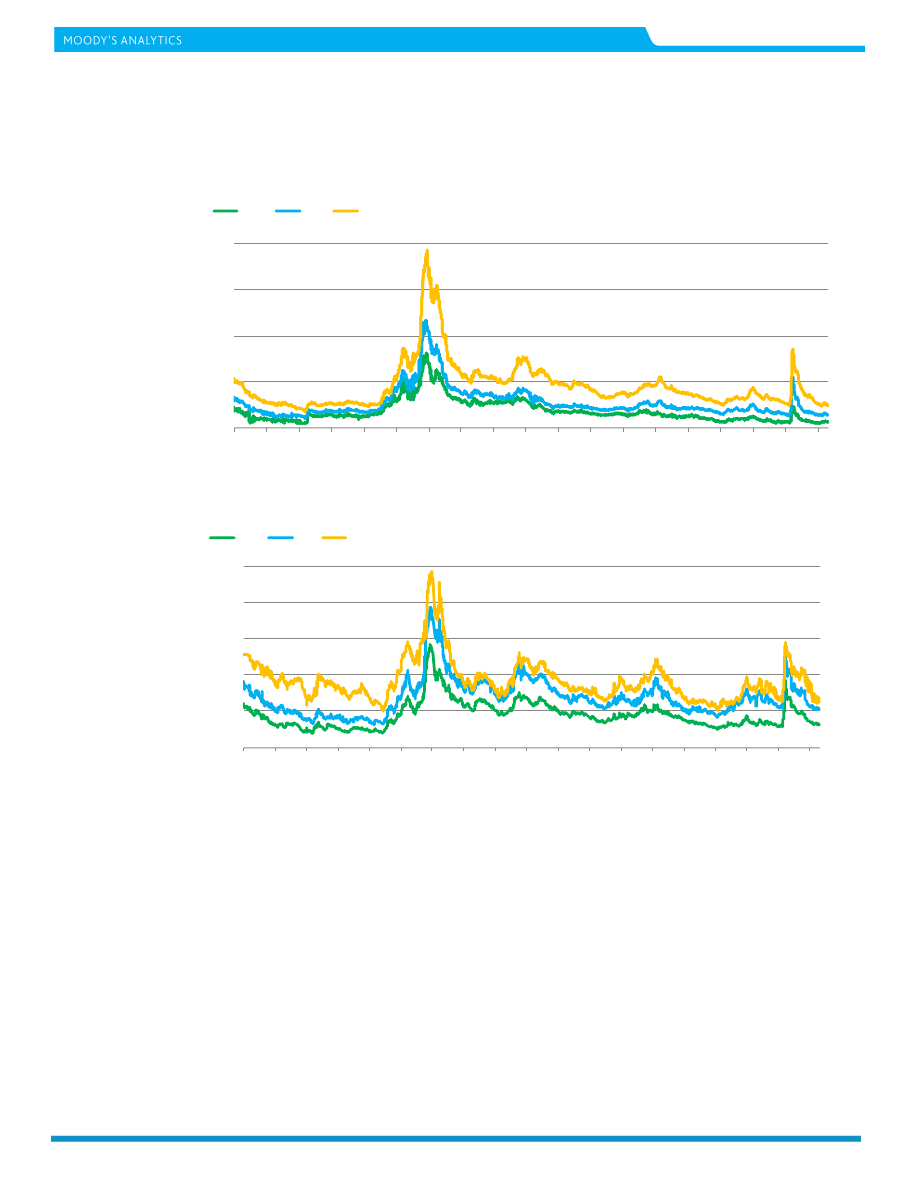

Spreads

0

200

400

600

800

0

200

400

600

800

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Spread (bp)

Spread (bp)

Aa2

A2

Baa2

Source: Moody's

Figure 1: 5-Year Median Spreads-Global Data (High Grade)

0

400

800

1,200

1,600

2,000

0

400

800

1,200

1,600

2,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Spread (bp)

Spread (bp)

Ba2

B2

Caa-C

Source: Moody's

Figure 2: 5-Year Median Spreads-Global Data (High Yield)

17

APRIL 29, 2021

CAPITAL MARKETS RESEARCH / MARKET OUTLOOK / MOODYS.COM

CAPI TAL MARKETS RESEARCH

Market Data

CDS Movers

CDS Implied Rating Rises

Issuer

Apr. 28

Apr. 21

Senior Ratings

Archer-Daniels-Midland Company

A2

Baa1

A2

Comcast Corporation

A2

A3

A3

American Express Credit Corporation

A2

A3

A2

Occidental Petroleum Corporation

B1

B2

Ba2

Capital One Financial Corporation

Baa2

Baa3

Baa1

United Parcel Service, Inc.

Aa3

A1

A2

Tenet Healthcare Corporation

B1

B2

Caa1

Crown Castle International Corp .

Baa2

Baa3

Baa3

ViacomCBS Inc.

Baa2

Baa3

Baa2

Dish DBS Corporation

B3

Caa1

B2

CDS Implied Rating Declines

Issuer

Apr. 28

Apr. 21

Senior Ratings

Kroger Co. (The)

Baa1

A2

Baa1

Conagra Brands, Inc.

Baa2

A3

Baa3

McDonald's Corporation

A1

Aa3

Baa1

Exxon Mobil Corporation

A2

A1

Aa2

Procter & Gamble Company (The)

Aa3

Aa2

Aa3

Johnson & Johnson

Aa2

Aa1

Aaa

Amazon.com, Inc.

A3

A2

A2

Amgen Inc.

A2

A1

Baa1

Burlington Northern Santa Fe, LLC

A1

Aa3

A3

CCO Holdings, LLC

Ba2

Ba1

B1

CDS Spread Increases

Issuer

Senior Ratings

Apr. 28

Apr. 21

Spread Diff

Staples, Inc.

B3

711

692

18

R.R. Donnelley & Sons Company

B3

476

463

13

Beazer Homes USA, Inc.

B3

314

305

9

Mattel, Inc.

Ba2

223

215

8

Colgate-Palmolive Company

Aa3

34

27

7

Amkor Technology, Inc.

B1

135

128

7

Kroger Co. (The)

Baa1

49

43

6

Conagra Brands, Inc.

Baa3

54

48

6

Yum! Brands Inc.

Ba3

92

87

6

International Game Technology

B3

282

276

6

CDS Spread Decreases

Issuer

Senior Ratings

Apr. 28

Apr. 21

Spread Diff

Tenet Healthcare Corporation

Caa1

258

313

-55

Apache Corporation

Ba1

260

310

-51

Nabors Industries, Inc .

Caa2

998

1,045

-47

Occidental Petroleum Corporation

Ba2

274

305

-31

Realogy Group LLC

Caa1

369

395

-26

Dish DBS Corporation

B2

343

367

-24

Pitney Bowes Inc.

B1

409

431

-23

United States Steel Corporation

Caa1

390

408

-19

Juniper Networks, Inc.

Baa2

93

112

-19

United Airlines Holdings, Inc.

Ba3

400

419

-18

Source: Moody's, CMA

CDS Spreads

CDS Implied Ratings

CDS Implied Ratings

CDS Spreads

Figure 3. CDS Movers - US ( April 21, 2021 – April 28, 2021)

18

APRIL 29, 2021

CAPITAL MARKETS RESEARCH / MARKET OUTLOOK / MOODYS.COM

CAPI TAL MARKETS RESEARCH

Market Data

CDS Implied Rating Rises

Issuer

Apr. 28

Apr. 21

Senior Ratings

Bayerische Landesbank

A1

Baa2

Aa3

Schaeffler Finance B.V.

A2

Baa1

Ba2

BNP Paribas

A1

A2

Aa3

National Grid plc

A1

A2

Baa2

Severn Trent Plc

Baa2

Baa3

Baa2

Thales

A3

Baa1

A2

Vedanta Resources Limited

Ca

C

Caa1

CMA CGM S.A.

Caa1

Caa2

B3

Legrand France S.A.

A2

A3

A3

Italy, Government of

Baa3

Baa3

Baa3

CDS Implied Rating Declines

Issuer

Apr. 28

Apr. 21

Senior Ratings

Rabobank

Aa3

Aa2

Aa3

Barclays PLC

Baa2

Baa1

Baa2

Portugal, Government of

A1

Aa3

Baa3

UniCredit S.p.A.

Baa3

Baa2

Baa1

Svenska Handelsbanken AB

Aa3

Aa2

Aa2

Swedbank AB

A1

Aa3

Aa3

RCI Banque

Ba3

Ba2

Baa2

ENGIE SA

A2

A1

Baa1

Compagnie de Saint-Gobain SA

A3

A2

Baa2

SSE plc

A3

A2

Baa1

CDS Spread Increases

Issuer

Senior Ratings

Apr. 28

Apr. 21

Spread Diff

Boparan Finance plc

Caa1

703

687

16

Jaguar Land Rover Automotive Plc

B1

351

347

5

RCI Banque

Baa2

190

185

4

Renault S.A.

Ba2

185

181

4

Ineos Group Holdings S.A.

B2

245

241

4

Italy, Government of

Baa3

80

77

3

Intesa Sanpaolo S.p.A.

Baa1

64

60

3

UniCredit S.p.A.

Baa1

68

65

3

Unione di Banche Italiane S.p.A.

Baa3

75

72

3

thyssenkrupp AG

B1

246

243

3

CDS Spread Decreases

Issuer

Senior Ratings

Apr. 28

Apr. 21

Spread Diff

Vedanta Resources Limited

Caa1

807

907

-100

Bayerische Landesbank

Aa3

31

66

-35

National Bank of Greece S.A.

Caa1

189

213

-24

TUI AG

Caa1

872

893

-21

CMA CGM S.A.

B3

383

403

-20

Severn Trent Plc

Baa2

54

72

-18

Novafives S.A.S.

Caa2

752

769

-17

Casino Guichard-Perrachon SA

Caa1

512

524

-12

Schaeffler Finance B.V.

Ba2

41

53

-11

Premier Foods Finance plc

B3

208

218

-10

Source: Moody's, CMA

CDS Spreads

CDS Implied Ratings

CDS Implied Ratings

CDS Spreads

Figure 4. CDS Movers - Europe ( April 21, 2021 – April 28, 2021)

19

APRIL 29, 2021

CAPITAL MARKETS RESEARCH / MARKET OUTLOOK / MOODYS.COM

CAPI TAL MARKETS RESEARCH

Market Data

Issuance

0

700

1,400

2,100

2,800

0

700

1,400

2,100

2,800

Jan Feb Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Issuance ($B)

Issuance ($B)

2018

2019

2020

2021

Source:

Moody's / Dealogic

Figure 5. Market Cumulative Issuance - Corporate & Financial Institutions: USD Denominated

0

200

400

600

800

1,000

0

200

400

600

800

1,000

Jan Feb Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Issuance ($B)

Issuance ($B)

2018

2019

2020

2021

Source:

Moody's / Dealogic

Figure 6. Market Cumulative Issuance - Corporate & Financial Institutions: Euro Denominated

Investment-Grade

High-Yield

Total*

Amount

Amount

Amount

$B

$B

$B

Weekly

37.775

11.282

49.175

Year-to-Date

612.427

253.227

885.546

Investment-Grade

High-Yield

Total*

Amount

Amount

Amount

$B

$B

$B

Weekly

14.707

3.454

18.160

Year-to-Date

254.201

56.182

320.251

* Difference represents issuance with pending ratings.

Source: Moody's/ Dealogic

USD Denominated

Euro Denominated

Figure 7. Issuance: Corporate & Financial Institutions

20

APRIL 29, 2021

CAPITAL MARKETS RESEARCH / MARKET OUTLOOK / MOODYS.COM

CAPI TAL MARKETS RESEARCH

Moody’s Capital Markets Research recent publications

Record-High Systemic Leverage Limits Upside for Benchmark Interest Rates (Capital Market Research)

Will Excessive Stimulus Lead to Excessive Leverage? (Capital Market Research)

Replay of the Inflationary 1970s Is Unlikely (Capital Market Research)

Real GDP Growth’s Biggest Improvement since 1950 May Power 2021’s Profits Growth (Capital Market Research)

Positive Outlook for Corporate Earnings Favors Narrower Credit Spreads (Capital Market Research)

Moody’s Analytics EDF-Based Bond Valuation Model Version 2.0

Stocks and High-Yield Performed Well Amid Prior Upturns by Treasury Bond Yields (Capital Market Research)

Quality Bonds Retreat as Leveraged Loans Shine (Capital Market Research)

Too Much of a Good Thing? (Capital Market Research)

Fast Declining EDF Favors Thinner High-Yield Bond Spread (Capital Market Research)

Prices Rise Here, There and Everywhere (Capital Market Research)

Investment-Grade Bond Offerings to Slow from 2020’s Torrid Pace (Capital Market Research)

Not All Debt Is Equal (Capital Market Research)

Market Value of U.S. Common Stock Soars to Record-High 185% of GDP (Capital Market Research)

Stimulatory Monetary and Fiscal Policies Enhance Corporate Credit Outlook (Capital Market Research)

Financial Markets Have Largely Priced-In 2021’s Positive Outlook (Capital Market Research)

Core Profits and U.S. Equities Set New Record Highs (Capital Market Research)

Operating Leverage May Help to Narrow Yield Spreads in 2021 (Capital Market Research)

Resurgent COVID-19 Threatens Corporate Credit’s Improved Trend (Capital Market Research)

Split Congress Sparks Rallies by Equities, Corporates and Treasuries (Capital Market Research)

Credit Disputes Equities Gloom (Capital Market Research)

Corporate Cash Outruns Corporate Debt (Capital Market Research)

Profits Give Direction to Downgrades and Defaults (Capital Market Research)

Markets Sense an Upturn Despite Pockets of Profound Misery (Capital Market Research)

Record-High Bond Issuance Aids Nascent Upturn (Capital Market Research)

Corporate Bond Issuance Boom May Steady Credit Quality, On Balance (Capital Market Research)

Markets, Bankers and Analysts Differ on 2021’s Default Rate (Capital Market Research)

Corporate Credit Mostly Unfazed by Equity Volatility (Capital Market Research)

Record August for Bond Issuance May Aid Credit Quality (Capital Market Research)

Fed Policy Shift Bodes Well for Corporate Credit (Capital Markets Research)

Markets Avoid Great Recession’s Calamities (Capital Markets Research)

Liquidity Surge Hints of More Upside Surprises (Capital Markets Research)

Unprecedented Stimulus Lessens the Blow from Real GDP’s Record Dive (Capital Markets Research)

Ultra-Low Bond Yields Buoy Corporate Borrowing (Capital Markets Research)

21

APRIL 29, 2021

CAPITAL MARKETS RESEARCH / MARKET OUTLOOK / MOODYS.COM

CAPI TAL MARKETS RESEARCH

To order reprints of this report (100 copies minimum), please call 212.553.1658 .

Report Number: 1281425

Contact Us

Editor

Reid Kanaley

Americas:

1.212.553 .4399

Europe:

+44 (0) 20.7772.5588

Asia:

813.5408.4131

22

APRIL 29, 2021

CAPITAL MARKETS RESEARCH / MARKET OUTLOOK / MOODYS.COM

CAPI TAL MARKETS RESEARCH

© 2021 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S CREDIT RATINGS AFFILIATES ARE THEIR CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT

COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MATERIALS, PRODUCTS, SERVICES AND INFORMATION PUBLISHED BY MOODY’S (COLLECTIVELY,

“PUBLICATIONS”) MAY INCLUDE SUCH CURRENT OPINIONS. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL

FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT OR IMPAIRMENT. SEE APPLICABLE MOODY’S

RATING SYMBOLS AND DEFINITIONS PUBLICATION FOR INFORMATION ON THE TYPES OF CONTRACTUAL FINANCIAL OBLIGATIONS ADDRESSED BY MOODY’S

CREDIT RATINGS. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE

VOLATILITY. CREDIT RATINGS, NON-CREDIT ASSESSMENTS (“ASSESSMENTS”), AND OTHER OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT

STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND

RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. AND/OR ITS AFFILIATES. MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER

OPINIONS AND PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER

OPINIONS AND PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. MOODY’S

CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS DO NOT COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR

INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS, ASSESSMENTS AND OTHER OPINIONS AND PUBLISHES ITS PUBLICATIONS WITH THE EXPECTATION AND

UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION

FOR PURCHASE, HOLDING, OR SALE. MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS, AND PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL

INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FOR RETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS WHEN MAKING

AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIED

OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR

ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN

CONSENT.

MOOD’S CREDIT RATINGS, ASSESSMENTS, OR OTHER OPINIONS AND PUBLICATIONS ARE NOT INTENDED FOR USE BY ANY PERSON AS A BENCHMARK AS THAT TERM IS

DEFINED FOR REGULATORY PURPOSES AND MUST NOT BE USED IN ANY WAY THAT COULD RESULT IN THEM BEING CONSIDERED A BENCHMARK.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as

other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information it uses

in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,

MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody’s publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for any

indirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use any

such information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses

or damages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of

a particular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatory

losses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for the

avoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents,

representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY

CREDIT RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (including

corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any rating,

agreed to pay to Moody’s Investors Service, Inc. for ratings opinions and services rendered by it fees ranging from $1,000 to approximately $5,000,000 . MCO and MIS also

maintain policies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of

MCO and rated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted

annually at

under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s Investors

Service Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intended to

be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, you

represent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly or

indirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as to

the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly owned by Moody’s

Overseas Holdings Inc., a wholly owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly owned credit rating agency subsidiary of MJKK. MSFJ is not a Nationally

Recognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by an

entity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies

registered with the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred

stock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for ratings opinions and services rendered by its

fees ranging from JPY125,000 to approximately JPY550,000,000 .

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

For Publications Issued by Moody’s Capital Markets Research, Inc. only:

The statements contained in this research report are based solely upon the opinions of Moody’s Capital Markets Research, Inc. and the data and information available to the

authors at the time of publication of this report. There is no assurance that any predicted results will actually occur. Past performance is no guarantee of future results.

The analysis in this report has not been made available to any issuer prior to publication.

When making an investment decision, investors should use additional sources of information and consult with their investment advisor. Investing in securities involves certain risks

including possible fluctuations in investment return and loss of principal. Investing in bonds presents additional risks, including changes in interest rates and credit risk.

Moody's Capital Markets Research, Inc., is a subsidiary of MCO. Please note that Moody’s Analytics, Inc., an affiliate of Moody’s Capital Markets Research, Inc. and a subsidiary of

MCO, provides a wide range of research and analytical products and services to corporations and participants in the financial markets. Customers of Moody’s Analytics, Inc. may

include companies mentioned in this report. Please be advised that a conflict may exist and that any investment decisions you make are your own responsibility. The Moody’s

Analytics logo is used on certain Moody’s Capital Markets Research, Inc. products for marketing purposes only. Moody’s Analytics, Inc. is a separate company from Moody’s Capital

Markets Research, Inc.