Gibson Energy Inc (TSE:GEI): When Will It Breakeven?

Gibson Energy Inc’s (TSX:GEI): Gibson Energy Inc., an integrated midstream company, engages in the movement, storage, optimization, processing, marketing, and distribution of crude oil, condensate, natural gas liquids (NGLs), water, oilfield waste, and refined products in North America. The CA$2.47B market-cap company’s loss lessens since it announced a -CA$115.71M bottom-line in the full financial year, compared to the latest trailing-twelve-month loss of -CA$99.77M, as it approaches breakeven. As path to profitability is the topic on GEI’s investors mind, I’ve decided to gauge market sentiment. I’ve put together a brief outline of industry analyst expectations for GEI, its year of breakeven and its implied growth rate.

Check out our latest analysis for Gibson Energy

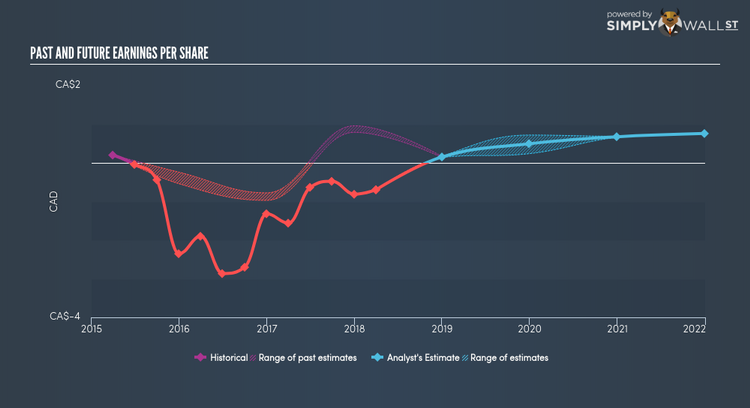

GEI is bordering on breakeven, according to analysts. They expect the company to post a final loss in 2017, before turning a profit of CA$22.01M in 2018. Therefore, GEI is expected to breakeven roughly a few months from now. In order to meet this breakeven date, I calculated the rate at which GEI must grow year-on-year. It turns out an average annual growth rate of 60.46% is expected, which is extremely buoyant. Should the business grow at a slower rate, it will become profitable at a later date than expected.

Underlying developments driving GEI’s growth isn’t the focus of this broad overview, though, take into account that by and large an oil and gas business has lumpy cash flows which are contingent on the natural resource and stage at which the company is operating. So, a high growth rate is not out of the ordinary, particularly when a company is in a period of investment.

Before I wrap up, there’s one issue worth mentioning. GEI currently has a debt-to-equity ratio of 154.47%. Generally, the rule of thumb is debt shouldn’t exceed 40% of your equity, which in GEI’s case, it has significantly overshot. Note that a higher debt obligation increases the risk in investing in the loss-making company.

Next Steps:

There are key fundamentals of GEI which are not covered in this article, but I must stress again that this is merely a basic overview. For a more comprehensive look at GEI, take a look at GEI’s company page on Simply Wall St. I’ve also put together a list of relevant factors you should look at:

Valuation: What is GEI worth today? Has the future growth potential already been factored into the price? The intrinsic value infographic in our free research report helps visualize whether GEI is currently mispriced by the market.

Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on Gibson Energy’s board and the CEO’s back ground.

Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.