Is Greatime International Holdings (HKG:844) Using Too Much Debt?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Greatime International Holdings Limited (HKG:844) makes use of debt. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Greatime International Holdings

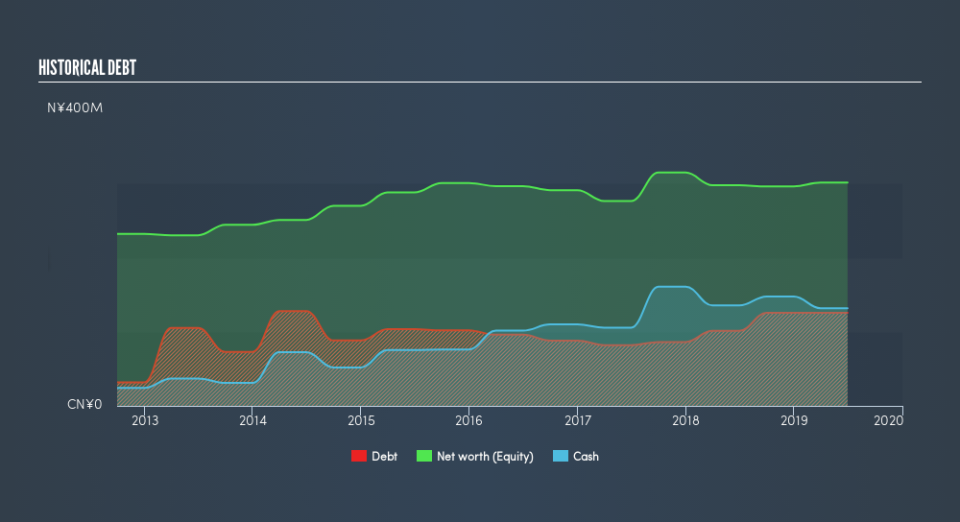

What Is Greatime International Holdings's Debt?

You can click the graphic below for the historical numbers, but it shows that as of June 2019 Greatime International Holdings had CN¥125.4m of debt, an increase on CN¥101.2m, over one year. However, it does have CN¥131.7m in cash offsetting this, leading to net cash of CN¥6.31m.

How Strong Is Greatime International Holdings's Balance Sheet?

We can see from the most recent balance sheet that Greatime International Holdings had liabilities of CN¥205.9m falling due within a year, and liabilities of CN¥769.0k due beyond that. Offsetting this, it had CN¥131.7m in cash and CN¥59.1m in receivables that were due within 12 months. So it has liabilities totalling CN¥15.9m more than its cash and near-term receivables, combined.

Of course, Greatime International Holdings has a market capitalization of CN¥284.2m, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. Despite its noteworthy liabilities, Greatime International Holdings boasts net cash, so it's fair to say it does not have a heavy debt load!

Notably, Greatime International Holdings made a loss at the EBIT level, last year, but improved that to positive EBIT of CN¥7.8m in the last twelve months. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Greatime International Holdings will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While Greatime International Holdings has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last year, Greatime International Holdings burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Summing up

While it is always sensible to look at a company's total liabilities, it is very reassuring that Greatime International Holdings has CN¥6.3m in net cash. So although we see some areas for improvement, we're not too worried about Greatime International Holdings's balance sheet. Over time, share prices tend to follow earnings per share, so if you're interested in Greatime International Holdings, you may well want to click here to check an interactive graph of its earnings per share history.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.