Is This 'Hated' Industry Making A Comeback?

During the past half decade, few industries have suffered as much as the for-profit education industry.

Congress took these companies to task when it became apparent that their students had poor graduation rates and many of those students were unable to find jobs and repay government-backed loans. The default rate on student loans at these institutions now exceeds 9%, which is alarmingly high.

Congressional hearings -- which questioned whether these firms were even necessary -- and a poor reputation among potential applicants have led to steady enrollment declines at almost all of the companies. And their share prices fell sharply, year after year, seemingly without a bottom.

And then a strange thing happened. These for-profit education stocks have begun to rally, posting the some of the sharpest gains in the market over the past month. Here’s a quick look at the one-month performance of 10 for-profit education stocks.

Still, these gains are cold comfort for the investors who have been wiped out in these stocks in recent years. Many of these stocks such as Strayer Education (STRA) and Corinthian Colleges (COCO) have fallen more than 70% since the industry's troubles began in 2010, despite the recent rebound.

Tangible And Intangible Causes

What’s driving the rebound? Well, the rally began in the midst of earnings season as many of these firms delivered quarterly results that were not quite as bad as had been feared. In fact, only Corinthian Colleges missed analysts’ forecasts.

For an industry that was heavily shorted, might that have led to a massive short squeeze? Looking at the two-week change in short positions for May 15, it’s hard to spot a clear trend. In fact, short sellers have built even bigger positions in names such as Strayer Education, DeVry (DV) and ITT Educational Services (ESI).

Simply judging by analysts’ ratings and coverage in the financial media, these companies are still widely reviled, even if they did deliver a decent set of quarterly results. Of course, the real test for these firms is whether they’ve been able to stem the tide of shrinking enrollment and revenues. And frankly, there are only two or three companies that appear to be positioned for growth. (An acquisition by Capella Education (CPLA) explains why that firm is also expected to boost revenue in 2014.)

Yet shares may be rallying simply on expectations that the steady declines will end by next year and reverse course soon thereafter. After all, a key factor behind the negative enrollment trends has been a weak economy, as potential students question the wisdom of taking on debt at a time when the job market that will await them remains bleak.

What happens if the job market gets much stronger and the national unemployment rate moves toward 6%? A lot of these firms noted on their recent conference calls that rising employment levels has been a big boon for them in the past, and though the industry’s reputation has been tarnished, a degree from one of these for-profit institutions can still help students strengthen their standing with employers.

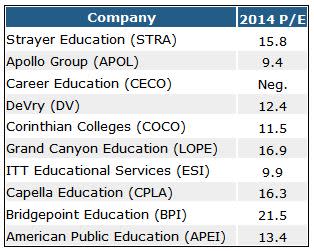

Let’s assume for the moment that these schools will hit bottom in 2014 and start to grow in 2015. Well, that would imply that profits in 2014 would mark a bottom for this cycle, and it’s helpful to gauge how these stocks are valued in the context of 2014 price-to-earnings (P/E) ratios. Viewed through that prism, these stocks are neither cheap nor expensive. But bulls would argue that they have ample room for earnings growth once enrollment trends start to build again.

Of course, in any industry that is still beset by shrinking revenues, it’s wise to focus on companies in the strongest financial position. After all, if industry conditions quickly worsen -- due to perhaps a fresh slowdown in the economy or even tougher congressional scrutiny -- then these companies might end up generating far smaller profits (or even losses) in 2014, relative to current expectations.

In effect, you want to invest only in companies with a high level of net cash and/or companies with high levels of net cash relative to their market value.

It’s quite unusual to find companies with more than 30% of their entire market value represented by net cash on the balance sheet, but some of these companies blow past that threshold. With companies like Apollo Group (APOL) boasting of more than $1 billion of net cash and a market value of $2.36 billion, why aren’t we seeing massive share buybacks? Well, we are. Apollo has bought back 64 million shares since 2005, shrinking the share count from 186 million to 122 million.

Of course, Apollo has nothing on Career Education (CECO), which is valued at just $207 million, despite having a net cash balance that is far higher. That disconnect is explained away by the fact that this company is on track to lose at least $1 a share in 2013 and again in 2014. Yet those views may be too harsh.

CECO recently brought in industry veteran Scott Steffey as the new CEO. He has extensive industry experience in both the for-profit (Strayer Education) and nonprofit (as vice chancellor for New York’s SUNY system) education sectors. He has quickly identified $25 million in cost savings and has laid out plans to boost enrollment. He has his work cut out for him, but with such a strong balance sheet behind him, the resources are in place for a turnaround.

Risks to Consider: This is an industry that may be approaching a bottom, but it’s not fully clear whether the current woes are largely due to a poor economic environment or the possibility that these companies have seen too much damage to survive. More than likely, half of these companies will go on to flourish with the right business models. But some of these companies may not even be around five years from now.

Action to Take --> This left-for-dead sector has suddenly become interesting again as some investors start to position for an eventual industry snapback. I am going to start tracking these companies a lot more closely, and they should be on your research lists as well.

Related Articles