Health Check: How Prudently Does Phoenix Global Resources (LON:PGR) Use Debt?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Phoenix Global Resources plc (LON:PGR) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Phoenix Global Resources

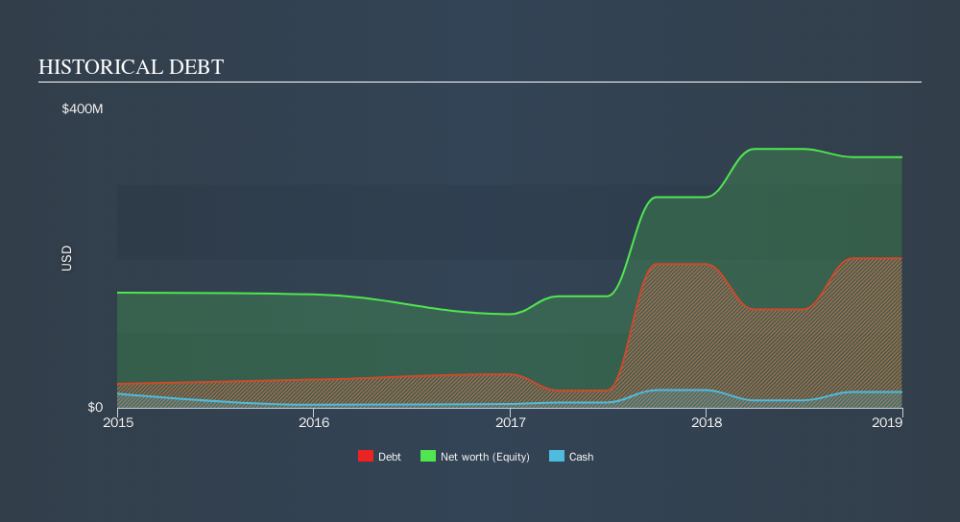

What Is Phoenix Global Resources's Net Debt?

The image below, which you can click on for greater detail, shows that at December 2018 Phoenix Global Resources had debt of US$200.3m, up from US$192.5m in one year. However, because it has a cash reserve of US$21.1m, its net debt is less, at about US$179.2m.

How Healthy Is Phoenix Global Resources's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Phoenix Global Resources had liabilities of US$119.1m due within 12 months and liabilities of US$254.8m due beyond that. Offsetting this, it had US$21.1m in cash and US$28.2m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$324.6m.

This is a mountain of leverage relative to its market capitalization of US$345.7m. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Phoenix Global Resources can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year Phoenix Global Resources managed to grow its revenue by 25%, to US$177m. With any luck the company will be able to grow its way to profitability.

Caveat Emptor

Despite the top line growth, Phoenix Global Resources still had negative earnings before interest and tax (EBIT), over the last year. Indeed, it lost a very considerable US$35m at the EBIT level. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. So we think its balance sheet is a little strained, though not beyond repair. However, it doesn't help that it burned through US$104m of cash over the last year. So in short it's a really risky stock. For riskier companies like Phoenix Global Resources I always like to keep an eye on whether insiders are buying or selling. So click here if you want to find out for yourself.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.