Here's Why Brüder Mannesmann (FRA:BMM) Has A Meaningful Debt Burden

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Brüder Mannesmann Aktiengesellschaft (FRA:BMM) makes use of debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Brüder Mannesmann

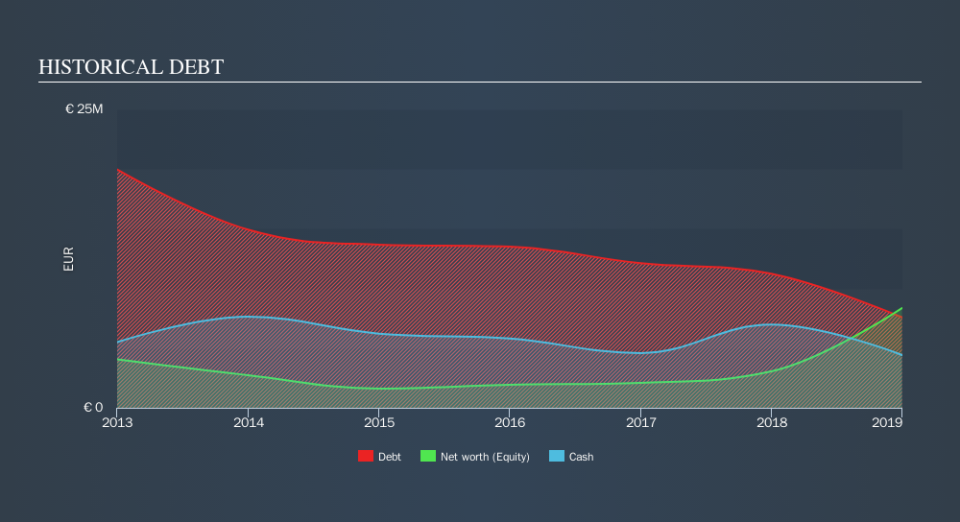

What Is Brüder Mannesmann's Debt?

As you can see below, Brüder Mannesmann had €7.57m of debt at December 2018, down from €11.2m a year prior. However, because it has a cash reserve of €4.43m, its net debt is less, at about €3.15m.

How Strong Is Brüder Mannesmann's Balance Sheet?

We can see from the most recent balance sheet that Brüder Mannesmann had liabilities of €7.48m falling due within a year, and liabilities of €20.4m due beyond that. On the other hand, it had cash of €4.43m and €2.27m worth of receivables due within a year. So it has liabilities totalling €21.2m more than its cash and near-term receivables, combined.

This deficit casts a shadow over the €6.53m company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. At the end of the day, Brüder Mannesmann would probably need a major re-capitalization if its creditors were to demand repayment.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Even though Brüder Mannesmann's debt is only 1.8, its interest cover is really very low at 1.1. This does suggest the company is paying fairly high interest rates. In any case, it's safe to say the company has meaningful debt. Shareholders should be aware that Brüder Mannesmann's EBIT was down 26% last year. If that decline continues then paying off debt will be harder than selling foie gras at a vegan convention. When analysing debt levels, the balance sheet is the obvious place to start. But it is Brüder Mannesmann's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Happily for any shareholders, Brüder Mannesmann actually produced more free cash flow than EBIT over the last three years. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Our View

On the face of it, Brüder Mannesmann's EBIT growth rate left us tentative about the stock, and its level of total liabilities was no more enticing than the one empty restaurant on the busiest night of the year. But at least it's pretty decent at converting EBIT to free cash flow; that's encouraging. Overall, it seems to us that Brüder Mannesmann's balance sheet is really quite a risk to the business. So we're almost as wary of this stock as a hungry kitten is about falling into its owner's fish pond: once bitten, twice shy, as they say. Over time, share prices tend to follow earnings per share, so if you're interested in Brüder Mannesmann, you may well want to click here to check an interactive graph of its earnings per share history.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.