Here's Why Diana Shipping (NYSE:DSX) Is Weighed Down By Its Debt Load

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Diana Shipping Inc. (NYSE:DSX) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Diana Shipping

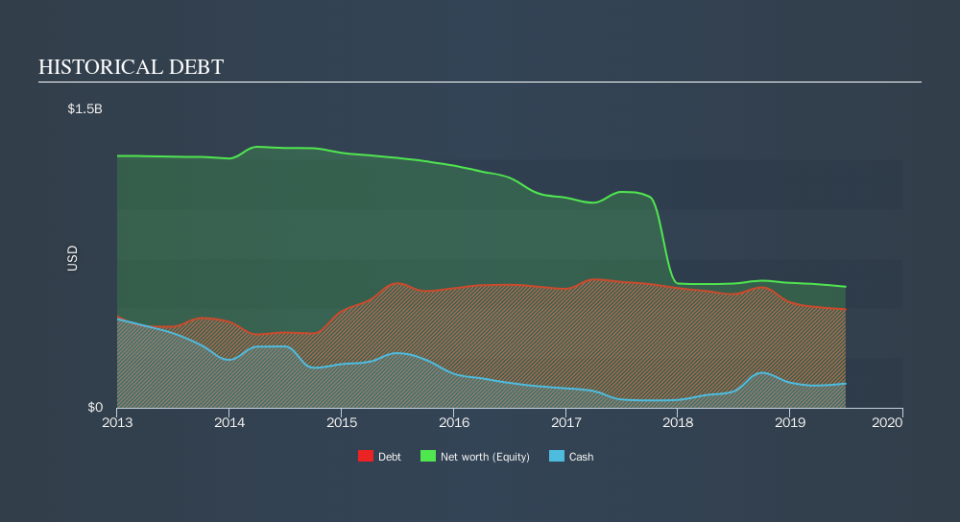

What Is Diana Shipping's Net Debt?

The image below, which you can click on for greater detail, shows that Diana Shipping had debt of US$495.0m at the end of June 2019, a reduction from US$571.9m over a year. On the flip side, it has US$121.4m in cash leading to net debt of about US$373.6m.

How Healthy Is Diana Shipping's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Diana Shipping had liabilities of US$125.2m due within 12 months and liabilities of US$395.7m due beyond that. Offsetting this, it had US$121.4m in cash and US$2.95m in receivables that were due within 12 months. So its liabilities total US$396.5m more than the combination of its cash and short-term receivables.

Given this deficit is actually higher than the company's market capitalization of US$325.5m, we think shareholders really should watch Diana Shipping's debt levels, like a parent watching their child ride a bike for the first time. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

While we wouldn't worry about Diana Shipping's net debt to EBITDA ratio of 4.3, we think its super-low interest cover of 2.3 times is a sign of high leverage. So shareholders should probably be aware that interest expenses appear to have really impacted the business lately. However, the silver lining was that Diana Shipping achieved a positive EBIT of US$54m in the last twelve months, an improvement on the prior year's loss. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Diana Shipping can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it is important to check how much of its earnings before interest and tax (EBIT) converts to actual free cash flow. Over the last year, Diana Shipping recorded negative free cash flow, in total. Debt is usually more expensive, and almost always more risky in the hands of a company with negative free cash flow. Shareholders ought to hope for and improvement.

Our View

On the face of it, Diana Shipping's level of total liabilities left us tentative about the stock, and its interest cover was no more enticing than the one empty restaurant on the busiest night of the year. Having said that, its ability to grow its EBIT isn't such a worry. We're quite clear that we consider Diana Shipping to be really rather risky, as a result of its balance sheet health. So we're almost as wary of this stock as a hungry kitten is about falling into its owner's fish pond: once bitten, twice shy, as they say. Over time, share prices tend to follow earnings per share, so if you're interested in Diana Shipping, you may well want to click here to check an interactive graph of its earnings per share history.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.