Here's Why Enservco (NYSEMKT:ENSV) Is Weighed Down By Its Debt Load

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Enservco Corporation (NYSEMKT:ENSV) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Enservco

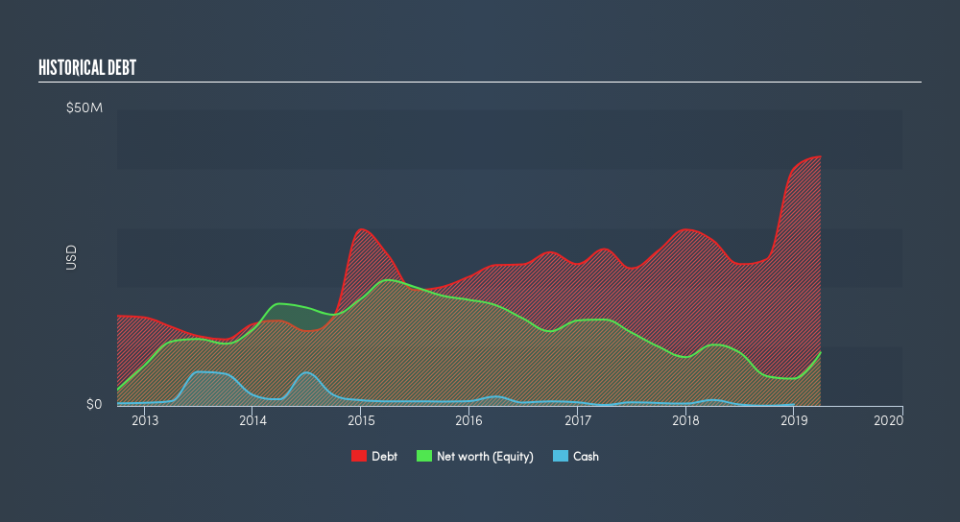

What Is Enservco's Net Debt?

The image below, which you can click on for greater detail, shows that at March 2019 Enservco had debt of US$42.0m, up from US$28.0m in one year. Net debt is about the same, since the it doesn't have much cash.

How Healthy Is Enservco's Balance Sheet?

We can see from the most recent balance sheet that Enservco had liabilities of US$9.40m falling due within a year, and liabilities of US$40.2m due beyond that. On the other hand, it had cash of US$257.0k and US$21.5m worth of receivables due within a year. So its liabilities total US$27.8m more than the combination of its cash and short-term receivables.

The deficiency here weighs heavily on the US$17.2m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we'd watch its balance sheet closely, without a doubt At the end of the day, Enservco would probably need a major re-capitalization if its creditors were to demand repayment.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Enservco shareholders face the double whammy of a high net debt to EBITDA ratio (6.1), and fairly weak interest coverage, since EBIT is just 0.24 times the interest expense. This means we'd consider it to have a heavy debt load. However, the silver lining was that Enservco achieved a positive EBIT of US$631k in the last twelve months, an improvement on the prior year's loss. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Enservco can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it is important to check how much of its earnings before interest and tax (EBIT) converts to actual free cash flow. Over the last year, Enservco saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

To be frank both Enservco's conversion of EBIT to free cash flow and its track record of staying on top of its total liabilities make us rather uncomfortable with its debt levels. Having said that, its ability to grow its EBIT isn't such a worry. Considering all the factors previously mentioned, we think that Enservco really is carrying too much debt. To us, that makes the stock rather risky, like walking through a dog park with your eyes closed. But some investors may feel differently. Given the risks around Enservco's use of debt, the sensible thing to do is to check if insiders have been unloading the stock.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.