Here's Why NexTier Oilfield Solutions (NYSE:NEX) Has A Meaningful Debt Burden

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that NexTier Oilfield Solutions Inc. (NYSE:NEX) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for NexTier Oilfield Solutions

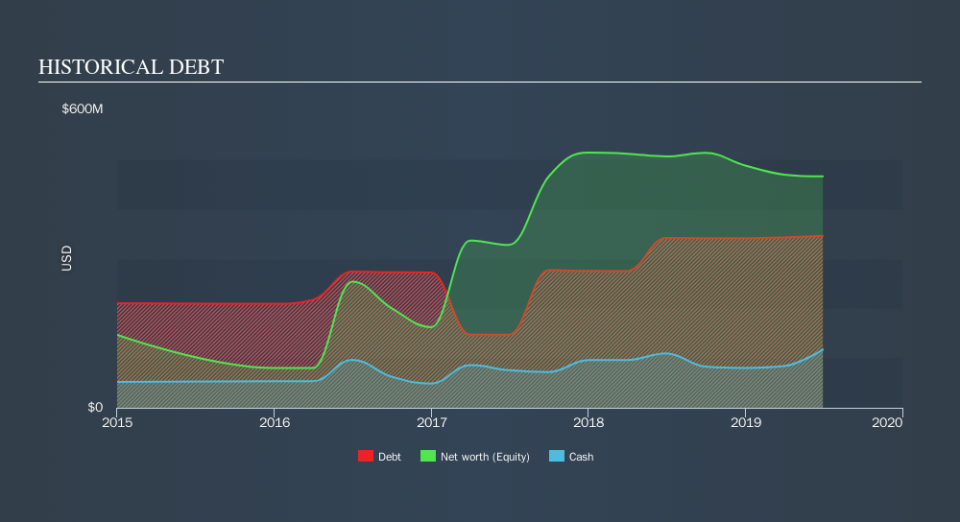

How Much Debt Does NexTier Oilfield Solutions Carry?

As you can see below, NexTier Oilfield Solutions had US$345.7m of debt, at June 2019, which is about the same the year before. You can click the chart for greater detail. On the flip side, it has US$117.1m in cash leading to net debt of about US$228.6m.

A Look At NexTier Oilfield Solutions's Liabilities

We can see from the most recent balance sheet that NexTier Oilfield Solutions had liabilities of US$223.5m falling due within a year, and liabilities of US$376.1m due beyond that. Offsetting these obligations, it had cash of US$117.1m as well as receivables valued at US$199.1m due within 12 months. So its liabilities total US$283.4m more than the combination of its cash and short-term receivables.

This is a mountain of leverage relative to its market capitalization of US$465.2m. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

NexTier Oilfield Solutions has a very low debt to EBITDA ratio of 0.69 so it is strange to see weak interest coverage, with last year's EBIT being only 2.1 times the interest expense. So while we're not necessarily alarmed we think that its debt is far from trivial. Importantly, NexTier Oilfield Solutions's EBIT fell a jaw-dropping 66% in the last twelve months. If that decline continues then paying off debt will be harder than selling foie gras at a vegan convention. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine NexTier Oilfield Solutions's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we always check how much of that EBIT is translated into free cash flow. Looking at the most recent two years, NexTier Oilfield Solutions recorded free cash flow of 20% of its EBIT, which is weaker than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

To be frank both NexTier Oilfield Solutions's interest cover and its track record of (not) growing its EBIT make us rather uncomfortable with its debt levels. But on the bright side, its net debt to EBITDA is a good sign, and makes us more optimistic. Overall, we think it's fair to say that NexTier Oilfield Solutions has enough debt that there are some real risks around the balance sheet. If everything goes well that may pay off but the downside of this debt is a greater risk of permanent losses. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of NexTier Oilfield Solutions's earnings per share history for free.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.