Here's Why You Should Retain Globus Medical (GMED) for Now

Globus Medical, Inc. GMED is gaining from product development and strength in the U.S. Spine business. The company ended the second quarter of 2021 with better-than-expected results. The company’s new surgical milestone for ExcelsiusGPS Robotic Navigation system buoys optimism. However, headwinds from Japan partially hampered the international spinal implant business. Escalating costs and stiff competition do not bode well either.

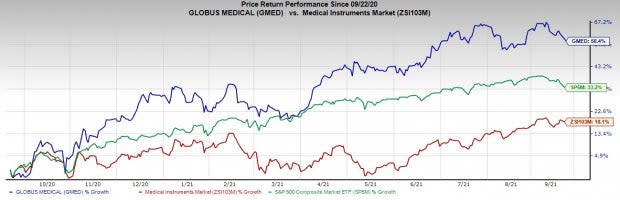

Over the past year, this Zacks Rank #3 (Hold) stock has charted a solid trajectory, appreciating 56.4% compared with 18.1% growth of the industry and 33.2% rise of the S&P 500 composite.

The renowned medical device company has a market capitalization of $7.92 billion. Its earnings surpassed the Zacks Consensus Estimate by 24.4%.

Over the past five years, the company has seen 5.5% growth, ahead of the industry’s 2.6% rise and the S&P 500’s 2.8% increase. The long-term expected growth rate is estimated at 10.6%, comparing with the industry’s growth expectation of 18.6% and the S&P 500’s estimated 11.3% growth.

Image Source: Zacks Investment Research

Let’s delve deeper.

Factors at Play

Q2 Upsides: Globus Medical exited the second quarter of 2021 with better-than-expected earnings and revenues despite pandemic-related adversities. The robust top-line growth along with improvements in the company’s U.S. revenues led by the U.S. Spine and Enabling Technologies businesses is impressive. Expansion in gross margin looks encouraging as well. Further, the company has raised its full-year 2021 guidance, which is indicative that this bullish trend will continue.

Steady Pace of Product Development: Globus Medical’s consistent efforts to innovate, research and develop are in line with its business strategy to focus on integrated product development. The company’s ExcelsiusGPS Robotic Navigation system was reported to have been used in more than 20,000 spine procedures in July 2021. In April 2021, the company launched CREO ONE -- the market’s first robotic screw designed for spine surgery with ExcelsiusGPS. Continued robust demand for various products in the HEDRON line of 3D-printed interbody spacers and SABLE raises our optimism. At present, the company is awaiting 510(k) clearance for its Excelsius 3D imaging system.

Spine Arm Grows Domestically: We are upbeat about Globus Medical’s solid second-quarter performance in the U.S. Spine business, which continues to capture significant market share, growing almost 30%. The company’s U.S. revenues grew 71.9% in the quarter, led by strength in the U.S. Spine business. The key factors driving growth in this segment include pull-through from robotics, contributions from product introductions and resurgence in the biologics business. The company has also been witnessing strong adoption of single-position lateral and prone lateral procedures, which are enhanced by the capabilities of ExcelsiusGPS.

Downsides

Escalating Costs: During the second quarter of 2021, Globus Medical witnessed a 26.1% rise in cost of goods sold. Meanwhile, selling, general and administrative expenses rose 34% in the quarter. These escalating expenses are building pressure on the company’s bottom line.

International Spinal Implant Business Hurt: Globus Medical’s international spinal implant business was partially affected by headwinds in Japan in the second quarter of 2021. The primary reasons for the decline were higher planned depreciation expenses related to instruments and cases, slightly higher product costs driven by the mix of sales, and additional inventory reserve expenses.

Competitive Landscape: Globus Medical faces stiff competition in the orthopedic industry from MedTech biggies like Zimmer Biomet Holdings, Inc. ZBH and Smith+Nephew SNN, among others. The company needs to constantly introduce or acquire new products to withstand the competitive pressure and maintain its market share.

Estimate Trend

Globus Medical has been witnessing a positive estimate revision trend for earnings in 2021. Over the past 90 days, the Zacks Consensus Estimate for its earnings has moved 5.8% north to $2.

The Zacks Consensus Estimate for its third-quarter 2021 revenues is pegged at $229.01 million, suggesting a 5.97% rise from the year-ago reported number.

Key Picks

A better-ranked stock from the Medical-Instruments industry is IDEXX Laboratories, Inc. IDXX.

IDEXX, which carries a Zacks Rank #2 (Buy), has a long-term earnings growth rate of 19.9%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Smith & Nephew SNATS, Inc. (SNN) : Free Stock Analysis Report

IDEXX Laboratories, Inc. (IDXX) : Free Stock Analysis Report

Globus Medical, Inc. (GMED) : Free Stock Analysis Report

Zimmer Biomet Holdings, Inc. (ZBH) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research