Here's Why You Should Stay Invested in Hanover Insurance (THG)

The Hanover Insurance Group’s THG focus on driving growth in the most profitable Core Commercial and Specialty segments, stable retention, better pricing and strong market presence along with favorable growth make it worth retaining in one’s portfolio.

THG has a solid track record of beating earnings estimates in the last 13 quarters.

Northbound Estimate Revision

The Zacks Consensus Estimate for 2022 and 2023 earnings has moved 1.1% and 0.1% north, respectively, in the past 30 days, reflecting analyst optimism.

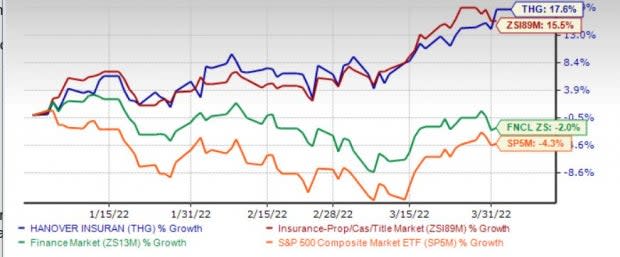

Zacks Rank & Price Performance

Hanover Insurance Group currently carries a Zacks Rank #3 (Hold). Year to date, the stock has gained 17.6%, outperforming the industry’s increase of 15.5%. The Finance sector and the S&P 500 composite index have lost 2% and 4.3%, respectively, in the said time frame.

Image Source: Zacks Investment Research

Growth Projections

The Zacks Consensus Estimate for THG’s 2022 earnings is pegged at $10.53, indicating a 20.6% increase from the year-ago reported figure on 6.9% higher revenues of $5.5 billion. The consensus estimate for 2023 earnings is pegged at $11.38, indicating an 8.1% increase from the year-ago reported figure on 5.5% higher revenues of $5.8 billion.

The long-term earnings growth rate is currently pegged at 13.8%, better than the industry average of 12.2%. THG estimates the bottom line to grow between 12% and 13% over the long term.

Return on Equity

Return on equity in the trailing 12 months was 10.2%, better than the industry average of 5.9%. This highlights efficiency in utilizing shareholders’ fund. THG estimates an operating return on equity of 14% in the long run, banking on improved rates and cost management.

Business Tailwinds

Hanover Insurance has evolved into a balanced, small/middle market-focused commercial and personal lines carrier. The company looks to be the premier P&C franchise in the independent agency channel.

Hanover Insurance expects to deliver mid-single-digit growth in target returns in Personal Lines in 2022 as it intends to increase prices in both home and auto.

Rate increases and the successful launch of TAP sales should drive Commercial Lines revenues. Hanover Insurance believes that its market-leading capabilities, operating model and portfolio performance should allow it to benefit in the high-margin $105 billion small commercial market segment.

Commercial Lines loss ratio is expected to improve in 2022 given the rate increases implemented in 2021. The consolidated expense ratio is projected to improve 20 basis points in 2022 to 31.1%.

Its focus on pricing segmentation and mix management and emphasis on growth in target states, product lines and industry classes in the middle market bode well for THG.

As digitalization ramps up across the insurance industry, this insurer is no exception. THG continues to invest in technology to upgrade the front-end capabilities.

All these together should help THG deliver the higher end of mid-single digits net written premium growth in 2022 and a five-year CAGR of more than 7% to $7 billion.

The company has a favorable VGM Score of A.

Solid Dividend History

The company has been hiking dividends for the last 16 years, in addition to paying special dividends. THG’s dividend witnessed an 11-year CAGR of 10.5%. Its yield of 2.2% is better than the industry average of 0.3%.

Stocks to Consider

Some better-ranked stocks from the property and casualty insurance sector are Kinsale Capital Group KNSL, United Fire Group UFCS and American Financial Group AFG. While Kinsale Capital and United Fire currently sport a Zacks Rank #1(Strong Buy), American Financial Group carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Kinsale Capital’s earnings surpassed estimates in each of the last four quarters, the average beat being 32.04%. In the past year, Kinsale Capital has rallied 36.1%.

The Zacks Consensus Estimate for KNSL’s 2022 and 2023 earnings has moved 5.9% and 8.2% north, respectively, in the past 60 days.

United Fire’s earnings surpassed estimates in each of the last four quarters, the average earnings surprise being 275.45%. In the past year, UFCS stock has declined 7.7%.

The Zacks Consensus Estimate for UFCS’ 2022 and 2023 earnings has moved 122.2% and 76.9% north, respectively, in the past 60 days.

The bottom line of American Financial surpassed earnings estimates in each of the last four quarters, the average being 39.58%. In the past year, the insurer has rallied 28.8%.

The Zacks Consensus Estimate for American Financial’s 2022 and 2023 earnings has moved 3.3% and 8.2% north, respectively, in the past 60 days.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

American Financial Group, Inc. (AFG) : Free Stock Analysis Report

The Hanover Insurance Group, Inc. (THG) : Free Stock Analysis Report

United Fire Group, Inc (UFCS) : Free Stock Analysis Report

Kinsale Capital Group, Inc. (KNSL) : Free Stock Analysis Report

To read this article on Zacks.com click here.