Here's Why We Think Bel Fuse (NASDAQ:BELF.A) Is Well Worth Watching

The excitement of investing in a company that can reverse its fortunes is a big draw for some speculators, so even companies that have no revenue, no profit, and a record of falling short, can manage to find investors. Sometimes these stories can cloud the minds of investors, leading them to invest with their emotions rather than on the merit of good company fundamentals. Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

Despite being in the age of tech-stock blue-sky investing, many investors still adopt a more traditional strategy; buying shares in profitable companies like Bel Fuse (NASDAQ:BELF.A). Now this is not to say that the company presents the best investment opportunity around, but profitability is a key component to success in business.

Check out our latest analysis for Bel Fuse

Bel Fuse's Improving Profits

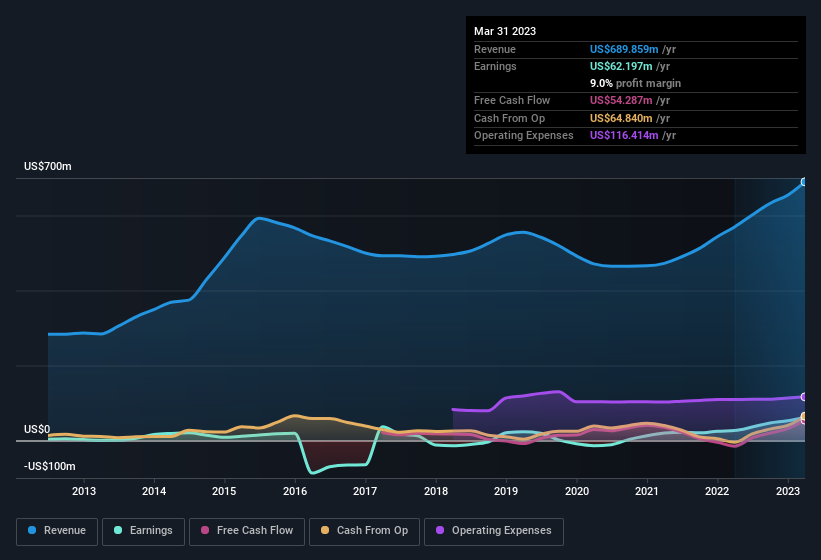

Bel Fuse has undergone a massive growth in earnings per share over the last three years. So much so that this three year growth rate wouldn't be a fair assessment of the company's future. So it would be better to isolate the growth rate over the last year for our analysis. Impressively, Bel Fuse's EPS catapulted from US$2.14 to US$4.87, over the last year. It's a rarity to see 127% year-on-year growth like that.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. Bel Fuse shareholders can take confidence from the fact that EBIT margins are up from 6.1% to 13%, and revenue is growing. That's great to see, on both counts.

In the chart below, you can see how the company has grown earnings and revenue, over time. For finer detail, click on the image.

You don't drive with your eyes on the rear-view mirror, so you might be more interested in this free report showing analyst forecasts for Bel Fuse's future profits.

Are Bel Fuse Insiders Aligned With All Shareholders?

It's said that there's no smoke without fire. For investors, insider buying is often the smoke that indicates which stocks could set the market alight. This view is based on the possibility that stock purchases signal bullishness on behalf of the buyer. However, small purchases are not always indicative of conviction, and insiders don't always get it right.

The good news is that Bel Fuse insiders spent a whopping US$1.8m on stock in just one year, without so much as a single sale. Knowing this, Bel Fuse will have have all eyes on them in anticipation for the what could happen in the near future. It is also worth noting that it was company insider Christopher Bennett who made the biggest single purchase, worth US$1.0m, paying US$31.95 per share.

The good news, alongside the insider buying, for Bel Fuse bulls is that insiders (collectively) have a meaningful investment in the stock. To be specific, they have US$38m worth of shares. This considerable investment should help drive long-term value in the business. As a percentage, this totals to 6.4% of the shares on issue for the business, an appreciable amount considering the market cap.

Shareholders have more to smile about than just insiders adding more shares to their already sizeable holdings. The cherry on top is that the CEO, Daniel Bernstein is paid comparatively modestly to CEOs at similar sized companies. The median total compensation for CEOs of companies similar in size to Bel Fuse, with market caps between US$200m and US$800m, is around US$2.5m.

The CEO of Bel Fuse only received US$825k in total compensation for the year ending December 2022. That looks like a modest pay packet, and may hint at a certain respect for the interests of shareholders. While the level of CEO compensation shouldn't be the biggest factor in how the company is viewed, modest remuneration is a positive, because it suggests that the board keeps shareholder interests in mind. It can also be a sign of a culture of integrity, in a broader sense.

Is Bel Fuse Worth Keeping An Eye On?

Bel Fuse's earnings have taken off in quite an impressive fashion. To make matters even better, the company insiders who know the company best have put their faith in the its future and have been buying more stock. This quick rundown suggests that the business may be of good quality, and also at an inflection point, so maybe Bel Fuse deserves timely attention. However, before you get too excited we've discovered 1 warning sign for Bel Fuse that you should be aware of.

There are plenty of other companies that have insiders buying up shares. So if you like the sound of Bel Fuse, you'll probably love this free list of growing companies that insiders are buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here