Himax (HIMX) Q1 Prelim Results Indicate Strength in IC Demand

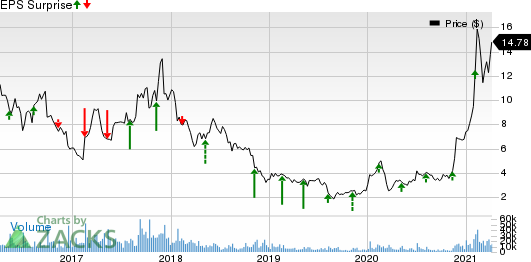

Shares of Himax Technologies HIMX were up 12.2% to hit $16.20 in the intraday trading session, eventually closing at $14.78 (up more than 2%) on Apr 7.

The surge was led by encouraging preliminary first-quarter 2021 results. The company anticipates revenues to be $309 million, indicating sequential growth of 12.1%, much higher than a rough 5-10% rise guided on Feb 4.

Revenues are now expected to surge 67.4% year over year on a strong momentum across all major business segments.

Moreover, Himax projects gross margin to be 40.2%, surpassing the company's original guidance of 37-38%, hinting at an expansion of 900 basis points (bps) sequentially and a 17.5% increase from the year-ago reported quarter.

Further, earnings on non-IFRS basis are expected to be 38.4 cents per ADS, much better than the previous forecast range of 30.1 cents to 34.1 cents. This also indicates 94.9% sequential growth and a significant rise from 2.2 cents per ADS in the prior-year quarter.

Notably, Himax stock has gained a whopping 375.2% in the past year, outperforming the industry’s rally of 91.4%.

Earnings Estimate Witness Upward Revision

The Zacks Consensus Estimate for the March-quarter earnings currently stands at 35 cents per share, revised upward by 9.4% over the past seven days and further suggests 1,650% growth from the figure reported in the year-earlier quarter.

Moreover, the consensus mark for revenues is currently pegged at $296.47 million, indicating an improvement of 60.6% from the number reported in the comparable quarter last year.

Key Factors Likely to Have Favored Q1 Performance

Himax’s first-quarter preliminary results reflect benefits from a rebound in the smartphone market, which led to an uptick in demand for its smartphone TDDI solutions, AMOLED driver ICs and PMIC for 5G smartphones.

Solid demand for high-end monitor and new-generation low-power notebook owing to the coronavirus-led work-from-home and online-learning wave is expected to have triggered the need for Himax’s display driver ICs and timing controllers, which in turn, might get reflected on the first-quarter top line. Robust demand for tablets also remained a key catalyst.

Moreover, improving display driver demand, diversified customer base and a strong partner ecosystem are likely to have boosted the company’s revenue base. Notably, the entity is a dominant name in the TFT LCD display driver and timing-controller IC markets.

Recovery in the automotive sector spurred demand for automotive driver ICs, which positioned Himax well to drive its gross margins and revenues.

Increasing usage of WLO in technologies across nanoimprinting manufacturing and diffraction optics design is a tailwind.

Himax Technologies, Inc. Price and EPS Surprise

Himax Technologies, Inc. price-eps-surprise | Himax Technologies, Inc. Quote

Surging demand for 3D decoder ASICs in 3D Sensing across smartphones, smart door lock, facial recognition-based e-payment, business access control and biomedical inspection device holds promise.

Strength in Himax’s WiseEye technology across notebook, TV, doorbell, door lock and air conditioner end-markets is noteworthy. Also, robust adoption of the company’s 8K TV display drivers and timing controller ICs bodes well.

Momentum for its CMOS image sensors across IP camera and notebook is expected to have contributed to first-quarter revenues. Markedly, Himax offers 2-in-1 CMOS image sensor, which supports RGB mode for video conferencing and an ultralow power AI mode for facial recognition. The solution is increasingly being utilized in the latest slim laptops.

Management anticipates robust demand momentum in the first quarter to continue through the second quarter and favor financial performance amid global semiconductor shortage, which shows no signs of fading.

Zacks Rank & Other Key Picks

Himax currently carries a Zacks Rank #2 (Buy). Some other top-ranked stocks in the broader sector are NVIDIA Corporation NVDA, Agilent Technologies, Inc. A and Micron Technology MU, all flaunting a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Long-term earnings growth rate for Micron, NVIDIA and Agilent is currently pegged at 15.66%, 12.55%, and 9%, respectively.

Time to Invest in Legal Marijuana

If you’re looking for big gains, there couldn’t be a better time to get in on a young industry primed to skyrocket from $17.7 billion back in 2019 to an expected $73.6 billion by 2027.

After a clean sweep of 6 election referendums in 5 states, pot is now legal in 36 states plus D.C. Federal legalization is expected soon and that could be a still greater bonanza for investors. Even before the latest wave of legalization, Zacks Investment Research has recommended pot stocks that have shot up as high as +285.9%

You’re invited to check out Zacks’ Marijuana Moneymakers: An Investor’s Guide. It features a timely Watch List of pot stocks and ETFs with exceptional growth potential.

Today, Download Marijuana Moneymakers FREE >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Agilent Technologies, Inc. (A) : Free Stock Analysis Report

To read this article on Zacks.com click here.