The Federal Reserve appears poised to raise U.S. overnight interest rates on Wednesday, but many investors believe that they may be driving blind as they move forward.

The central bank’s quantitative easing programs have distorted traditional investment metrics and created an environment where no one is quite sure how to read the market. These distortions have been exacerbated by market factors, such as Amazon (AMZN) and other tech companies’ consistent downward pressure on prices.

Traditionally correlated dynamics like low unemployment and rising wages and inflation pressures have lessened significantly. Other indicators that in years past would have signaled alerts to buy or sell are now uncertain, confusing investors and likely central bankers, analysts say.

“The Fed is working without full information right now,” said Rebecca Patterson, chief investment officer at asset manager Bessemer Trust. “It’s not a new phenomenon, but it’s relatively new, some of the deflationary forces we’re seeing [from the tech companies], and how does the Fed incorporate that in their analytics? How do you forecast the pace of change that’s going to happen going forward? No one knows.”

Some have said they expect the Fed’s moves to raise rates and pare back its balance sheet will push the economy into recession, with the U.S. already near the top of the economic cycle. However, given the Fed’s unprecedented actions following the financial crisis of 2008, a growing chorus of market participants say trying to read the market is now a fool’s errand.

‘The whole playing field has been skewed’

“If the Fed wasn’t involved, I would very easily say stocks are wildly overpriced and equity markets are going to crash,” said Christopher Irons, founder of Quoth the Raven Research. “The sentiment for equities right now would be best described as confusion. Certainly, that’s my sentiment.”

Irons says the Fed’s build-up of more than $4 trillion in bond holdings, its quantitative easing program in concert with 0% interest rates have distorted the market.

Because of central banks’ — the Fed as well as the European Central Bank, Bank of Japan and others — weighty intervention in the market, typical indicators, such as the possibility of the U.S. Treasury yield curve inverting, can’t be understood the same way they were in previous years, Irons said. “The whole playing field has been skewed, so I’m reluctant to make a guess as to what means what anymore.”

While yield curve inversions have happened multiple times, often but not always preceding a recession, John Davi, chief investment officer at Astoria Portfolio Advisors, said he has started to de-risk his holdings because of much more rare market happenings.

“In December we started shifting the portfolio because there were things that happened that I’ve never seen in my 20-year career or read in books that have 100 years worth of data,” Davi said.

Unusual activity

Mark Yusko, chief executive and chief investment officer at Morgan Creek Capital Management, said he is now 50% below MSCI’s All-Country World Index (ACWI) weight on U.S. equities, expecting commodities to “crush” stocks and bonds over the coming decade.

Both Yusko and Davi, who debated their views recently at the Inside Smart Beta Conference in New York, said the market in 2017 was awash in strikingly unusual activity.

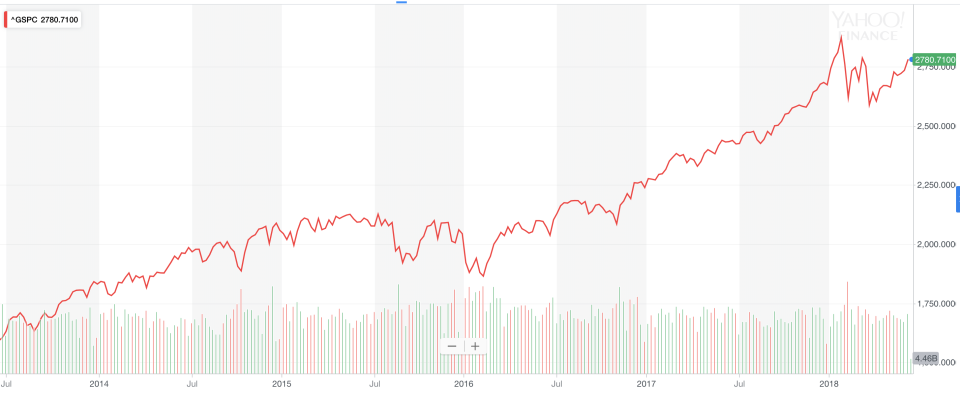

The S&P 500 (^GSPC) last year boasted a 3.5 sharpe ratio — a popular metric for judging returns in which a higher number signals better returns with less risk — and Davi pointed out MSCI’s 70% ACWI/30% Bloomberg Barclays Bond Index sported a 6 sharpe ratio. Historically, the S&P has carried a sharpe ratio of 0.7, according to Vincent Deluard of brokerage INTL FCStone.

Further, 2017 was the first year that MSCI’s ACWI index rose every single month in the history of the index. The S&P rose for 15 straight months, went the longest period in its history without a 3% pullback and both the Dow (^DJI) and S&P had their smallest levels of absolute daily change since 1964, according to the Wall Street Journal’s Market Data Group.

There’s also the matter of unconventional U.S. fiscal policy from the administration of President Donald Trump. The recently passed $1.5 trillion tax cut and $300 billion increase in federal spending the president signed last year add stimulus to a market already operating near the peak of its expansion. Typically when countries increase spending it’s to offset an economic downturn and usually not when the country is more than $20 trillion in debt.

All of that puts an even brighter spotlight on the Fed’s meeting this week, which will be picked apart for guidance and for signs of a possible policy misstep.

“They have armies of PhDs, but at the end of the day they are making educated guesses so … there is room for policy error from the Fed,” said Bessemer Trust’s Patterson. “It’s important to think about when we listen to the Fed – they’re making their best educated guess.”

—

Dion Rabouin is a markets reporter for Yahoo Finance. Follow him on Twitter: @DionRabouin.

Follow Yahoo Finance on Facebook, Twitter, Instagram, and LinkedIn.

Read more:

Fund managers warn a downturn is coming and ‘it’s going to be pretty ugly’

Investors flee emerging markets at the fastest pace since November 2016