Investors Still Waiting For A Pull Back In CanWel Building Materials Group Ltd. (TSE:CWX)

Want to participate in a short research study? Help shape the future of investing tools and earn a $40 gift card!

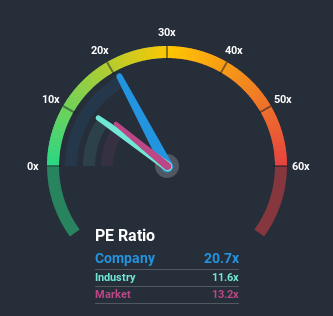

When close to half the companies in Canada have price-to-earnings ratios (or "P/E's") below 13x, you may consider CanWel Building Materials Group Ltd. (TSE:CWX) as a stock to avoid entirely with its 20.7x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

While the market has experienced earnings growth lately, CanWel Building Materials Group's earnings have gone into reverse gear, which is not great. It might be that many expect the dour earnings performance to recover substantially, which has kept the P/E from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

View our latest analysis for CanWel Building Materials Group

Where Does CanWel Building Materials Group's P/E Sit Within Its Industry?

An inspection of average P/E's throughout CanWel Building Materials Group's industry may help to explain its particularly high P/E ratio. The image below shows that the Trade Distributors industry as a whole has a P/E ratio similar to the market. So it appears the company's ratio isn't really influenced by these industry numbers currently. Some industry P/E's don't move around a lot and right now most companies within the Trade Distributors industry should be getting restrained. Nonetheless, the greatest force on the company's P/E will be its own earnings growth expectations.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on CanWel Building Materials Group.

Is There Enough Growth For CanWel Building Materials Group?

The only time you'd be truly comfortable seeing a P/E as steep as CanWel Building Materials Group's is when the company's growth is on track to outshine the market decidedly.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 20%. As a result, earnings from three years ago have also fallen 70% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Shifting to the future, estimates from the seven analysts covering the company suggest earnings growth will be highly resilient over the next year growing by 15%. That would be an excellent outcome when the market is expected to decline by 7.8%.

With this information, we can see why CanWel Building Materials Group is trading at such a high P/E compared to the market. At this time, shareholders aren't keen to offload something that is potentially eyeing a much more prosperous future.

The Key Takeaway

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

As we suspected, our examination of CanWel Building Materials Group's analyst forecasts revealed that its superior earnings outlook against a shaky market is contributing to its high P/E. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. Our only concern is whether its earnings trajectory can keep outperforming under these tough market conditions. Otherwise, it's hard to see the share price falling strongly in the near future under the current growth expectations.

We don't want to rain on the parade too much, but we did also find 3 warning signs for CanWel Building Materials Group (1 makes us a bit uncomfortable!) that you need to be mindful of.

If you're unsure about the strength of CanWel Building Materials Group's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.