Jim Cramer Gives These 2 Stocks His Stamp of Approval

Markets are rewriting the same story we’ve been looking at all summer – investors are skittish, and wary of the headwinds. Those headwinds are enough to spook even the most experienced traders. High inflation is making everyone nervous, the Fed’s turn to higher interest rates – to combat inflation – brings with it the risk of recession, and macro data on the economy is starting to show declines in the housing markets and consumer confidence and spending. As if all that wasn’t enough, now add in the national election coming up on November 8, and it’s a recipe for trouble.

But as usual, with trouble comes opportunity. Jim Cramer, the well-known host of CNBC’s ‘Mad Money’ program, has never been one to shy away from a turbulent market, and he has a knack for finding solid stocks that can support an investment portfolio pending better times down the road. Right now, Cramer sees the trading world in something of a holding pattern, saying, “The market needs time to adjust, and the Fed doesn’t want to rock the boat too aggressively right before the election.”

Cramer is well-known for the ‘lightning round’ feature on his program, where he gives his short takes to callers’ stock questions. We’ve used the TipRanks platform to pull up the details on a couple of his recent bullish calls. Let’s take a look at the data and the analyst commentary, and find out why Cramer thinks lightning will strike.

State Street Corporation (STT)

Boston-based State Street makes a unique boast: it is the second-oldest bank in the United States, tracing its roots back to 1792. Today, with $3.3 trillion in total assets under management, along with $35.7 trillion in assets under custody, the company is also one of the largest asset managers on the global scene. State Street reported $11.16 billion in revenues last year, and is well on its way to beating that total this year.

On October 18, the company reported its results for 3Q22, showing $2.96 billion at the top line, along with net income of $690 million. STT’s diluted EPS came in at $1.80. State Street reported decreases in its overall fee revenues, including servicing fees and management fees; these were partly offset by increases in fees for forex trading, securities finance, and software and processing. Net interest income was up 36%. These results were considered mostly in-line with expectations.

That performance is holding up a dividend of 63 cents per common share. At an annualized rate of $2.52, the dividend is yielding 3.47%.

Looking at State Street’s financial performance compared to its share price – the latter is down 20% so far this year – Jim Cramer says of STT: “I think State Street down here at this level is a terrific buy.”

5-star analyst Stephen Biggar, covering State Street from Argus, agrees that the stock is one to buy. Laying out the case, he writes, “We expect State Street to benefit from several long-term earnings drivers. First, asset managers are facing cost pressures that will likely lead to the further outsourcing of back-office operations. Second, the company has scale advantages, and should see improved operating leverage over time. Third, asset managers must focus on their core competency (managing money) and not on more-mundane servicing tasks..."

"We believe that recent weakness provides a favorable entry point for the high-quality STT shares," Biggar summed up.

Standing squarely in the bull camp, Biggar rates STT a Buy, and his $88 price target suggests an upside of ~21% over the coming year. (To watch Biggar’s track record, click here)

It would seem that, for the most part, Wall Street is in agreement with both Biggar and Cramer. The 10 recent analyst reviews include 7 Buys and 3 Holds, for a Moderate Buy consensus rating, and the $79.60 average price target implies ~10% gain from the current trading price of $72.48. (See STT stock forecast on TipRanks)

Cummins, Inc. (CMI)

The second stock we’ll look at is Cummins, a major name in engineering, best known as a supplier of engines and ancillary components for heavy industrial vehicles. Cummins operates through several segments, offering engines, engine and drive train components, and power generation systems. The company has a global presence, with over 9,000 locations worldwide, and offers full mechanical and maintenance support to its customers.

A few numbers will give the scale of Cummins’ ops. The company has more than 58,000 employees, and its revenues are in the tens of billions. The top line hit $19.8 billion in 2020, and in 2021 that rose to $24 billion. So far this year, Cummins has reported results for Q1 and Q2; its first half revenue is up 6.3% from 1H21.

Digging into the Q2 report, we find that Cummins had earnings of $702 million, with a diluted EPS of $4.94. International revenues slipped 2% in Q2, but that was more than compensated by North American revenues, which grew 15%. Overall, Cummins reported a top line of $6.6 billion for the quarter. This was up 8% year-over-year, and was in-line with the company’s overall forward guidance; Cummins is expecting a full-year revenue gain of 8% over 2021.

Looking at Cummins, Jim Cramer is impressed by the company’s status as a stalwart of the industrial engineering world, an essential sector of the modern economy. He writes of Cummins, “I think Cummins is a great company. This is the kind of stock that is working right now in this environment. It doesn’t really get hurt much by rates. It’s got superior products [that] it’s selling all over the world. I like Cummins.”

Cowen analyst Matt Elkot would agree. The 5-star analyst covers CMI, and looking at the company, ahead of Q3 earnings (November 3), he sees several reasons for optimism going forward.

“We are positive on CMI into the print... Chips have gotten a bit more stable, and the company has become a little less worried on the issue... Demand environment remains strong. September truck orders came in a lot higher than expected... Backlogs for medium-duty trucks remain robust, and demand may last longer than demand for heavy-duty trucks," Elkot noted.

To this end, Elkot gives Cummins an Outperform (i.e. Buy) rating, and backs it with a $267 price target that indicates potential for a 13.5% share growth by the end of next year. (To watch Elkot’s track record, click here)

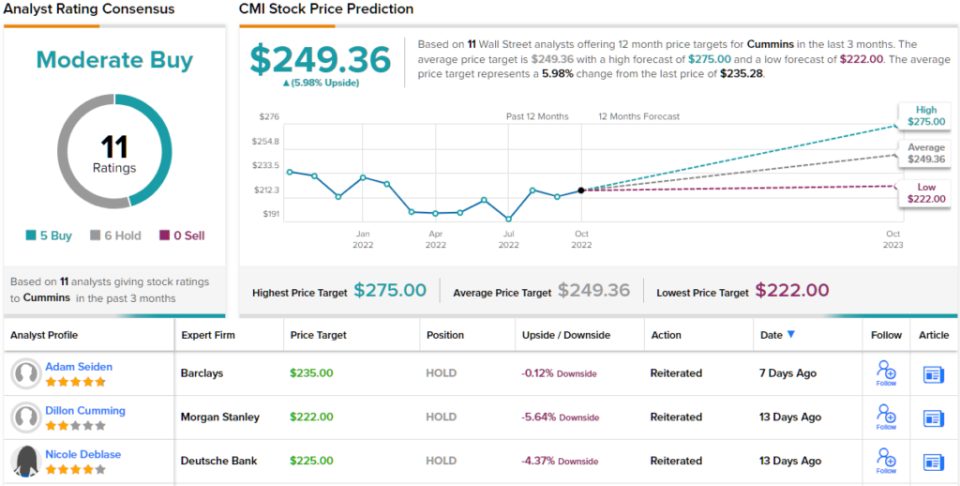

What does the rest of the Street think? Looking at the consensus breakdown, opinions from other analysts are more spread out. The stock has 11 recent analyst reviews, breaking down to 5 Buys and 6 Holds for a Moderate Buy consensus view. With an average price target of $249.36 and a trading price of $235.28, Cummins has a one-year potential upside of about 6%. (See CMI stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.