Need To Know: Analysts Are Much More Bullish On Gambling.com Group Limited (NASDAQ:GAMB) Revenues

Celebrations may be in order for Gambling.com Group Limited (NASDAQ:GAMB) shareholders, with the analysts delivering a significant upgrade to their statutory estimates for the company. The revenue forecast for next year has experienced a facelift, with analysts now much more optimistic on its sales pipeline.

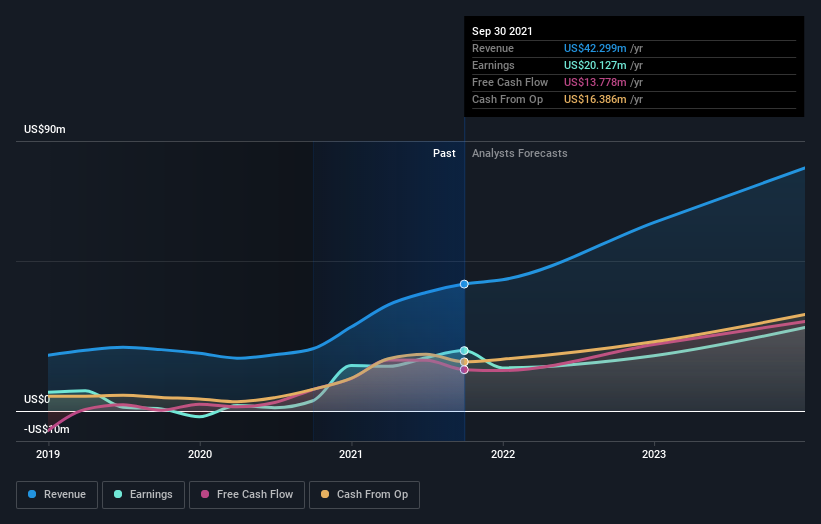

Following the upgrade, the most recent consensus for Gambling.com Group from its three analysts is for revenues of US$71m in 2022 which, if met, would be a major 69% increase on its sales over the past 12 months. Statutory earnings per share are supposed to drop 13% to US$0.51 in the same period. Prior to this update, the analysts had been forecasting revenues of US$63m and earnings per share (EPS) of US$0.50 in 2022. There's clearly been a surge in bullishness around the company's sales pipeline, even if there's no real change in earnings per share forecasts.

See our latest analysis for Gambling.com Group

Analysts increased their price target 6.8% to US$15.67, perhaps signalling that higher revenues are a strong leading indicator for Gambling.com Group's valuation. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. There are some variant perceptions on Gambling.com Group, with the most bullish analyst valuing it at US$16.00 and the most bearish at US$13.00 per share. Even so, with a relatively close grouping of estimates, it looks like the analysts are quite confident in their valuations, suggesting Gambling.com Group is an easy business to forecast or the underlying assumptions are obvious.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. It's clear from the latest estimates that Gambling.com Group's rate of growth is expected to accelerate meaningfully, with the forecast 52% annualised revenue growth to the end of 2022 noticeably faster than its historical growth of 32% p.a. over the past three years. Compare this with other companies in the same industry, which are forecast to grow their revenue 4.1% annually. Factoring in the forecast acceleration in revenue, it's pretty clear that Gambling.com Group is expected to grow much faster than its industry.

The Bottom Line

The most important thing to take away is that there's been no major change in sentiment, with analysts reconfirming that earnings per share are expected to continue performing in line with their prior expectations. They also upgraded their revenue estimates for next year, and sales are expected to grow faster than the wider market. There was also an increase in the price target, suggesting that there is more optimism baked into the forecasts than there was previously. Given that analysts appear to be expecting substantial improvement in the sales pipeline, now could be the right time to take another look at Gambling.com Group.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At Simply Wall St, we have a full range of analyst estimates for Gambling.com Group going out to 2023, and you can see them free on our platform here..

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.