Do LCNB's (NASDAQ:LCNB) Earnings Warrant Your Attention?

It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. Sometimes these stories can cloud the minds of investors, leading them to invest with their emotions rather than on the merit of good company fundamentals. Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

In contrast to all that, many investors prefer to focus on companies like LCNB (NASDAQ:LCNB), which has not only revenues, but also profits. While this doesn't necessarily speak to whether it's undervalued, the profitability of the business is enough to warrant some appreciation - especially if its growing.

Check out our latest analysis for LCNB

LCNB's Earnings Per Share Are Growing

If a company can keep growing earnings per share (EPS) long enough, its share price should eventually follow. So it makes sense that experienced investors pay close attention to company EPS when undertaking investment research. LCNB managed to grow EPS by 9.2% per year, over three years. That's a pretty good rate, if the company can sustain it. Getting in to the the finer details, it important to know that the EPS growth has been helped by share buybacks, demonstrating that the business is positioned to return capital to its shareholders.

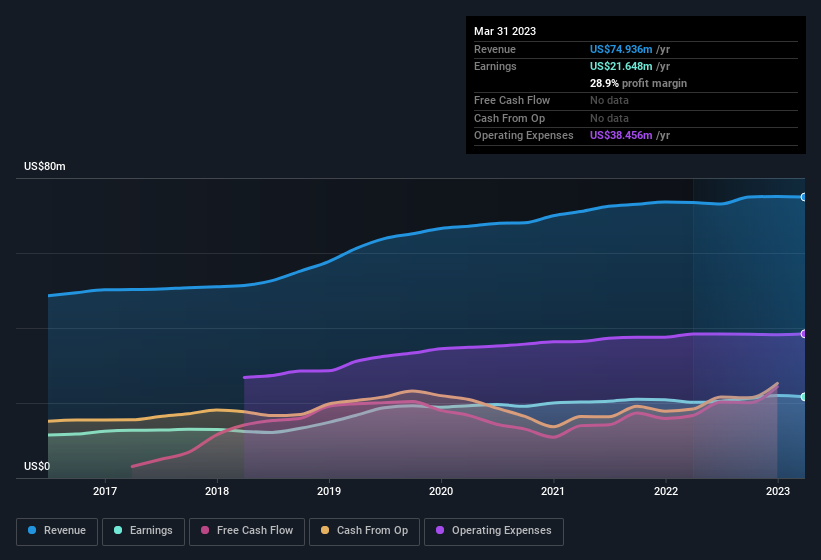

It's often helpful to take a look at earnings before interest and tax (EBIT) margins, as well as revenue growth, to get another take on the quality of the company's growth. It's noted that LCNB's revenue from operations was lower than its revenue in the last twelve months, so that could distort our analysis of its margins. While we note LCNB achieved similar EBIT margins to last year, revenue grew by a solid 2.0% to US$75m. That's a real positive.

The chart below shows how the company's bottom and top lines have progressed over time. Click on the chart to see the exact numbers.

LCNB isn't a huge company, given its market capitalisation of US$180m. That makes it extra important to check on its balance sheet strength.

Are LCNB Insiders Aligned With All Shareholders?

Investors are always searching for a vote of confidence in the companies they hold and insider buying is one of the key indicators for optimism on the market. Because often, the purchase of stock is a sign that the buyer views it as undervalued. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

We note that LCNB insiders spent US$150k on stock, over the last year; in contrast, we didn't see any selling. That paints the company in a nice light, as it signals that its leaders are feeling confident in where the company is heading. Zooming in, we can see that the biggest insider purchase was by Assistant Secretary for the Board & Director William Kaufman for US$49k worth of shares, at about US$16.45 per share.

On top of the insider buying, it's good to see that LCNB insiders have a valuable investment in the business. To be specific, they have US$13m worth of shares. That's a lot of money, and no small incentive to work hard. As a percentage, this totals to 7.0% of the shares on issue for the business, an appreciable amount considering the market cap.

Shareholders have more to smile about than just insiders adding more shares to their already sizeable holdings. That's because LCNB's CEO, Eric Meilstrup, is paid at a relatively modest level when compared to other CEOs for companies of this size. The median total compensation for CEOs of companies similar in size to LCNB, with market caps between US$100m and US$400m, is around US$1.7m.

The CEO of LCNB only received US$589k in total compensation for the year ending December 2022. That looks like a modest pay packet, and may hint at a certain respect for the interests of shareholders. CEO compensation is hardly the most important aspect of a company to consider, but when it's reasonable, that gives a little more confidence that leadership are looking out for shareholder interests. It can also be a sign of a culture of integrity, in a broader sense.

Does LCNB Deserve A Spot On Your Watchlist?

One positive for LCNB is that it is growing EPS. That's nice to see. On top of that, we've seen insiders buying shares even though they already own plenty. That makes the company a prime candidate for your watchlist - and arguably a research priority. Before you take the next step you should know about the 1 warning sign for LCNB that we have uncovered.

The good news is that LCNB is not the only growth stock with insider buying. Here's a list of them... with insider buying in the last three months!

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here