What We Learned About L3Harris Technologies' (NYSE:LHX) CEO Compensation

Bill Brown became the CEO of L3Harris Technologies, Inc. (NYSE:LHX) in 2011, and we think it's a good time to look at the executive's compensation against the backdrop of overall company performance. This analysis will also assess whether L3Harris Technologies pays its CEO appropriately, considering recent earnings growth and total shareholder returns.

View our latest analysis for L3Harris Technologies

Comparing L3Harris Technologies, Inc.'s CEO Compensation With the industry

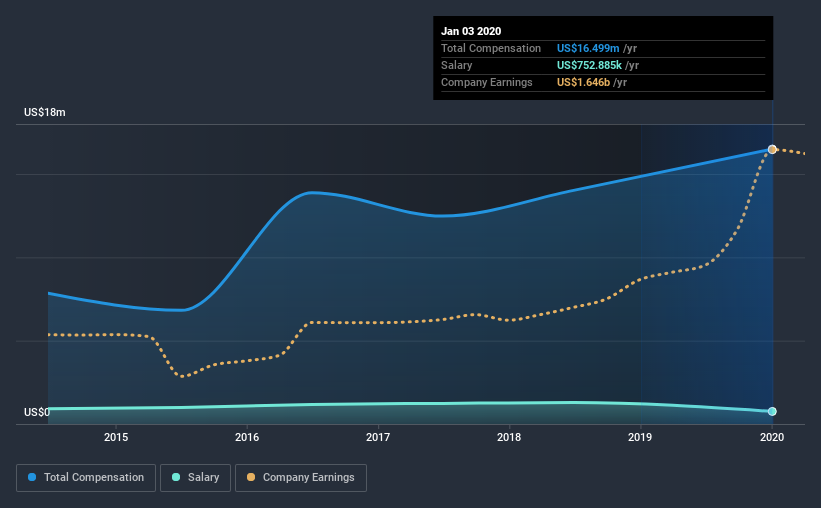

Our data indicates that L3Harris Technologies, Inc. has a market capitalization of US$37b, and total annual CEO compensation was reported as US$16m for the year to January 2020. That's a notable increase of 18% on last year. We think total compensation is more important but our data shows that the CEO salary is lower, at US$753k.

For comparison, other companies in the industry with market capitalizations above US$8.0b, reported a median total CEO compensation of US$16m. This suggests that L3Harris Technologies remunerates its CEO largely in line with the industry average. Furthermore, Bill Brown directly owns US$63m worth of shares in the company, implying that they are deeply invested in the company's success.

Component | 2020 | 2018 | Proportion (2020) |

Salary | US$753k | US$1.3m | 5% |

Other | US$16m | US$13m | 95% |

Total Compensation | US$16m | US$14m | 100% |

Speaking on an industry level, nearly 21% of total compensation represents salary, while the remainder of 79% is other remuneration. Interestingly, the company has chosen to go down an unconventional route in that it pays a smaller salary to Bill Brown as compared to non-salary compensation over the one-year period examined. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

L3Harris Technologies, Inc.'s Growth

Over the past three years, L3Harris Technologies, Inc. has seen its earnings per share (EPS) grow by 9.9% per year. It achieved revenue growth of 223% over the last year.

It's great to see that revenue growth is strong. Combined with modest EPS growth, we get a good impression of the company. We'd stop short of saying the business performance is amazing, but there are enough positives to justify further research, or even adding the stock to your watch-list. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has L3Harris Technologies, Inc. Been A Good Investment?

Most shareholders would probably be pleased with L3Harris Technologies, Inc. for providing a total return of 55% over three years. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

To Conclude...

L3Harris Technologies prefers rewarding its CEO through non-salary benefits. As previously discussed, Bill is compensated close to the median for companies of its size, and which belong to the same industry. However, the company's earnings growth numbers over the last three years is not that impressive. On the other hand, shareholder returns over the same period have been very healthy. So while shareholders shouldn't be overly concerned about CEO compensation, we suspect most would prefer to see improved performance, before a bump in pay.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. That's why we did some digging and identified 3 warning signs for L3Harris Technologies that investors should think about before committing capital to this stock.

Switching gears from L3Harris Technologies, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.