McCormick (MKC) Up More Than 15% in 3 Months: Here's Why

McCormick & Company MKC is benefiting from solid growth endeavors, including lucrative acquisitions and effective cost-saving plans. The company is on track to capitalize on the sustained shift to cooking more at home, higher digital engagement, clean and flavorful eating as well as trusted brands. Also, a robust recovery in the away-from-home demand has been aiding.

Courtesy of such upsides, McCormick’s fourth-quarter fiscal 2021 top and the bottom line increased year over year and surpassed the Zacks Consensus Estimate. Management expects to achieve sales growth of 3-5% (up 4-6% at constant currency) year over year in fiscal 2022. Management anticipates sales to be led by new products, brand marketing, category management and differentiated customer engagement. McCormick’s pricing actions and cost savings are likely to offset projected inflationary pressures. Adjusted earnings per share (EPS) are expected in the range of $3.17-$3.22 during this time.

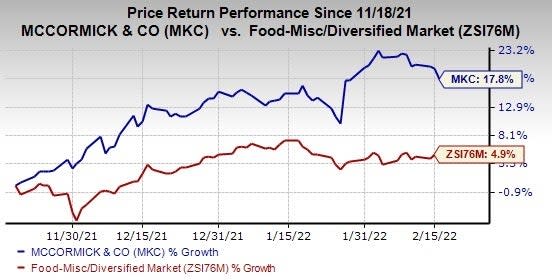

McCormick’s shares have increased 17.8% in the past three months compared with the industry’s growth of 4.9%. Let’s delve deeper

Image Source: Zacks Investment Research

Other Factors Driving Growth

McCormick strategically increased its presence through acquisitions to grow its portfolio. In December 2020, McCormick bought a 100% stake in FONA International, LLC and some of its affiliates. FONA’s diverse portfolio helps McCormick bolster its value-add offerings and expand the flavor solutions segment into attractive categories. In November 2020, McCormick also completed the acquisition of the parent company of Cholula Hot Sauce — a premium Mexico-based hot sauce brand. The buyout of Cholula accelerates McCormick growth potential across the condiment platform and widens the product portfolio in the hot sauce category.

Apart from these factors, the company is on track to make investments to expand its infrastructure worldwide. In this regard, McCormick is investing in its supply chain to enhance capacity and capabilities. Management earlier highlighted that it is on track to increase the condiment and seasoning capacity. The company is on track to optimize its distribution network for the new Northeast U.S. distribution center. MKC had earlier stated that it is about to complete its U.K. Flavor Solutions manufacturing facility.

Will Hurdles be Countered?

McCormick has been grappling with cost inflation for a while now. During fourth-quarter fiscal 2021, the company’s gross profit margin contracted 180 basis points (bps) to 40.6%, thanks to increased cost inflation. In its last earnings call, management highlighted that it continues to face cost pressures from higher inflation along with broad-based supply chain-related hurdles. The company expects the 2022 adjusted gross margin to range between comparable to 2021 to 50 bps lower year over year. The view reflects the projected impact of mid-teens increase in cost inflation and the unfavorable impact of sales mix between segments.

That said, the Zacks Rank #3 (Hold) company is on track to counter the inflationary pressure through various pricing and cost-saving actions. McCormick focuses on saving costs and enhancing productivity through its ongoing Comprehensive Continuous Improvement (CCI) program. McCormick’s CCI program helped the company to reduce costs and enhance productivity. The company expects to achieve CCI-led cost savings of nearly $85 million in 2022.

Looking for Solid Consumer Staple Stocks? Check These

Some better-ranked stocks are Tyson Foods, Inc. TSN, Flowers Foods FLO and Medifast, Inc. MED

Tyson Foods, a meat provider, currently sports a Zacks Rank #1 (Strong Buy). Shares of Tyson Foods have increased 14.4% in the past three months. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Tyson Foods’ current financial year sales suggests growth of 9.5% from the year-ago reported number. TSN has a trailing four-quarter earnings surprise of 32.2%, on average.

Medifast, the manufacturer and distributor of weight loss, weight management, healthy living products and other consumable health and nutritional products, currently carries a Zacks Rank #2 (Buy). Shares of Medifast have declined 12.4% in the past three months.

The Zacks Consensus Estimate for Medifast’s current financial year sales and EPS suggests growth of about 63% and 49.3%, respectively, from the year-ago reported figure. MED has a trailing four-quarter earnings surprise of 17.3%, on average.

Flowers Foods, which produces and markets packaged bakery products, carries a Zacks Rank #2. Shares of Flowers Foods have moved up 4.6% in the past three months.

The Zacks Consensus Estimate for Flowers Foods' 2022 financial year EPS suggests growth of 3.2% from the year-ago reported number. FLO has a trailing four-quarter earnings surprise of 9%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Tyson Foods, Inc. (TSN) : Free Stock Analysis Report

McCormick & Company, Incorporated (MKC) : Free Stock Analysis Report

Flowers Foods, Inc. (FLO) : Free Stock Analysis Report

MEDIFAST INC (MED) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research