It Might Not Be A Great Idea To Buy Reitmans (Canada) Limited (TSE:RET.A) For Its Next Dividend

Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see Reitmans (Canada) Limited (TSE:RET.A) is about to trade ex-dividend in the next 3 days. Investors can purchase shares before the 9th of October in order to be eligible for this dividend, which will be paid on the 24th of October.

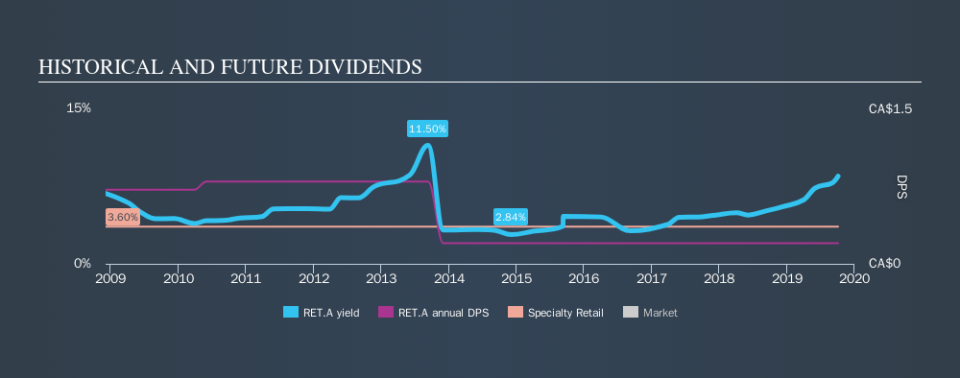

Reitmans (Canada)'s upcoming dividend is CA$0.05 a share, following on from the last 12 months, when the company distributed a total of CA$0.2 per share to shareholders. Based on the last year's worth of payments, Reitmans (Canada) has a trailing yield of 8.5% on the current stock price of CA$2.35. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! That's why we should always check whether the dividend payments appear sustainable, and if the company is growing.

See our latest analysis for Reitmans (Canada)

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Reitmans (Canada) reported a loss after tax last year, which means it's paying a dividend despite being unprofitable. While this might be a one-off event, this is unlikely to be sustainable in the long term. Given that the company reported a loss last year, we now need to see if it generated enough free cash flow to fund the dividend. If Reitmans (Canada) didn't generate enough cash to pay the dividend, then it must have either paid from cash in the bank or by borrowing money, neither of which is sustainable in the long term. It paid out more than half (71%) of its free cash flow in the past year, which is within an average range for most companies.

Click here to see how much of its profit Reitmans (Canada) paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Companies with falling earnings are riskier for dividend shareholders. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. Reitmans (Canada) was unprofitable last year and, unfortunately, the general trend suggests its earnings have been in decline over the last five years, making us wonder if the dividend is sustainable at all.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. Reitmans (Canada) has seen its dividend decline 12% per annum on average over the past ten years, which is not great to see. It's never nice to see earnings and dividends falling, but at least management has cut the dividend rather than potentially risk the company's health in an attempt to maintain it.

We update our analysis on Reitmans (Canada) every 24 hours, so you can always get the latest insights on its financial health, here.

To Sum It Up

From a dividend perspective, should investors buy or avoid Reitmans (Canada)? First, it's not great to see the company paying a dividend despite being loss-making over the last year. On the plus side, the dividend was covered by free cash flow." It's not the most attractive proposition from a dividend perspective, and we'd probably give this one a miss for now.

Want to learn more about Reitmans (Canada)'s dividend performance? Check out this visualisation of its historical revenue and earnings growth.

A common investment mistake is buying the first interesting stock you see. Here you can find a list of promising dividend stocks with a greater than 2% yield and an upcoming dividend.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.