Mirvac Group's (ASX:MGR) On An Uptrend But Financial Prospects Look Pretty Weak: Is The Stock Overpriced?

Mirvac Group's (ASX:MGR) stock is up by a considerable 25% over the past three months. We, however wanted to have a closer look at its key financial indicators as the markets usually pay for long-term fundamentals, and in this case, they don't look very promising. Particularly, we will be paying attention to Mirvac Group's ROE today.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. Put another way, it reveals the company's success at turning shareholder investments into profits.

Check out our latest analysis for Mirvac Group

How Do You Calculate Return On Equity?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Mirvac Group is:

5.5% = AU$563m ÷ AU$10b (Based on the trailing twelve months to June 2020).

The 'return' is the profit over the last twelve months. That means that for every A$1 worth of shareholders' equity, the company generated A$0.06 in profit.

What Is The Relationship Between ROE And Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

Mirvac Group's Earnings Growth And 5.5% ROE

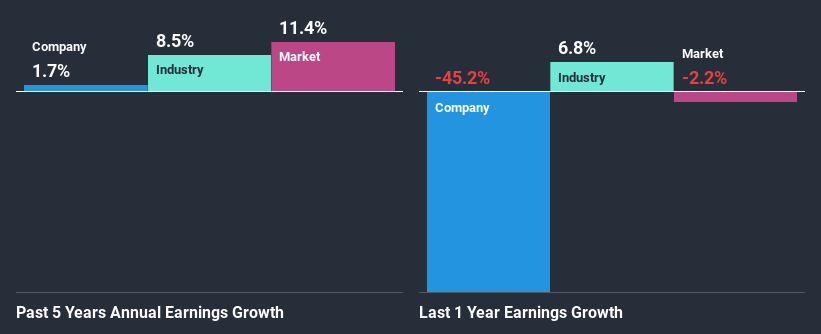

At first glance, Mirvac Group's ROE doesn't look very promising. Yet, a closer study shows that the company's ROE is similar to the industry average of 6.6%. Still, Mirvac Group has seen a flat net income growth over the past five years. Bear in mind, the company's ROE is not very high. Hence, this provides some context to the flat earnings growth seen by the company.

As a next step, we compared Mirvac Group's net income growth with the industry and were disappointed to see that the company's growth is lower than the industry average growth of 8.5% in the same period.

Earnings growth is an important metric to consider when valuing a stock. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). This then helps them determine if the stock is placed for a bright or bleak future. Is MGR fairly valued? This infographic on the company's intrinsic value has everything you need to know.

Is Mirvac Group Making Efficient Use Of Its Profits?

Mirvac Group has a very high three-year median payout ratio of 66% (or a retention ratio of 34%). However, it's not unusual to see a REIT with such a high payout ratio mainly due to statutory requirements. So this probably explains the absence of growth in earnings.

Additionally, Mirvac Group has paid dividends over a period of at least ten years, which means that the company's management is determined to pay dividends even if it means little to no earnings growth. Based on the latest analysts' estimates, we found that the company's future payout ratio over the next three years is expected to hold steady at 70%. Therefore, the company's future ROE is also not expected to change by much with analysts predicting an ROE of 5.8%.

Summary

Overall, we would be extremely cautious before making any decision on Mirvac Group. Because the company is not reinvesting much into the business, and given the low ROE, it's not surprising to see the lack or absence of growth in its earnings. That being so, the latest analyst forecasts show that the company will continue to see an expansion in its earnings. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.