Netflix’s Debt Makes It Tough to Be Bullish on Netflix Stock

By and large, investors shrugged off the fact that Netflix (NASDAQ:NFLX) will be taking on another $2 billion of debt. Indeed, with Netflix stock jumping another 1.2% on Tuesday following Monday’s 4.7% post-earnings gain, the market almost seems to be celebrating the streaming giant’s indebtedness.

Source: Shutterstock

Sooner or later though, debts have to stop growing and start being paid off. A company can’t burn cash in perpetuity.

Fans of Netflix stock are generally quick to argue that that day is coming, sooner or later. With “just a little more subscriber growth,” they say, NFLX will be self-sustaining and will be able to fund its content-creation operations without borrowing.

InvestorPlace - Stock Market News, Stock Advice & Trading Tips

Pulling off that feat, however, has become significantly more difficult now than it would have been just a few months ago.

Debt Continues to Pile Up

For more than a year. NFLX has been spending more and more on video content — both home-grown and from third parties — as a means of growing its subscriber base.

The approach appears to be working too. Netflix has reportedly budgeted $15 billion for content this year, up from 2018’s $12 billion, and last quarter’s total subscriber count of 148.86 million set another record. Both numbers have been growing in tandem for years.

Netflix has yet to achieve true profitability though.

Some investors will argue that point. For the first quarter of 2019, Netflix reported an operating profit of 76 cents per share of Netflix stock, up from the 64 cents per share of NFLX stock the company reported in the same quarter a year earlier.

Cash flow remains uncomfortably negative, though. Last quarter’s operational cash flow was a negative $379.8 million, growing from the negative cash flow of $236.8 million reported for the first quarter of 2018.

Non-GAAP free cash flow grew from a negative $286.5 million in the first quarter of 2018 to a negative $459.9 million in Q1 of this year.

In fact, Netflix hasn’t reported positive cash flow since the second quarter of 2014. Rising content costs are part of the reason for that.

Also contributing to the red ink are the rising interest payments on the junk-rated debt that Netflix continues to issue to fund that content creation and curation. So are increasing marketing costs, which are even more necessary, given new competition from the likes of Walt Disney (NYSE:DIS) and now Apple (NASDAQ:AAPL).

The question not enough people are asking is: What’s the endgame? When and where might Netflix stop adding debt at a faster clip than it’s adding revenue and subscribers?

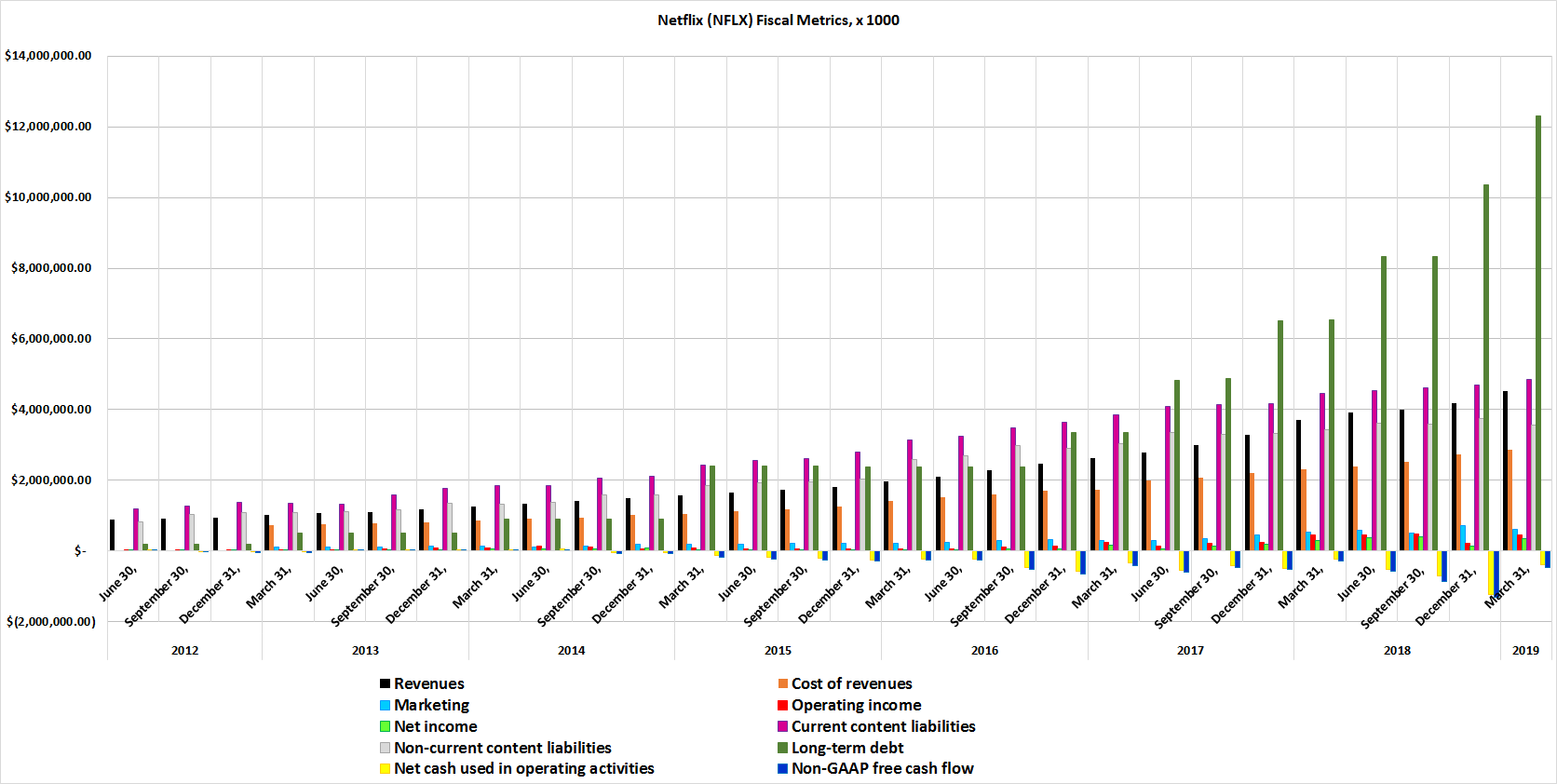

The graphic below puts things in perspective, visually. All the numbers, with the exception of long-term debt, are based on the company’s Q1 report which it released on Apr. 16. The bar that reflects long-term debt has been adjusted to reflect the $2 billion in additional debt NFLX recently announced that it plans to take on.

Few serious investors would dispute that companies have to spend money to make money. The question for NFLX now is simply, at what point do any of these numbers start to make their long-awaited pivot?

The Outlook of Netflix Stock

A handful of professional and amateur analysts will attribute Netflix’s new content-related debt to Disney’s and Apple’s foray into the streaming-video waters. And that argument probably has some credibility.

But the main concern facing Netflix stock at this point is — as it has been for several quarters — what’s the endgame for NFLX? Is there one? Will Netflix ever reach a point where it can grow its subscriber base without adding tons of new content?

In the meantime, a new wrinkle has developed. Even if Netflix does somehow find a cash-generating balance between subscriber counts and content spending, will anyone else in the space allow that to continue for very long?

Disney is clearly deep in the game with a majority stake in Hulu as well as with an impending launch of Disney+. The aforementioned Apple is also stepping up its presence, even if its seevice will mostly feature content from third-party providers.

AT&T (NYSE:T) is finally going to do something on its own, utilizing Time Warner. In the meantime, Amazon Prime may not be crushing its competitors, but it’s making waves, and funneling people toward Amazon.com (NASDAQ:AMZN.) All of these competitors are going to force Netflix to spend more, in exchange for less revenue.

The profit opportunity on this latest $2 billion in debt seems much weaker than the ROI prospects of its first $2 billion of debt. The strength of the arguments of those who are bullish on Netflix stock continues to fade.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can learn more about James at his site, jamesbrumley.com, or follow him on Twitter, at @jbrumley.

More From InvestorPlace

The post Netflix’s Debt Makes It Tough to Be Bullish on Netflix Stock appeared first on InvestorPlace.