Nike's Gross Margin Is an Issue, but Shares Look Undervalued

Nike Inc. (NYSE:NKE) reported quarterly results last week that were not well received by the market. Shares declining almost 13% in the trading session following the release. In total, Nike is down more than 48% for the year.

Nike has some issues in its business, but the stock is trading well below its GF Value. Lets look closer at the company and its most recent quarter to see why I believe Nike offers good value at this price.

Quarterly highlights

Nike reported first-quarter earnings results for its fiscal year 2023 on Sept. 29. Revenue grew 3.6% to $12.7 billion, beating Wall Street analysts estimates by $404 million. Excluding the impact of currency exchange, Nikes sales were higher by 10%. Net income of $1.5 billion, or 93 cents per share, compared unfavorably to $1.9 billion, or $1.16 per share, in the year-ago period. Earnings per share were 10 cents better than expected.

Nike Direct sales grew 8% to $5.1 billion. This channel was up 14% on a currency-neutral basis. Nike Brand Digital revenue was higher by 16%% on a reported basis and 23% excluding currency.

By region, North America grew 13%, Asia Pacific and Latin America improved 5% (up 16% in constant currency) and Europe, Middle East and Africa was up 1% (up 17% in constant currency). Greater China fell 16%. The Converse brnad was up 2%.

Merchandise markdowns and higher expenses for fright and logistics caused a 220 basis point decline in the gross margin to 44.3%. Inventory levels were up 44% to $9.7 billion.

Takeaways

Several weeks ago, I opined that the market was offering a good entry point into Nike Inc. (NYSE:NKE). That view was based on the companys previous quarter, where merchandise levels were higher, but the company wasnt discounting products in order to move them as demand remained elevated. As a result, the gross margin expanded 120 basis points last fiscal year. The most recent quarter has showed some cracks in my previous thesis.

First, the gross margin has contracted much faster than it did in the prior quarter as the company began to discount products at a much heavier rate in order to clear inventory that had built up. Much of the increase in inventory took place in North America, where supply chain constraints led to Nike carrying an increase in out-of-season products.

Inventories remain high, though, even after the discounting activity, which means that markdowns will likely continue into the current quarter. Gross margins will thus be under pressure once again.

Another headwind is Nikes performance in Greater China, which has been a real source of strength for the company historically. Sales for the region fell mid-double-digits, which comes on the heels of a 19% decline in the fourth quarter and a 5% decrease in the third quarter of fiscal year 2022. The weakness in those quarters were largely attributed to Covid-19 restrictions, but those had mostly eased by the end of fiscal year 2022. Clearly, Nike is having difficulty in its most important growth region beyond just lockdowns.

The third item that is impacting Nike is the strengthening of the U.S. dollar, which has railed more than 16% year-to-date. Much of this increase is due to aggressive Federal Reserve quantitative easing and quantitative tighening policies. With more interest rate hikes likely in the near-term, the dollar could rally further. More than 50% of Nike's revenue comes from international markets, so the company is likely to see continued pressure from currency exchange rates.

Not all is lost, however. Management stated on the conference call that the company saw double-digit sales growth in the month of September as back-to-school shopping was robust. Some of the supply chain disruptions have been smoothed out, so markdowns may not persist much past the next quarter or two. A strong dollar hurts results, but the good news here is that demand remains very high in international markets outside of China, as currency neutral sales were all in the mid to high double-digit range. And in China, the decline in year-over-year sales has at least decelerated quarter-over-quarter.

Valuation

The reduction in the share price has also brought the stock to a more reasonable valuation. Shares of Nike closed at $84 apiece on Oct. 3. Analysts project earnings per share of $3.02 this fiscal year, implying a forward price-earnings ratio of 27.8. Removing the artificially elevated multiple of 2020 due to Covid-19, the average price-earnings ratio has been just under 30 since 2012, according to Value Line. Thus, the stock is priced at a discount to its historical valuation.

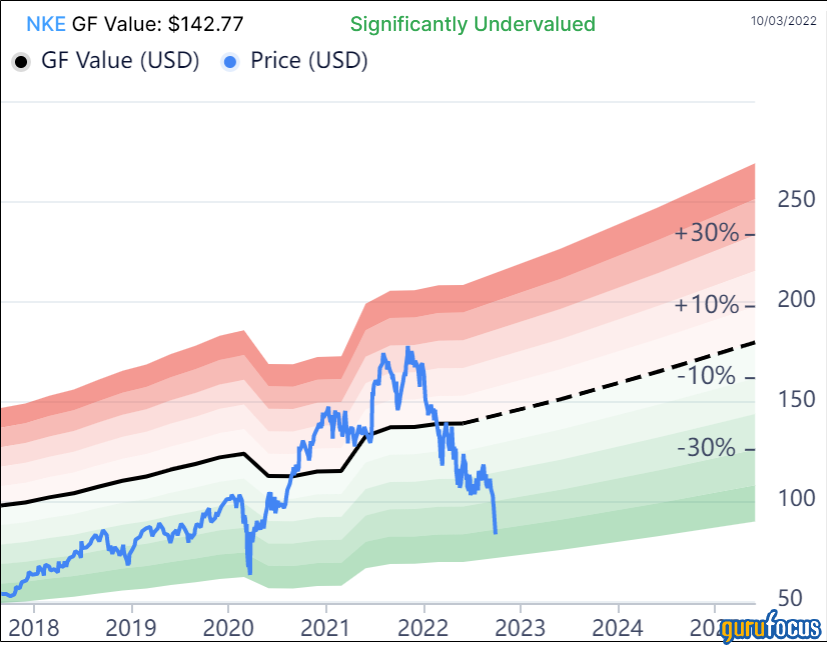

The GF Value chart rates the stock as significantly undervalued. Nike is trading at a 70% discount to its GF Value.

Final thoughts

Nikes stock was punished following the release of its fiscal first-quarter earnings, and maybe it needed the correction. The company had to mark down products in North America in order to begin right-sizing its inventory levels. Nike also continues to struggle in its most important growth region, and currency remains a headwind as well.

The plus side is that Nikes stock is now more reasonably valued on a historical basis, and the discount to its GF Value is even steeper than it was last month. It might take the company several more quarters to get its inventory to lower levels, but Nike remains one of the worlds most well-known and valuable brands. For investors looking at the long-term, I believe Nike could be an excellent value proposition.

This article first appeared on GuruFocus.