A New Question Now Hovers Over MPLX's Earnings

It was looking like, for the first time in a while, we were going to be able to look at MPLX's (NYSE: MPLX) most recent earnings report without having to consider some big transaction down the road that would fundamentally change these numbers and render them useless. Then, just a couple days before earnings were released, MPLX's parent company, Marathon Petroleum (NYSE: MPC), announced a huge acquisition that could have a profound impact on MPLX down the road.

Let's take a look at MPLX's most recent earnings numbers and sift through the recent deal to see what it could mean for shareholders.

Image source: Getty Images.

By the numbers

Metric | Q1 2018 | Q4 2017 | Q1 2017 |

|---|---|---|---|

Revenue | $1.42 billion | $1.08 billion | $886 million |

Adjusted EBITDA | $762 million | $569 million | $471 million |

EPS | $0.61 | $0.31 | $0.19 |

Distributable cash flow | $619 million | $445 million | $354 million |

SOURCE: MPLX EARNINGS RELEASE. EPS= EARNINGS PER SHARE.

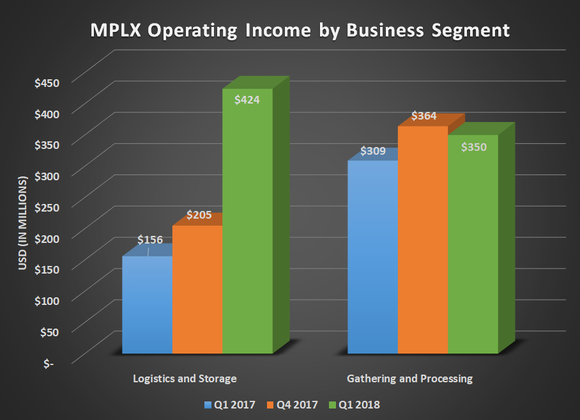

It's pretty much impossible to compare MPLX's earnings results on a quarterly basis because so much changed over the past 12 months. Ever since the beginning of 2017, Marathon Petroleum has been dropping down assets at an accelerated rate to get all of is MLP qualifying assets off its books and into the hands of MPLX. On Feb. 1, Marathon completed the last of those transactions with a deal to acquire a suite of Logistics and Storage assets that generate approximately $1 billion in annual EBITDA. So what is even more surprising about these earnings results is that they only partially reflect the impact on MPLX's bottom line. We should see results for its logistics and storage segment gain even more in the second quarter.

Data source: MPLX earnings release. Chart by author.

Even after this flurry of activity, MPLX's financials still remained rather strong. It ended the quarter with a distribution coverage ratio of 1.29 times, which is more than enough to cover its current payment and leave plenty of wiggle room for future payout hikes. Because of the timing of this recent transaction, its debt metrics took a bit of a hit, but on a pro forma basis, net debt to adjusted EBITDA was a healthy 3.8 times.

What management had to say

After such a monumental amount of changes to MPLX's business segments and corporate structure over the past year, I'm guessing that investors were expecting a period of calm. That wasn't the case as Marathon recently announced that it was acquiring fellow refiner Andeavor (NYSE: ANDV) in a $23 billion deal. Like Marathon, Andeavor has its own subsidiary MLP in Andeavor Logistics (NYSE: ANDX), which of course Marathon will take control of in the transaction. This, of course, raises the immediate question about the fate of these two subsidiaries. On the company's conference call, CEO Gary Heminger addressed the question as much as he could considering that the deal is still pending.

You are likely aware that earlier this morning MPC announces plans to acquire all the outstanding shares of Andeavor to create a leading energy company in the U.S. We're enthusiastic about MPLX's role in this new leading energy company that is well positioned for long-term growth and value creation for all the stakeholders and we believe this combination and expansion of MPC's footprint will provide additional strategic and organic growth opportunities for MPLX.

Also, at the closing of the transaction, MPC will own the general partner of MPLX and Andeavor Logistics as well as the majority of the limited partner units of both partnerships. We know that a very logical question is, what will the general partner do with the two MLPs post-closing? We're not commenting on any potential structural considerations for MPLX and Andeavor Logistics today, both will operate as separate MLPs and MPC will evaluate structural considerations at the appropriate time following the close of the Andeavor transaction.

Reading between the lines here, I think it's pretty clear that Marathon will do some move in the future to combine the two. It probably won't happen immediately, but it probably will.

Waiting until we know what will happen

Full disclosure, I'm an MPLX shareholder and have a vested interest in what Marathon decides to do with MPLX and Andeavor Logistics once the deal to merge the two refiners is complete. If you look at the logistics footprints of MPLX and Andeavor, there isn't a whole lot of geographic overlap. It could give the combined entity a plethora of investment opportunities across the country, but it also means there aren't a whole lot of opportunities to enhance their respective networks into a more compelling value proposition for its customers.

Ultimately, it will be in MPLX's and Andeavor Logistics' best interests if they were to be a combined entity rather than acting as two separate subsidiaries of the same parent providing duplicative services. Situations like that make it unnecessarily complicated when allocating capital. The question for investors will be how much MPLX has to pay to add Andeavor Logistics to the mix and who much it will impact its financials. Its debt levels are already creeping up from this recent deal, and part of the value proposition for MPLX has been its squeaky-clean balance sheet. We may have to wait a while for the answer to these questions, so investors may want to sit tight.

More From The Motley Fool

Tyler Crowe owns shares of MPLX LP. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.