Is PageGroup plc’s (LON:PAGE) Liquidity As Good As Its Solvency?

Mid-caps stocks, like PageGroup plc (LSE:PAGE) with a market capitalization of £1.70B, aren’t the focus of most investors who prefer to direct their investments towards either large-cap or small-cap stocks. Surprisingly though, when accounted for risk, mid-caps have delivered better returns compared to the two other categories of stocks. PAGE’s financial liquidity and debt position will be analysed in this article, to get an idea of whether the company can fund opportunities for strategic growth and maintain strength through economic downturns. Note that this commentary is very high-level and solely focused on financial health, so I suggest you dig deeper yourself into PAGE here. View our latest analysis for PageGroup

Can PAGE service its debt comfortably?

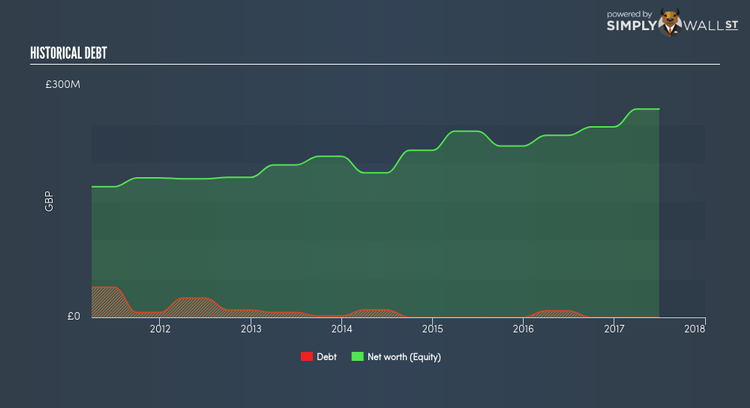

What is considered a high debt-to-equity ratio differs depending on the industry, because some industries tend to utilize more debt financing than others. A ratio below 40% for mid-cap stocks is considered as financially healthy, as a rule of thumb. The good news for investors is that PageGroup has no debt. It has been operating its business with zero debt and utilising only its equity capital. Investors’ risk associated with debt is virtually non-existent with PAGE, and the company has plenty of headroom and ability to raise debt should it need to in the future.

Does PAGE’s liquid assets cover its short-term commitments?

Given zero long-term debt on its balance sheet, PageGroup has no solvency issues, which is used to describe the company’s ability to meet its long-term obligations. But another important aspect of financial health is liquidity: the company’s ability to meet short-term obligations, including payments to suppliers and employees. Looking at PAGE’s most recent £199.5M liabilities, it seems that the business has maintained a safe level of current assets to meet its obligations, with the current ratio last standing at 1.83x. Generally, for Professional Services companies, this is a reasonable ratio as there’s enough of a cash buffer without holding too capital in low return investments.

Next Steps:

PAGE has zero-debt in addition to ample cash to cover its near-term commitments. Its safe operations reduces risk for the company and its investors, however, some level of debt may also ramp up earnings growth and operational efficiency. I admit this is a fairly basic analysis for PAGE’s financial health. Other important fundamentals need to be considered alongside. I recommend you continue to research PageGroup to get a more holistic view of the stock by looking at:

1. Future Outlook: What are well-informed industry analysts predicting for PAGE’s future growth? Take a look at our free research report of analyst consensus for PAGE’s outlook.

2. Valuation: What is PAGE worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether PAGE is currently mispriced by the market.

3. Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.