Pennon Group (LON:PNN) Takes On Some Risk With Its Use Of Debt

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Pennon Group Plc (LON:PNN) makes use of debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Pennon Group

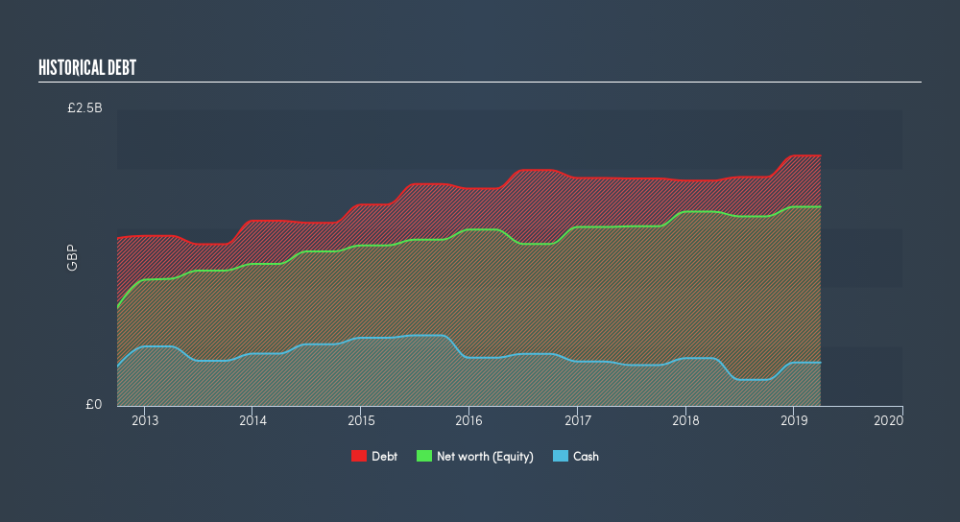

What Is Pennon Group's Debt?

You can click the graphic below for the historical numbers, but it shows that Pennon Group had UK£2.11b of debt in March 2019, down from UK£3.40b, one year before. On the flip side, it has UK£365.7m in cash leading to net debt of about UK£1.74b.

How Healthy Is Pennon Group's Balance Sheet?

We can see from the most recent balance sheet that Pennon Group had liabilities of UK£511.1m falling due within a year, and liabilities of UK£4.27b due beyond that. Offsetting these obligations, it had cash of UK£365.7m as well as receivables valued at UK£318.1m due within 12 months. So its liabilities total UK£4.10b more than the combination of its cash and short-term receivables.

Given this deficit is actually higher than the company's market capitalization of UK£2.93b, we think shareholders really should watch Pennon Group's debt levels, like a parent watching their child ride a bike for the first time. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Pennon Group has a debt to EBITDA ratio of 3.2 and its EBIT covered its interest expense 5.0 times. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. We saw Pennon Group grow its EBIT by 6.1% in the last twelve months. That's far from incredible but it is a good thing, when it comes to paying off debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Pennon Group can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of that EBIT is backed by free cash flow. Considering the last three years, Pennon Group actually recorded a cash outflow, overall. Debt is usually more expensive, and almost always more risky in the hands of a company with negative free cash flow. Shareholders ought to hope for and improvement.

Our View

On the face of it, Pennon Group's level of total liabilities left us tentative about the stock, and its conversion of EBIT to free cash flow was no more enticing than the one empty restaurant on the busiest night of the year. But at least it's pretty decent at growing its EBIT; that's encouraging. We should also note that Water Utilities industry companies like Pennon Group commonly do use debt without problems. Overall, it seems to us that Pennon Group's balance sheet is really quite a risk to the business. For this reason we're pretty cautious about the stock, and we think shareholders should keep a close eye on its liquidity. Another positive for shareholders is that it pays dividends. So if you like receiving those dividend payments, check Pennon Group's dividend history, without delay!

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.