People have stopped paying their mobile-home loans, and it's a warning sign for the economy

Flickr/Dave Young

Delinquencies on mobile-home loans have increased by 2 percentage points over the past year, according to research cited by UBS.

The rising delinquency rate, combined with signs of stress in other areas of the consumer-finance market, suggests there's a two-speed economy.

The mobile-home market is showing signs of stress.

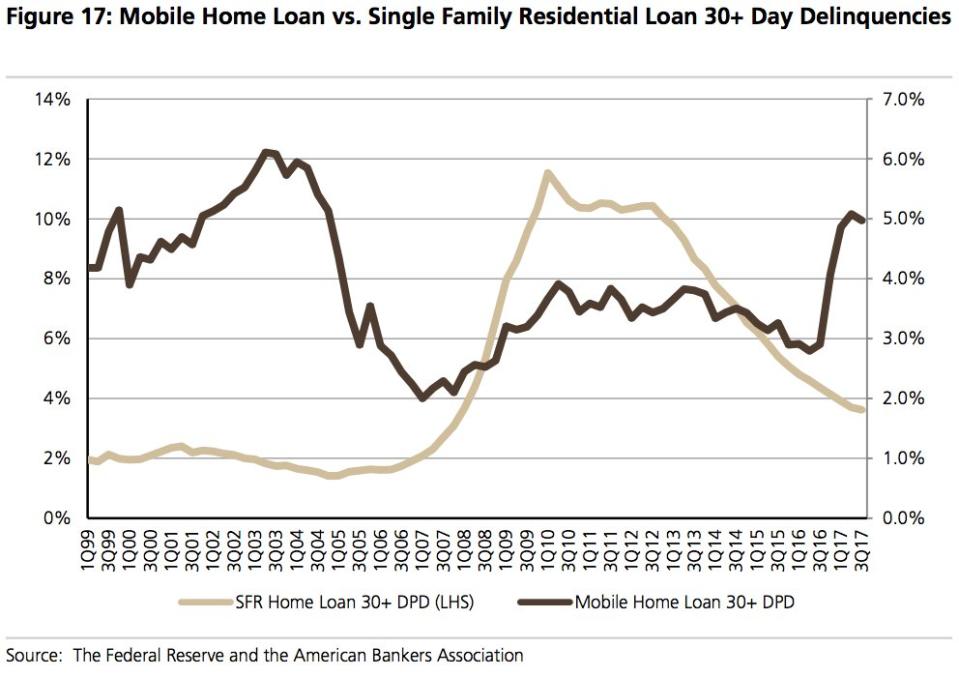

The delinquency rate on mobile-home loans has increased by 200 basis points, or 2 percentage points, over the past year, according to research cited by UBS. The 30-day-plus delinquency level is now about 5%, the highest level since 2005.

The increase in the number of struggling mobile-home borrowers suggests that a large chunk of these people haven't benefitted from the economic growth of the past few years, despite the low unemployment level.

"We interpret this data to mean that these individuals have not largely benefitted from these macro-dynamics, and may also be disproportionately exposed to industries that have experienced compression — rather than expansion — in the current economic conditions, such as retail or some areas of energy extraction," UBS said.

Conventional single-family residential loan delinquencies haven't seen a similar uptick, instead continuing their steady downward path through the post-recession recovery.

UBS

This data represents a piece of a jigsaw puzzle of the condition of consumer finances in the US. And the picture that's emerging, according to UBS, is of a two-speed economy, with lower-income consumers and younger borrowers with substantial student debt moving at a slower pace than more affluent and established participants.

For example:

About three in five consumers with an annual income below $40,000 indicate that their earnings barely or do not cover their expenses, a UBS survey found.

Lower-income earners are often renting and carrying non-mortgage debt — such as credit card, auto, and student debt — at levels similar to or higher than the period before the financial crisis.

More than one-third of borrowers in this demographic report misrepresenting their financials in loan applications, a UBS survey found.

"While delinquency rates among student loans remain the highest of any consumer asset class, several other asset classes are beginning to inflect off of recent lows, despite broadly supportive economic conditions," UBS said.

The new tax law is likely to benefit middle-income borrowers, but it could have limited benefits for lower-income borrowers.

"We believe weakness in these two groups will drive higher credit losses at some stage over the next few years — particularly in credit card, installment, and student loans — with macroeconomic inflection from job growth to job loss as a likely catalyst," UBS said.

NOW WATCH: Facebook can still track you even if you delete your account — here's how to stop it

See Also: