Performant Financial (NASDAQ:PFMT) Is Achieving High Returns On Its Capital

To find a multi-bagger stock, what are the underlying trends we should look for in a business? Ideally, a business will show two trends; firstly a growing return on capital employed (ROCE) and secondly, an increasing amount of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. Speaking of which, we noticed some great changes in Performant Financial's (NASDAQ:PFMT) returns on capital, so let's have a look.

What is Return On Capital Employed (ROCE)?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. To calculate this metric for Performant Financial, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

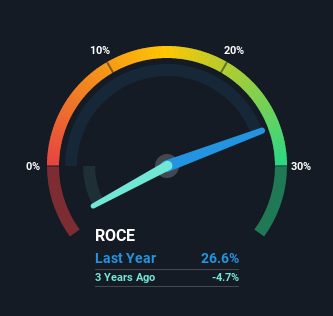

0.27 = US$13m ÷ (US$126m - US$77m) (Based on the trailing twelve months to December 2020).

Thus, Performant Financial has an ROCE of 27%. In absolute terms that's a great return and it's even better than the Commercial Services industry average of 7.5%.

Check out our latest analysis for Performant Financial

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you'd like to look at how Performant Financial has performed in the past in other metrics, you can view this free graph of past earnings, revenue and cash flow.

What The Trend Of ROCE Can Tell Us

You'd find it hard not to be impressed with the ROCE trend at Performant Financial. We found that the returns on capital employed over the last five years have risen by 386%. That's not bad because this tells for every dollar invested (capital employed), the company is increasing the amount earned from that dollar. In regards to capital employed, Performant Financial appears to been achieving more with less, since the business is using 74% less capital to run its operation. If this trend continues, the business might be getting more efficient but it's shrinking in terms of total assets.

For the record though, there was a noticeable increase in the company's current liabilities over the period, so we would attribute some of the ROCE growth to that. Essentially the business now has suppliers or short-term creditors funding about 61% of its operations, which isn't ideal. And with current liabilities at those levels, that's pretty high.

Our Take On Performant Financial's ROCE

From what we've seen above, Performant Financial has managed to increase it's returns on capital all the while reducing it's capital base. Since the stock has only returned 32% to shareholders over the last five years, the promising fundamentals may not be recognized yet by investors. Given that, we'd look further into this stock in case it has more traits that could make it multiply in the long term.

If you want to know some of the risks facing Performant Financial we've found 2 warning signs (1 is a bit unpleasant!) that you should be aware of before investing here.

If you want to search for more stocks that have been earning high returns, check out this free list of stocks with solid balance sheets that are also earning high returns on equity.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.