Pilgrims Pride: A Recession-Proof Defensive Stock

Food inflation in the United States has accelerated for the 12th straight month in a row to 10.1% as of May 2022. This is the first increase of 10% or more since 1981. Larger price hikes of 14.2% were seen for meats, poultry, fish and even eggs. The Federal Reserve has only just started to raise interest rates mildly, and the war in Ukraine has exacerbated food shortages around the world. With all of these factors combined, a deadly combination of runaway inflation and a recession could be possible.

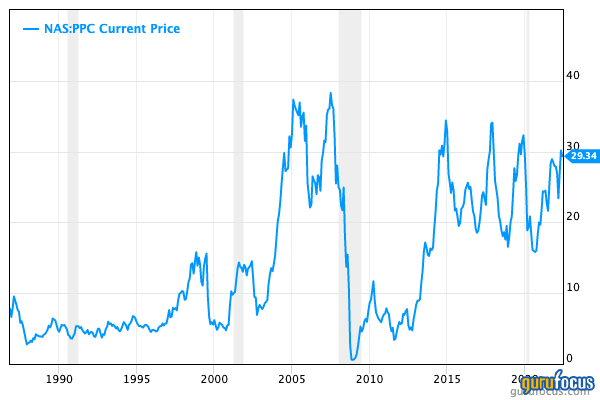

Recession or not, people will always need to eat, and with rising food prices, an investment into a large meat producer could be a wise investment, in my opinion. In particular, I like Pilgrim's Pride (NASDAQ:PPC), which is one of the largest chicken producers in the U.S. This stock recently caught my attention because the world's largest hedge fund, Ray Dalio (Trades, Portfolio)'s Bridgewater Associates, added to their position in the stock in the first quarter of 2022.

Business model

Pilgrim's Pride is one of the largest chicken producers in the U.S. and the second-largest chicken producer in Mexico. They distribute a variety of fresh and frozen chicken, pork and various other meats globally.

They employ over 59,000 people and operate protein processing plants in 14 U.S. states, in addition to Mexico, the U.K. and mainland Europe. They distribute their products through retailers and various foodservice distributors.

The business is pretty straightforward and dependent on macroeconomic conditions.

Financials

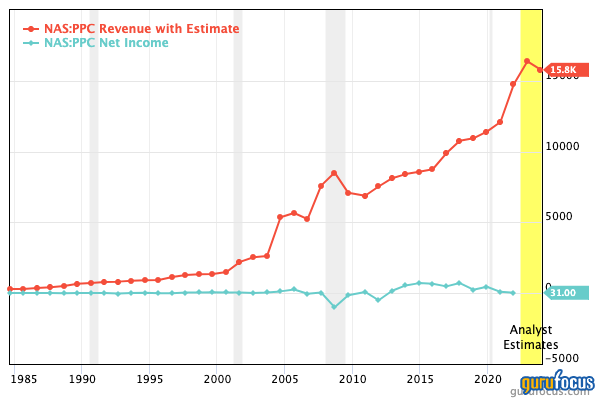

Pilgrim's Pride achieved tremendous growth in the first quarter of 2022. Net sales came in at $4.24 billion, up 30% from the prior year.

Their U.S. foodservice business improved significantly year over year and reached pre-pandemic sales volume. Their brand momentum was also strong in U.S. retail with Just Bare up 49% and Pilgrims fully cooked up by over 150%.

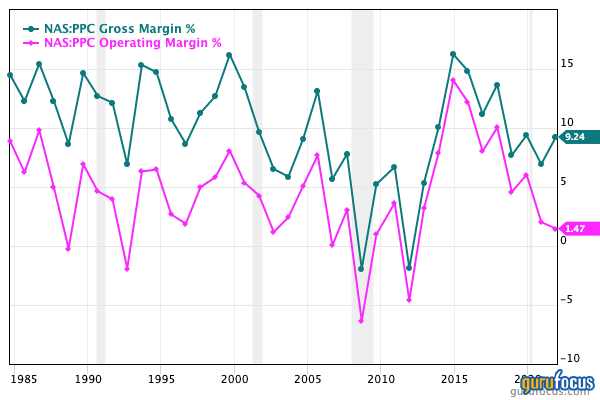

The company generated adjusted Ebitda of $501.8 million for the quarter. This equated to an 11.8% adjusted Ebitda margin, which was 97.7% higher than a year ago. According to the CEO, Matt Galvanoni, gross and operating margins were higher compared to the prior year due to higher commodity prices, strong consumer demand, improved efficiencies and key customer growth.

Valuation

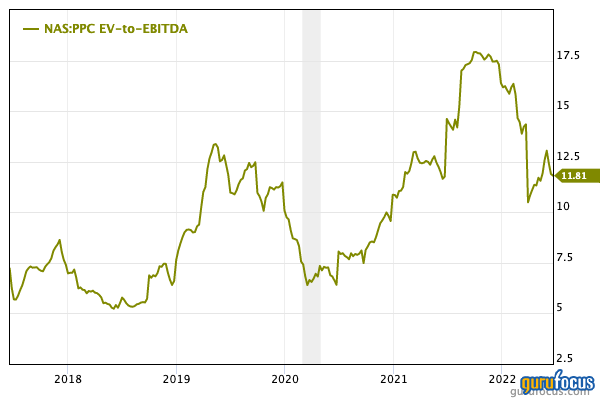

In terms of valuation, Pilgrim's Pride currently trades at an enterprise-value-to-Ebitda ratio of 11.81, which is lower than 2021, but still higher than 2020.

The GF Value chart indicates the stock is fairly valued.

Pilgrim's Pride has achieved tremendous momentum and margin increases recently, which was driven by food price inflation, supply constraints and high demand. Recession or not, people will always need to eat, and thus I believe this fairly valued food stock could help to protect portfolios from inflation.

This article first appeared on GuruFocus.