Is Premaitha Health PLC (AIM:NIPT) A Financially Sound Company?

While small-cap stocks, such as Premaitha Health PLC (AIM:NIPT) with its market cap of GBP £14.05M, are popular for their explosive growth, investors should also be aware of their balance sheet to judge whether the company can survive a downturn. Healthcare Equipment and Supplies companies, in particular ones that run negative earnings, tend to be high risk. Assessing first and foremost the financial health is crucial. Here are few basic financial health checks you should consider before taking the plunge. Though, since I only look at basic financial figures, I suggest you dig deeper yourself into NIPT here.

Does NIPT generate an acceptable amount of cash through operations?

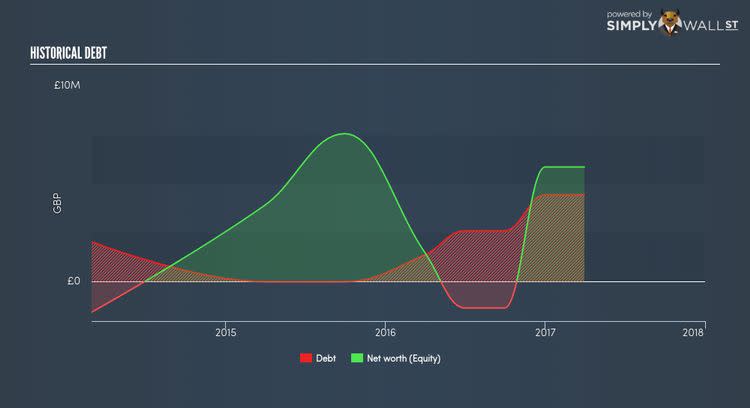

NIPT’s debt levels surged from £1M to £4M over the last 12 months , which is made up of current and long term debt. With this increase in debt, NIPT currently has £1M remaining in cash and short-term investments for investing into the business. Though its operating cash flow is not yet significant enough to calculate a meaningful cash-to-debt ratio, indicating that operational efficiency is something we’d need to take a look at. As the purpose of this article is a high-level overview, I won’t be looking at this today, but you can examine some of NIPT’s operating efficiency ratios such as ROA here.

Does NIPT’s liquid assets cover its short-term commitments?

Looking at NIPT’s most recent £7M liabilities, the company has not been able to meet these commitments with a current assets level of £6M, leading to a 0.88x current account ratio. which is under the appropriate industry ratio of 3x.

Does NIPT face the risk of succumbing to its debt-load?

With a debt-to-equity ratio of 75.79%, NIPT can be considered as an above-average leveraged company. This is not uncommon for a small-cap company given that debt tends to be lower-cost and at times, more accessible. But since NIPT is presently unprofitable, sustainability of its current state of operations becomes a concern. Maintaining a high level of debt, while revenues are still below costs, can be dangerous as liquidity tends to dry up in unexpected downturns.

Next Steps:

Are you a shareholder? At its current level of cash flow coverage, NIPT has room for improvement to better cushion for events which may require debt repayment. In addition to this, the company may not be able to pay all of its upcoming liabilities from its current short-term assets. Given that its financial position may be different. I recommend researching market expectations for NIPT’s future growth on our free analysis platform.

Are you a potential investor? NIPT’s high debt levels along with low cash coverage of debt in addition to low liquidity coverage of near-term commitments may not build the strongest investment case. Though, keep in mind that this is a point-in-time analysis, and today’s performance may not be representative of NIPT’s track record. As a following step, you should take a look at NIPT’s past performance analysis on our free platform in order to determine for yourself whether its debt position is justified.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.