Quaterra Resources (CVE:QTA) Is In A Good Position To Deliver On Growth Plans

There's no doubt that money can be made by owning shares of unprofitable businesses. For example, Quaterra Resources (CVE:QTA) shareholders have done very well over the last year, with the share price soaring by 117%. Nonetheless, only a fool would ignore the risk that a loss making company burns through its cash too quickly.

So notwithstanding the buoyant share price, we think it's well worth asking whether Quaterra Resources' cash burn is too risky. For the purposes of this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow. Let's start with an examination of the business' cash, relative to its cash burn.

View our latest analysis for Quaterra Resources

Does Quaterra Resources Have A Long Cash Runway?

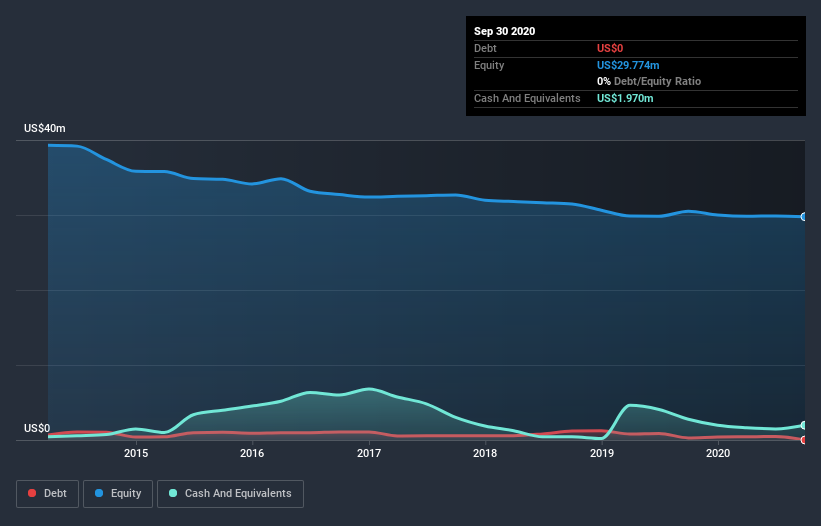

You can calculate a company's cash runway by dividing the amount of cash it has by the rate at which it is spending that cash. In September 2020, Quaterra Resources had US$2.0m in cash, and was debt-free. Importantly, its cash burn was US$903k over the trailing twelve months. Therefore, from September 2020 it had 2.2 years of cash runway. That's decent, giving the company a couple years to develop its business. You can see how its cash balance has changed over time in the image below.

Can Quaterra Resources Raise More Cash Easily?

Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. Commonly, a business will sell new shares in itself to raise cash and drive growth. We can compare a company's cash burn to its market capitalisation to get a sense for how many new shares a company would have to issue to fund one year's operations.

Since it has a market capitalisation of US$22m, Quaterra Resources' US$903k in cash burn equates to about 4.2% of its market value. Given that is a rather small percentage, it would probably be really easy for the company to fund another year's growth by issuing some new shares to investors, or even by taking out a loan.

How Risky Is Quaterra Resources' Cash Burn Situation?

Given it's an early stage company, we don't have a lot of data with which to judge Quaterra Resources' cash burn. We would undoubtedly be more comfortable if it had reported some operating revenue. However, it is fair to say that its cash burn relative to its market cap gave us comfort. In conclusion, we don't see why investors should be concerned with its cash burn, at least for some time. Taking a deeper dive, we've spotted 3 warning signs for Quaterra Resources you should be aware of, and 1 of them makes us a bit uncomfortable.

If you would prefer to check out another company with better fundamentals, then do not miss this free list of interesting companies, that have HIGH return on equity and low debt or this list of stocks which are all forecast to grow.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.