Would Rainbow Rare Earths (LON:RBW) Might Be Better Off With Less Debt

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Rainbow Rare Earths Limited (LON:RBW) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Rainbow Rare Earths

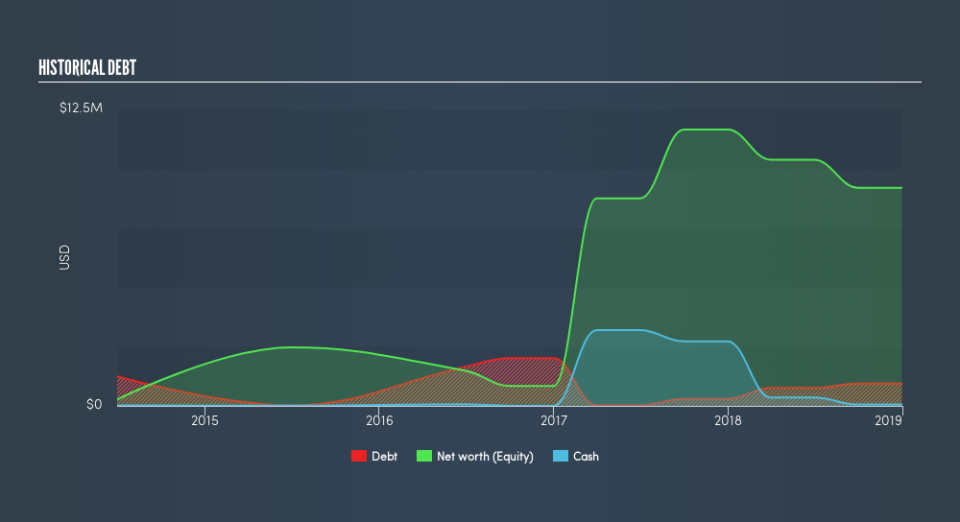

How Much Debt Does Rainbow Rare Earths Carry?

You can click the graphic below for the historical numbers, but it shows that as of December 2018 Rainbow Rare Earths had US$945.0k of debt, an increase on US$298.0k, over one year. However, because it has a cash reserve of US$56.0k, its net debt is less, at about US$889.0k.

How Healthy Is Rainbow Rare Earths's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Rainbow Rare Earths had liabilities of US$2.12m due within 12 months and no liabilities due beyond that. Offsetting this, it had US$56.0k in cash and US$159.0k in receivables that were due within 12 months. So it has liabilities totalling US$1.91m more than its cash and near-term receivables, combined.

Given Rainbow Rare Earths has a market capitalization of US$16.2m, it's hard to believe these liabilities pose much threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Rainbow Rare Earths can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

In the last year Rainbow Rare Earths managed to produce its first revenue as a listed company, but given the lack of profit, shareholders will no doubt be hoping to see some strong increases.

Caveat Emptor

Over the last twelve months Rainbow Rare Earths produced an earnings before interest and tax (EBIT) loss. Indeed, it lost a very considerable US$4.7m at the EBIT level. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. Another cause for caution is that is bled US$5.4m in negative free cash flow over the last twelve months. So suffice it to say we consider the stock very risky. When I consider a company to be a bit risky, I think it is responsible to check out whether insiders have been reporting any share sales. Luckily, you can click here ito see our graphic depicting Rainbow Rare Earths insider transactions.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.