Are The Reject Shop Limited's (ASX:TRS) Mixed Financials The Reason For Its Gloomy Performance on The Stock Market?

It is hard to get excited after looking at Reject Shop's (ASX:TRS) recent performance, when its stock has declined 12% over the past three months. It is possible that the markets have ignored the company's differing financials and decided to lean-in to the negative sentiment. Stock prices are usually driven by a company’s financial performance over the long term, and therefore we decided to pay more attention to the company's financial performance. In this article, we decided to focus on Reject Shop's ROE.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. Put another way, it reveals the company's success at turning shareholder investments into profits.

View our latest analysis for Reject Shop

How Do You Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Reject Shop is:

5.7% = AU$8.7m ÷ AU$152m (Based on the trailing twelve months to December 2020).

The 'return' is the amount earned after tax over the last twelve months. That means that for every A$1 worth of shareholders' equity, the company generated A$0.06 in profit.

What Has ROE Got To Do With Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

Reject Shop's Earnings Growth And 5.7% ROE

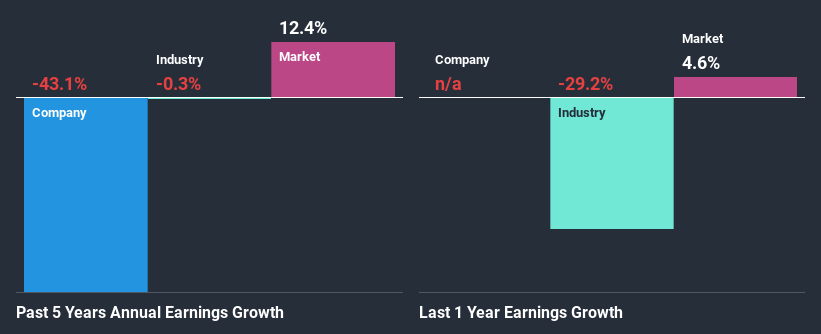

On the face of it, Reject Shop's ROE is not much to talk about. However, its ROE is similar to the industry average of 6.3%, so we won't completely dismiss the company. But Reject Shop saw a five year net income decline of 43% over the past five years. Remember, the company's ROE is a bit low to begin with. Hence, this goes some way in explaining the shrinking earnings.

As a next step, we compared Reject Shop's performance with the industry and found thatReject Shop's performance is depressing even when compared with the industry, which has shrunk its earnings at a rate of 0.3% in the same period, which is a slower than the company.

Earnings growth is a huge factor in stock valuation. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. This then helps them determine if the stock is placed for a bright or bleak future. Is Reject Shop fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Reject Shop Using Its Retained Earnings Effectively?

While the company did payout a portion of its dividend in the past, it currently doesn't pay a dividend. This implies that potentially all of its profits are being reinvested in the business.

Based on the latest analysts' estimates, we found that the company's future payout ratio over the next three years is expected to hold steady at 32%. Regardless, the future ROE for Reject Shop is predicted to rise to 11% despite there being not much change expected in its payout ratio.

Conclusion

Overall, we have mixed feelings about Reject Shop. Even though it appears to be retaining most of its profits, given the low ROE, investors may not be benefitting from all that reinvestment after all. The low earnings growth suggests our theory correct. That being so, the latest industry analyst forecasts show that the analysts are expecting to see a huge improvement in the company's earnings growth rate. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.