Retail Supermarkets Outlook: Can Strategies Pare Margin Woes?

An upbeat economic scenario has been favoring the retail supermarket industry. Notably, a strong labor market, rising disposable income, tax cuts and higher consumer spending have been major catalysts — also evident from the uptick in retail sales in July that rose 0.4% from June.

The supermarket space is expected to continue benefiting from consumers’ increased spending on groceries. To top it off, strategic growth efforts like enhancing store experience, enriching assortments, making innovation, strengthening online business and optimizing costs paint a bright picture for the space.

The industry underwent a massive change after Amazon (AMZN) took over Whole Foods Market. The online giant’s move impelled several players to sharpen their act to survive the competitive frenzy. Incidentally, companies have been stepping up their omni-channel game through alliances, mergers and acquisitions. Also, supermarket retailers are adopting ways to improve delivery and payment systems, among other initiatives, to expand in the booming online grocery space.

Though companies are trying all means to combat competition, costs associated with such endeavors, intense promotional activities and a compelling pricing strategy have been denting margins. Apart from this, competition from private-label brands, elevated transportation costs, high wage expenses and food cost inflation remain hurdles. Nevertheless, we expect supermarket players to continue witnessing improved revenue trends, while a higher mix of e-commerce sales may keep margins under pressure.

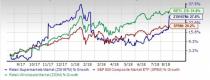

Industry Outperforms Shareholder Returns

Constant efforts to strengthen both brick-and-mortar and dot.com businesses have been driving a sizeable number of stocks in the space. However, intense competition and escalating costs have been impeding growth for some.

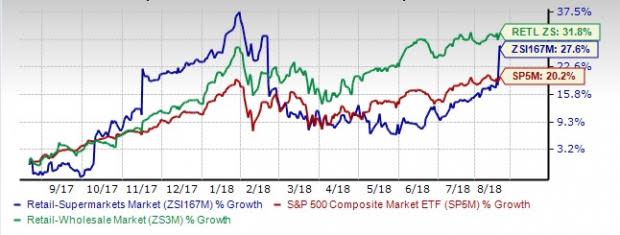

Notably, the Zacks Retail – Supermarkets Industry within the broader Zacks Retail – Wholesale Sector has outperformed the S&P 500, though it lagged its own sector over the past year.

While the stocks in this industry have collectively gained 27.6%, the Zacks S&P 500 Composite and Zacks Retail – Wholesale Sector have rallied 20.2% and 31.8%, respectively.

One-Year Price Performance

Supermarket Stocks Seem Pricey

Owing to the industry’s outperformance in the past year, the valuation looks somewhat expensive when compared with the broader market. One might get a good sense of the industry’s relative valuation by looking at its price-to-earnings ratio (P/E), which is the most appropriate multiple for valuing Retail – Wholesale stocks because their earnings are effective in gauging performance.

Generally, the price of a stock rallies on a rise in earnings. As forecasts for earnings move higher, demand for the stock should drive its price. If the P/E of a stock is rising steadily, it means that investors are pinning hopes on the company’s inherent strength.

This ratio essentially measures a stock’s current market value relative to its earnings performance. Investors believe that the lower the P/E, the higher will be the value of the stock.

The industry currently has a trailing 12-month P/E ratio of 20.9, which is lower than the high level of 23.3 over the past year but above the median level of 19.4. This indicates limited upside potential.

The space also looks quite expensive when compared with the market at large, as the trailing 12-month P/E ratio for the S&P 500 is 19.7 and the median level is 20.1.

Price-to-Earnings Ratio (TTM)

Does Earnings Projection Look Favorable for the Industry?

Amid a highly competitive environment, stocks in the Retail – Supermarkets industry are likely to continue driving shareholder returns on the back of their efforts to improve merchandise, keep pace with changing shopping patterns as well as consumers’ growing preference for organic and natural food.

But what really matters to investors is whether this group has the potential to perform better than the broader market in the quarters ahead. While the earlier valuation analysis reflects that there is little upside left, there are enough reasons for investors to continue looking for a good entry point.

One reliable measure that can help investors understand the industry’s prospects of solid price performance is its earnings outlook. Empirical research shows that earnings outlook for the industry, a reflection of the earnings revisions trend for the constituent companies, has a direct bearing on its stock market performance.

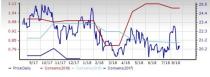

The Price & Consensus chart for the industry shows the market's evolving bottom-up earnings expectations for the industry and its aggregate stock market performance. The red line in the chart represents the Zacks measure of consensus earnings expectations for 2019, while the light blue line represents the same for 2018.

Price and Consensus: Zacks Retail – Supermarkets industry

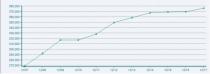

This becomes clearer when we focus on the aggregate bottom-up EPS revisions trend. The chart below shows the evolution of aggregate consensus expectations for 2018.

Please note that the $4.01 EPS estimate for the industry for 2018 is not the actual bottom-up dollar EPS estimate for every company in the Zacks Retail – Supermarkets industry, but rather an illustrative aggregate number created by our proprietary analytics model. The key factor to keep in mind is not earnings of $4.01 per share of the industry for 2018, but how this estimate has evolved recently.

Current Fiscal Year EPS Estimate Revisions

As you can see here, the $4.01 EPS estimate for 2018 is up from $3.99 at the end of July and $3.78 at this time last year. Though the current estimate has increased by a couple of cents, after remaining stable in the past three months, it has actually declined from its peak of $4.04 attained in the month of April. Quite apparent, the sell-side analysts covering the companies in the Zacks Retail – Wholesale industry have been treading with caution while revising their estimates.

Zacks Industry Rank Indicates Dim Prospects

Players in the supermarket space, especially traditional grocers, are bearing the brunt of mounting competition from other brick-and-mortar players as well as Amazon. This has compelled players to strengthen their e-commerce operations and undertake efforts like increased promotions and compelling pricing, which come at the cost of margins. Moreover, rising wages and transportation costs remain hurdles for many players in the supermarket industry.

These factors are also reflected in the group’s Zacks Industry Rank, which is basically the average of the member stocks’ Zacks Rank.

The Zacks Retail – Supermarkets industry currently carries a Zacks Industry Rank #234, which places it in the bottom 9% of more than 250 Zacks industries. Our research shows that the top 50% of the Zacks-ranked industries outperforms the bottom 50% by a factor of more than 2 to 1.

Our proprietary Heat Map shows that the industry’s rank has deteriorated, when compared to its rank eight weeks ago.

Retail – Supermarkets Space: Earnings & Revenue Trends

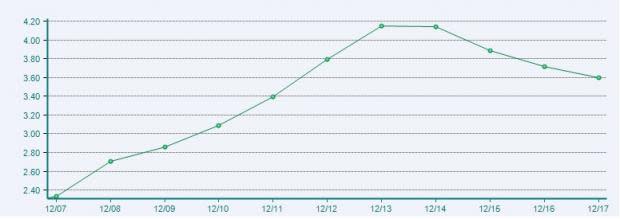

The past earnings trend of the supermarkets space reveals that the group has been witnessing a declining trend since 2015, prior to which it was seen rising for quite some time.

Retail – Supermarkets EPS

Nevertheless, the top-line performance of the Zacks Retail – Supermarkets industry has been impressive and has not showed any decline since 2007.

Retail – Supermarkets Revenues

Bottom Line

A rosy economic environment and an insight into the raised retail sales projections give out positive signals for the Retail – Supermarkets industry. The recent retail sales forecast for the full year by National Retail Federation shows growth of at least 4.5%, up from the prior view of 3.8-4.4%. Incidentally, a 4.9% year-over-year increase in July retail sales also looks quite encouraging. Clearly, there is a reason why players in the industry are upbeat.

That said, the space is likely to gain from the companies’ omni-channel efforts. While digital transformation has become the need of the hour, the importance of brick-and-mortar remains, especially for grocery shoppers. Thus, companies are set to gain from store expansion and remodelling, e-commerce strategies and efforts to replenish assortments given consumers’ willingness to spend on premium and organic foods.

Talking of e-commerce strategies, supermarket players are exploiting each nook and cranny of the booming online grocery space. From same-day deliveries to upgraded payment systems, they are leaving no stone unturned to make the most of this money-spinning business. However, increased mix of e-commerce sales has been straining margins of major players in the supermarkets space. Also, increased promotions to boost traffic, a compelling pricing strategy, competition from private-label brands and escalating costs remain deterrents.

On that note, we have highlighted a stock that investors should pass up.

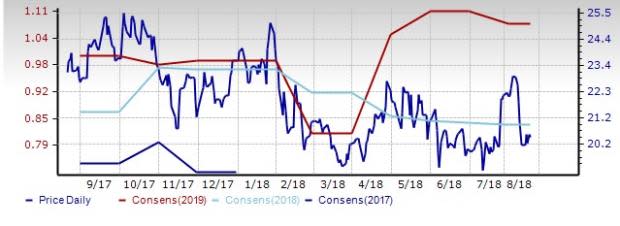

Companhia Brasileira de Distribuicao (CBD) has lost 10.4% in the past year. It carries a Zacks Rank #4 (Sell). The Zacks Consensus Estimate for current fiscal EPS has dropped a notch in the last 30 days.

Price and Consensus: Companhia Brasileira

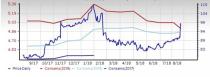

Nonetheless, the strategic endeavors undertaken by some of the big players have placed them favorably in the group. We bring you two such stocks that you may prefer to hold for now.

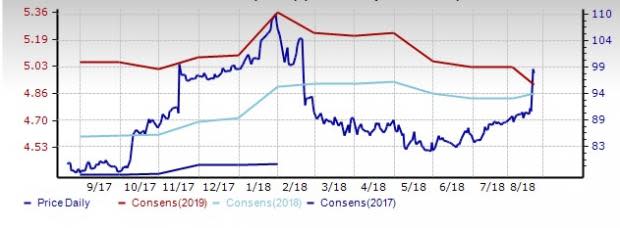

Walmart Inc. (WMT): This world’s largest retailer has gained close to 26% over the past year. The company, which has seen its earnings estimates for the current fiscal increase by 4 cents over the past seven days, currently carries a Zacks Rank #3 (Hold).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Price and Consensus: Walmart

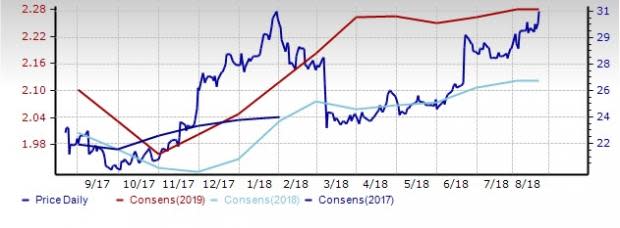

The Kroger Co. (KR), which has rallied more than 41% in the past year, also carries a Zacks Rank #3. The Zacks Consensus Estimate for current fiscal EPS has remained stable in the last 30 days.

Price and Consensus: Kroger

Looking for Stocks with Skyrocketing Upside?

Zacks has just released a Special Report on the booming investment opportunities of legal marijuana.

Ignited by new referendums and legislation, this industry is expected to blast from an already robust $6.7 billion to $20.2 billion in 2021. Early investors stand to make a killing, but you have to be ready to act and know just where to look.

See the pot trades we're targeting>>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Walmart Inc. (WMT) : Free Stock Analysis Report

The Kroger Co. (KR) : Free Stock Analysis Report

Companhia Brasileira de Distribuicao (CBD) : Free Stock Analysis Report

Amazon.com, Inc. (AMZN) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research