Shopify: Reassessing the E-commerce Powerhouse Amid Diminishing Profitability

E-commerce giant Shopify (NYSE:SHOP) has taken its investors on a rollercoaster ride over the years. Nevertheless, its growth-at-all-costs strategy paid off for early investors, with Shopify stock rising over 200% in the past five years.

SHOP Data by GuruFocus

However, its tanked more than 38% last year as the top line growth rate normalized even as the bottom line continued falling. Consequently, its margins have sunk further into the red, with the investing punditry in a fix over whether the stock is worth its price tag.

SHOP Data by NASDAQ:MORN) analysts, its future three to five-year revenue growth estimate is at 21%, a far cry from its growth rates in the past. Gross margins are down significantly at just 46% in the fourth quarter of 2022 compared to 57% in the first quarter of 2021. With the challenging macroeconomic conditions and the risk-off market sentiment, I believe Shopify stock will struggle in the near term.

Profitability erosion

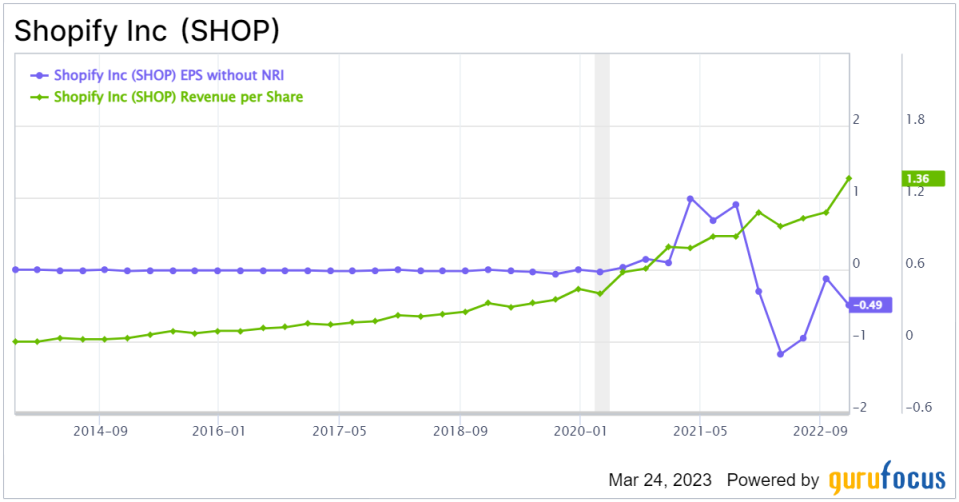

Shopify has grown revenue at a breathtaking pace over the years, but the same cannot be said for its profitability position. Its earnings have been mostly in the red in the past decade, despite the rampant increase in its top line. Consequently, its stock soared to new heights during the bull market but has suffered ever since.

The chart below shows how Shopify's Ebit per share has dropped over the years and how it turned a tide during the pandemic years. However, its results from last year have effectively reversed those gains and then some.

Over the years, Shopify has grown its top line from just $50.3 million in 2013 to a whopping $5.6 billion last year. These impressive growth rates are linked to its aggressive marketing initiatives, quality product offerings and macro tailwinds resulting in widespread e-commerce adoption. As a result, the company posted 85% sales growth in 2020 and 55% in 2021. It even turned profitable over that time.

Nevertheless, it is important to understand that most of these profits were linked to equity investments. Unrealized gains and losses from equity investments are recorded annually on the income statement. With the stock market catching fire during 2021, the company's equity investments increased substantially, resulting in windfall profits. In 2022, the positive impact was effectively reversed, with the company recently reporting $3 billion in unrealized losses. Even without those losses, though, it would be unprofitable. It posted an operating loss of $822 million in 2022, driven by a 61% year-over-year bump in operational costs.

More downside ahead

In all likelihood, Shopify will continue struggling, at least in the short term. For the first quarter of this year, it predicts sales growth in the "high teens," while analysts projected over 20% growth.

To be fair, given the competitive landscape and the macro headwinds, it's tough to foresee a rebound scenario. In fact, GuruFocus' GF Value rank suggests that the company is likely to have a below average performance.

Expecting 40% to 50% growth revenue growth in the future is futile, which throws the spotlight on Shopify's bottom line to make a positive move. Though it shed a ton of value in the past year, its stock still trades at over 9.5 times forward sales estimates. Investors may have paid a premium for Shopify's incredible growth rates in the past, but to be honest, the stock appears to still be trading at a premium even now.

I expect the e-commerce giant to continue suffering from a profitability standpoint. Apart from the challenging business environment, Shopify's business model is such that it needs to continue pumping truckloads of money into marketing to deliver robust revenue growth. Marketing costs are unlikely to come down any time soon, which will pressure its bottom line further.

Takeaway on Shopify

Shopify has been an excellent wealth compounder over the pandemic years but saw its stock price drop precipitously last year as its growth rates normalized. Amidst a challenging macro environment, Shopify's revenue growth has slowed down substantially, putting immense pressure on its bottom line. I don't foresee its future growth rates comparing to its historical averages, even after the risk-off sentiment disappears, as the overall market downturn is only part of the reason why Shopify is struggling.

The bottom line is also misleading because the equity portfolio moves the needle more than the operating business. That's how it became so profitable during the pandemic years, but those gains have effectively been reversed. With a predicted sales growth in the "high teens" for its upcoming quarter, a rebound seems unlikely.

This article first appeared on GuruFocus.