Signet's (SIG) Digital Efforts Promising, Up 26.5% in a Year

Signet Jewelers Limited SIG looks well poised for growth, thanks to its sturdy digital capabilities and a steady progress in its Inspiring Brilliance strategy. Management is consistently integrating the physical stores with advanced virtual experiences through data-driven in-store consultations and services like buy online pickup in-store and curbside options.

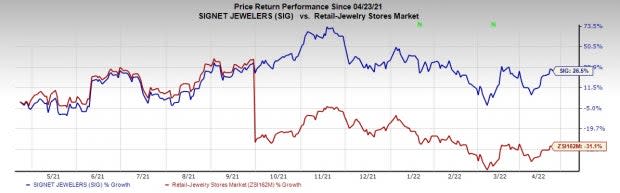

Additionally, robust gains from growth initiatives like advanced connected-commerce capabilities as well as unique banner value propositions and marketing efforts are aiding SIG’s performance. Its Inspiring Brilliance and innovation efforts are also boding well. This jewelry retailer’s shares have gained 26.5% in a year’s time against the industry’s 31.1% plunge. A VGM Score of A coupled with a projected long-term earnings growth rate of 8% for this presently Zacks Rank #2 (Buy) stock further speaks volumes.

Let’s Delve Deeper

Signet’s digital business is a key driver and has been fueling its performance for a while. Management is focused on enhancing the data-analytics capabilities and connected-commerce approach. The connected-commerce strategy helps combining customer experiences, leveraging in store and online as well as mobile and delivery. Such efforts indicate that Signet is continuously focusing on evolving its channel-agnostic retailer capabilities.

Image Source: Zacks Investment Research

SIG added several features and capabilities across its digital platform to offer a seamless customer experience. Signet rolled out Google Business Messages and Apple Business Chat features, which allow customers to engage virtual jewelry consultants in real time or offline from search results or maps. SIG is constantly offering a curbside pickup and virtual consultations, and buy online pick up in store in its several locations.

During fourth-quarter fiscal 2022, e-commerce sales jumped 8.7% year over year to $556 million. Brick-and-mortar sales grew 34.6% year over year to $2.3 billion. North America segment’s e-commerce sales grew 14% year over year, while brick-and-mortar same-store sales jumped 30.6%. Hence, the momentum in the digital realm is likely to continue and keep fueling results ahead.

Signet’s Inspiring Brilliance strategy has been driving the market share gains for a while. The Inspiring Brilliance strategy focuses on expanding big banners, boosting service revenues, broadening the Accessible Luxury and Value segments, as well as accelerating digital commerce among others. As part of the Inspiring Brilliance strategy, SIG makes use of data-driven insights for targeting new and existing customers. SIG’s acquisition of Diamonds Direct, a company known for unique bridal-focused collections, appears encouraging as well.

More Strengths

Going into fiscal 2023, Signet expects to keep gaining from its prudent growth efforts and consumers’ favorable response toward its assortments. For first-quarter fiscal 2023, management projects revenues of $1.78-$1.82 billion, higher than $1.69 billion delivered in the year-earlier quarter.

For fiscal 2023, management expects total revenues of $8.03-$8.25 billion, indicating growth from $7.83 billion delivered in fiscal 2022. Adjusted operating income is anticipated in the range of $921-$974 million, suggesting a rise from $908.1 million recorded last fiscal year. Adjusted earnings per share are envisioned in the bracket of $12.28-$13.00, implying a rise from$12.28 earned in fiscal 2022.

The Zacks Consensus Estimate for sales is currently pegged at $1.81 billion for the first quarter and $8.23 billion for the current fiscal year, indicating respective growth of 7.1% and 5.2% from the corresponding reported figures of the last fiscal year’s comparable period and the full fiscal itself.

Wrapping up, Signet is likely to continue the momentum on the bourses, considering all the above-discussed tailwinds.

More Solid Picks in Retail

A few other top-ranked stocks in the Retail sector that investors can consider are Target TGT, Kohl's KSS and Costco COST.

General merchandise retailer Target is currently Zacks #1 (Strong Buy) Ranked. TGT has an expected earnings per share (EPS) growth rate of 16.5% for three-five years. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Target’s current financial-year sales and EPS suggests growth of 3.5% and 6.7%, respectively, from the corresponding year-ago period’s levels. TGT has a trailing four-quarter earnings surprise of 21.3%, on average.

Kohl's, an omnichannel retailer, currently carries a Zacks Rank of 2. KSS’s bottom line outperformed the Zacks Consensus Estimate by 4.8% in the last reported quarter.

The Zacks Consensus Estimate for Kohl's current financial-year sales suggests growth of 2.5% from the year-ago period’s reading. KSS has an expected EPS growth rate of 8% for three-five years.

Costco, which operates membership warehouses, carries a Zacks Rank of 2 at present. COST has a trailing four-quarter earnings surprise of 13.3%, on average.

The Zacks Consensus Estimate for Costco’s current financial-year sales and EPS suggests growth of 13.5% and 17.6%, respectively, from the corresponding year-ago period’s actuals. COST has an expected EPS growth rate of 9.1% for three-five years.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Target Corporation (TGT) : Free Stock Analysis Report

Kohl's Corporation (KSS) : Free Stock Analysis Report

Costco Wholesale Corporation (COST) : Free Stock Analysis Report

Signet Jewelers Limited (SIG) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research