After Soaring 382% in One Year, What’s Next for Zoom Video?

After surging on COVID-19-related catalysts, investors have cooled on Zoom Video stock. With prices having topped $588.84 per share, the popular remote work play has since moved lower, and now changes hands at around $433 per share.

As the pandemic continues to affect office life, it’s hard to say that Zoom has peaked, as the move towards a permanent remote-work environment may continue even after the pandemic abates.

This trend bodes well for Zoom, and its remote conferencing platform. Even as Wall Street continues to give this stock a rich valuation, shares could continue to gain, albeit at a slower pace.

However, this doesn’t mean that shares won’t head lower in the near-term. As tech giants like Microsoft (MSFT) go after a larger piece of this lucrative market, competitive challenges could make it tough for Zoom to live up to its aggressive growth projections.

So, weighing the long-term trends against the potential risks, what’s the play? One could consider the shares a cautious buy at today’s prices, and a solid buy on any pullback.

Zoom Has a Lot Going For it

Risk-averse investors may be uncomfortable buying Zoom at its current high valuation. However, the bulls make a solid argument as to why it has more runway ahead.

Several big tech names are adopting full-time, remote work policies. Facebook (FB) was one of the first, but now, other major Silicon Valley employers like Salesforce (CRM) are making the leap as well.

Just because Silicon Valley is doing it doesn’t necessarily mean that corporations elsewhere will follow suit, but as we’ve seen with other changes to the working environment, such as open offices, this trend is likely to trickle down to businesses large and small.

Future gains in the share price will likely be more gradual than what we’ve seen recently, but a continued shift to a permanent remote working environment could help push Zoom shares well above their all-time highs.

Downside Risk Going Forward

So far, today’s growth-oriented stock market doesn’t seem too worried about the rich valuation of ZM, but with the stock trading at a high forward P/E ratio of 148.2x, any sort of hiccup may be enough to fuel a near-term move lower.

Why? This frothy valuation is predicated on its expected outsized growth. If the company fails to deliver, a severe sell-off could be on tap, probably not to pre-pandemic price levels, but those buying today could experience heavy losses.

On top of this, the competition in Zoom’s main market is heating up. Rivals like Microsoft, with its Teams communications platform, could give it a run for its money.

Does this mean it’s high time to sell Zoom ahead of these looming risks? Not exactly. Sure, they may put some near-term downward pressure on the stock, but for those with a longer time horizon, there’s still merit to buying shares at today’s prices.

What Analysts are Saying about ZM Stock

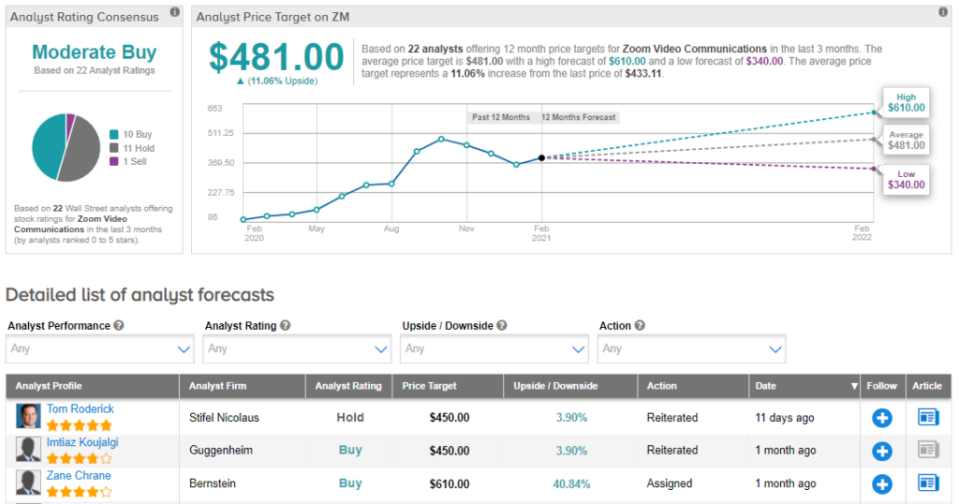

According to TipRanks, Zoom Video has a Moderate Buy consensus rating. With 10 Buy ratings, 11 Hold ratings, and just 1 Sell rating, Wall Street’s sell-side community is largely bullish or on the fence about this stock.

What about price targets? ZM stock has an average analyst price target of $481 per share, implying 11.1% upside potential from today’s prices. (See Zoom Video stock analysis on TipRanks)

Bottom Line

As COVID-19 continues to affect the world, hopes of a rapid recovery have been dashed. This points to continued strength for Zoom Video, and in turn, its stock price.

Yet, keep in mind that shares could still see some downward pressure in the coming months, whether it’s due to a reversal in remote working trends, or from rival tech giants muscling in on its turf.

Bottom line: ZM is still a worthwhile long-term buy at today’s prices, but waiting for a correction to back up the truck might be more prudent.

Disclosure: Thomas Niel held no position in any of the stocks mentioned in this article at the time of publication.

Disclaimer: The information contained herein is for informational purposes only. Nothing in this article should be taken as a solicitation to purchase or sell securities.