Starbucks (SBUX) Rides on Comps & Store Growth, Cost Woes Stay

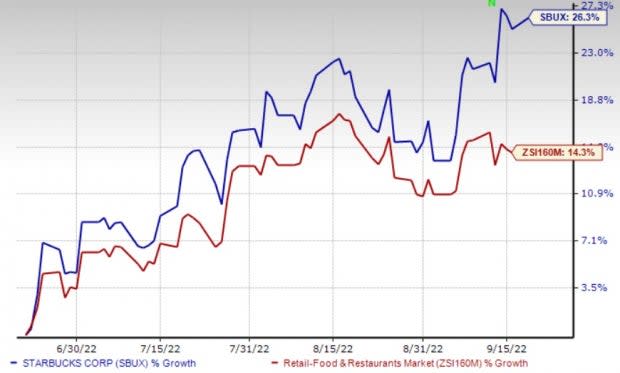

Starbucks Corporation SBUX is very optimistic about its growth opportunities. Store expansion efforts, comps growth and digitalization are likely to drive growth. In the past three months, the company’s shares have gained 26.3% compared with the industry’s increase of 14.3%.

This Zacks Rank #3 (Hold) company has an estimated long-term earnings growth rate of 12.9%. The company’s targeted investments in partners, customers and stores are likely to be the major growth drivers in the long run. This will help it to increase operating margin and drive high-teens non-GAAP EPS growth annually through fiscal 2025.

Growth Drivers

Management is focusing on increasing global market share by judiciously opening stores in new and existing markets, remodeling existing stores, deploying technology, controlling costs and aggressive product innovation, and brand building. Starbucks is focusing on store expansion efforts to drive growth. For fiscal 2023 to 2025, it expects its global store portfolio to increase approximately 7% annually, up from the prior estimate of 6%. In the same period, the company is likely to witness net new store growth of 3-4% annually in the U.S., up from the prior estimate of nearly 3%.

In China, the company is likely to witness net unit growth of roughly 13% annually. By the end of 2025, the company’s global store count is likely to reach 45,000 and by 2030 it is projected to be 55,000. In China, the company expects its store count to increase to 9,000 by 2025, up from the current store count of 5,700.

For fiscal 2023 to 2025, Starbucks anticipates global and U.S. comparable store sales growth between 7% and 9% year over year. The figure is higher than the previous range of 4-5%. For fiscal 2023 to 2025, the company anticipates global revenue to increase in the range of 10-12% annually. The figure is higher than the company’s prior range of 8-10%. Starbucks anticipates robust margin expansion in fiscal 2023, 2024 and 2025. It expects non-GAAP earnings per share to grow between 15% and 20% annually through 2025, up from the prior range of 10-12%.

Image Source: Zacks Investment Research

The company will also benefit from purpose-built store concepts. It will invest an incremental $450 million in the current U.S. store base in fiscal 2023 and will continue to invest in fiscal 2024 and 2025.

The company is also focusing on robust digitization to drive growth. To make Starbucks available to all customers, it is focusing on expanding its Starbucks Delivers program in the United States with a new partner, DoorDash.

Hurdles to Cross

High costs remain a major concern for the company. The company’s margin in third-quarter 2022 was negatively impacted by inflationary pressure along with increased investments in store partner wages and benefits. Reduced traffic in China also added to the woes. However, these were partially offset by higher pricing in North America. On a non-GAAP basis, the operating margin during the fiscal third quarter came in at 16.9%, down from 20.4% reported in the prior-year quarter.

Key Picks

Some better-ranked stocks in the Zacks Retail-Wholesale sector are Tecnoglass Inc. TGLS, Cracker Barrel Old Country Store, Inc. CBRL and Arcos Dorados Holdings Inc. ARCO.

Tecnoglass currently sports a Zacks Rank #1 (Strong Buy). The company has a trailing four-quarter earnings surprise of 24.4%, on average. Shares of the company have increased 2.1% in the past three months. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for TGLS’s 2022 sales and earnings per share (EPS) suggests growth of 28.2% and 47.7%, respectively, from the year-ago period’s levels.

Cracker Barrel currently carries a Zacks Rank #2 (Buy). It has a long-term earnings growth of 6.9%. Shares of the company have declined 21.3% in the past year.

The Zacks Consensus Estimate for CBRL’s 2022 sales and EPS suggests growth of 16.3% and 15.4%, respectively, from the year-ago period’s levels.

Arcos Dorados carries a Zacks Rank #2. It has a long-term earnings growth of 34.4%. Shares of the company have improved 47.9% in the past year.

The Zacks Consensus Estimate for ARCO’s 2022 sales and EPS suggests growth of 27.1% and 104.2%, respectively, from the year-ago period’s levels.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cracker Barrel Old Country Store, Inc. (CBRL) : Free Stock Analysis Report

Starbucks Corporation (SBUX) : Free Stock Analysis Report

Arcos Dorados Holdings Inc. (ARCO) : Free Stock Analysis Report

Tecnoglass Inc. (TGLS) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research