'Lousy system': U.S. official who resigned explains how the student debt crisis got so bad

The student loan crisis has reached epic proportions. And it’s only getting worse.

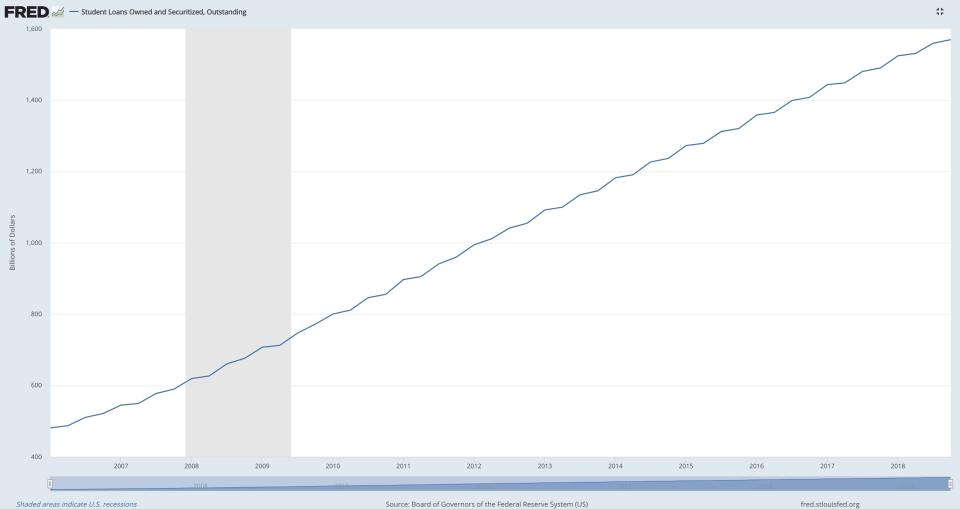

Outstanding balances have grown more than 500% since 2003, according to New York Fed data, bringing the total amount of student debt to $1.5 trillion and counting.

In an interview with Yahoo Finance, former Consumer Financial Protection Bureau (CFPB) Ombudsman and current Executive Director of D.C.-based nonprofit Student Borrower Protection Center Seth Frotman explained that the ongoing crisis is a result of decades of unchecked behavior of various predatory parties and weak government regulation of the industry.

“When trying to understand the student debt crisis, the most important thing to realize is that there weren't these ‘glory days’ when student lending and servicing worked well for families,” said Frotman, who resigned from the CFPB in August 2018.

‘Sleepy backwater in consumer finance’

For the past few decades, the overwhelming majority of student loans were made by banks or private lenders that were then guaranteed by the federal government since the borrowers were students with little to no credit history.

“They were small loans with fewer repayment options, but because of the federal guarantees, banks got their money one way or the other,” Frotman explained. “These were basically rounding errors on a big bank's balance sheet.”

The relatively small student loan market was “considered a sleepy backwater in consumer finance,” Frotman added, so it didn’t receive much attention from regulators.

‘No one was minding the store’

In the meantime, the cost of college began to climb — slowly at first and then exponentially.

In the College Board’s Trends in College Pricing 2018 report, the average cost of tuition at a private non-profit four-year university has now reached $35,830 — more than twice of what a college student would pay in the late 1980s.

To foot the bigger bill, increasingly larger loans were subsequently taken out. The student loan industry began to transform from a sleepy backwater to a thriving, profitable industry.

The issue was that despite the surge in demand, the infrastructure largely remained the same — and the inherent flaws in the system were carried over.

“No one was minding the store,” said Frotman. “On top of this pretty lousy system, we dropped a trillion dollars of new student debt — tripling the size of the student loan market in less than a decade.”

‘Congress bailed out the banks' student loan arms’

The 2008 Financial Crisis only made things worse.

When the financial crisis hit, banks and private lenders were faced with a credit crunch with bad assets on their books.

To make sure they didn’t fail, “Congress bailed out the banks' student loan arms to the tune of hundreds of billions of dollars,” Frotman explained.

That bailout was done to “ensure students access to loans when lending in the nation's credit markets was frozen,” then-Education Secretary Arne Duncan wrote in an opinion piece in the Wall Street Journal in 2009.

“Over the next decade, according to the Congressional Budget Office, the Education Department is slated to subsidize banks to the tune of $87 billion to enable them to make federal student loans,” Duncan continued. “Our real aim is to simply stop using banks as the middle man for student loans.”

But in effect, “taxpayers' money flowed from the federal government to the private sector,” Frotman argued. “In exchange, the government now owned a ton of new student debt.”

The government then ended up signing contracts with the same banks and loan providers that used to manage student loans — familiar names including Navient, Nelnet, Great Lakes, and FedLoan.

Those contracts expire this June, according to plans made by current Education Secretary Betsy DeVos. In 2017, DeVos said that she wanted to start “afresh and pursuing a truly modern loan servicing environment” and to turn “what was a good plan into a great one.”

DeVos even suggested that she would offer an exclusive contract to one company to service billions of dollars of existing student loans.

But nothing much has happened thus far and given the time crunch, the agency is likely to extend existing contracts — an option confirmed by a spokesperson to the New York Times in December.

‘Risk of continued noncompliance’

The Trump administration’s inaction is possibly making the situation even worse.

According to a report by a government watchdog published last month, the Department of Education (DoE) was found to have not held the loan providers accountable to the rules and regulations that it laid out.

The Federal Student Aid (FSA) division within the DoE had, according to the Office of the Inspector General’s report, "rarely used available contract accountability provisions to hold servicers accountable for instances of noncompliance.”

Some of the issues highlighted included Navient’s loan officers misdirecting people to put their loans in forbearance, which would accrue further interest and increase the total loan cost, instead of other repayment options.

Another involved Great Lakes officers automatically placed delinquent accounts into forbearance.

“By rarely holding servicers accountable for instances of noncompliance with Federal loan servicing requirements,” the report concluded, “FSA is not providing servicers with incentives to take actions to mitigate the risk of continued noncompliance that harms students and their families.”

In other words, the report accused the FSA of doing a shoddy job of policing the loan servicers to make sure that they are providing decent — not deceptive — customer service for the millions of borrowers.

Souring student loans

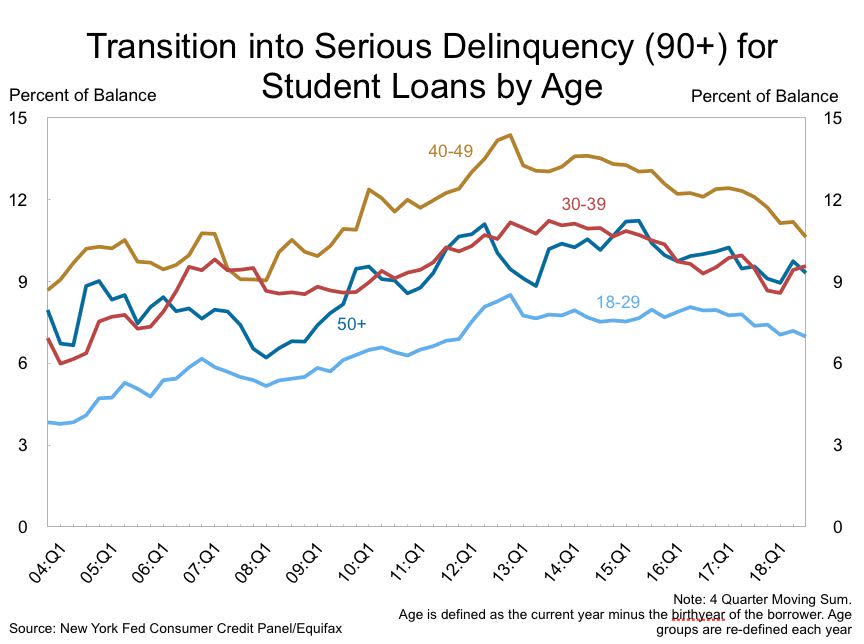

In the meantime, the trillion-dollar student loan debt pile is quickly turning rancid. As of February 2019, according to Student Loan Hero, “11.5% of student loans are 90 days or more delinquent or are in default.”

And that number is likely to be understated, according to the New York Fed, as half of the loans included in the the published rates are deferred or in forbearance status.

Most of those borrowers fall within the ages of 40 and 49, as seen in the graph below. This group, according to the NY Fed’s data, has the worst delinquency rates as compared to other demographics.

The outlook for the future is correspondingly bleak. A Brookings report from last year estimated that by 2023 almost 40% of borrowers are likely to default.

Delinquencies concentrated in the south

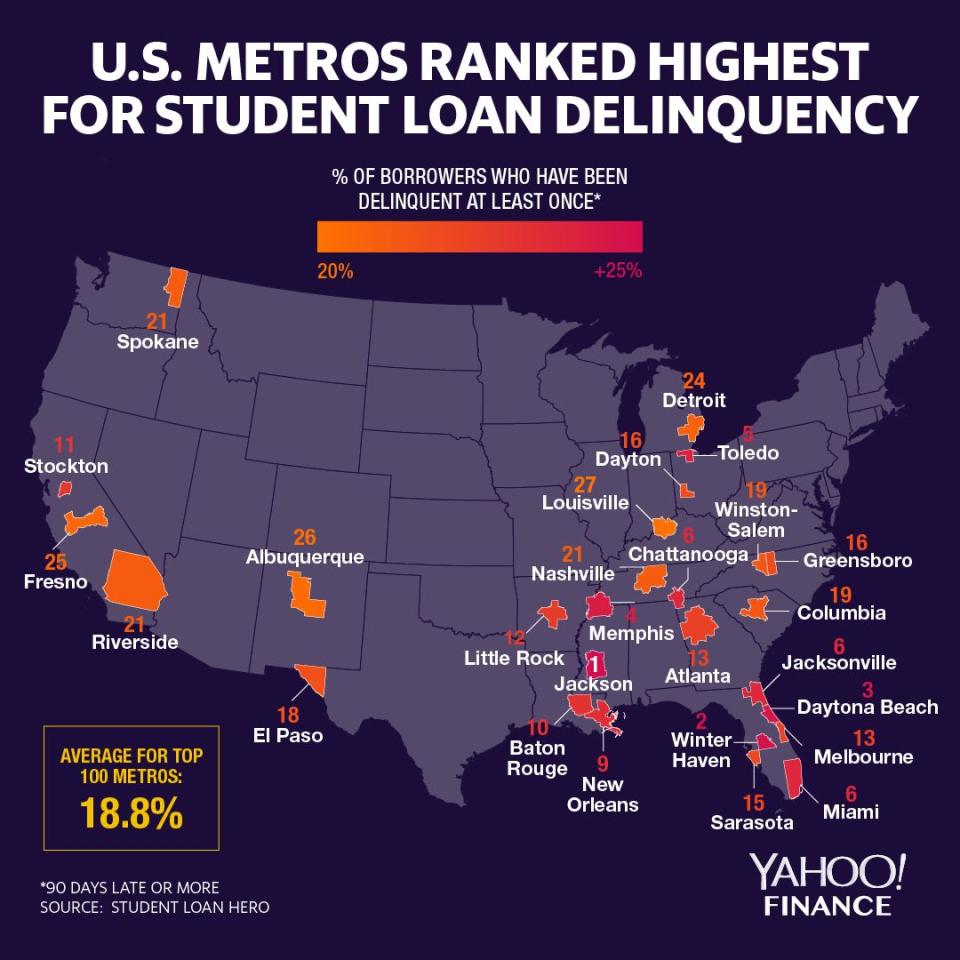

Student Loan Hero also analyzed delinquencies across the U.S. and found that most of the deeply delinquent loans are concentrated in the South.

“A full 14 of the 15 metros at the top of the delinquency list lie below the Mason-Dixon line,” Student Loan Hero reported, “and not one Southern metro made it onto the list of 25 metros with the lowest rates of delinquency.”

And as a result of the student debt crisis, millennial borrowers are increasingly putting off big milestones like starting a family, buying a house, and planning for retirement because of the burden, according to survey by Bankrate.

“Irrational student lending, soaring college costs and the burden of student loans have become a significant issue,” J.P. Morgan Chase CEO Jamie Dimon wrote in his widely-read annual letter. “The impact of student debt is now affecting mortgage credit and household formation… Recent research shows that the burdens of student debt are now starting to affect the economy.”

Dimon highlighted a study by Fed economists from January that found that a $1,000 increase in student debt reduces homeownership rates by 1.8%.

“We would be well-advised to have more properly designed underwriting standards around the creation of student loans,” Dimon wrote. “Direct government lending to students has grown almost 500% over the last 10 years – and it has not all been responsible lending.”

‘Corrosive on economic growth’

Others argue that while the situation is bad, student loan debt isn’t going to topple the economy or cause the next recession.

“The risk of a significant increase in student loan defaults is receding,” Moody’s Analytics Chief Economist Mark Zandi told Yahoo Finance. “The growth in student loan debt has moderated, and is currently in the mid-single digits, close to income growth. Student loan quality is also much improved, with delinquencies on student loan debt falling back to where they were pre-financial crisis.”

Zandi added that at the end of the day, since the loans were federally guaranteed, “student loan defaults are a taxpayer problem, and not a problem for the nation’s banking or financial system.”

At the same time, Zandi agreed with Dimon that student loan debt is “corrosive on economic growth” — because debt was weighing on millennials’ capacity to do things that would help stimulate the economy.

Frotman, for his part, feels a greater sense of urgency.

“In 2019, we live in pretty decent economic times and interest rates are still low, for now... But what happens when unemployment spikes again?” he asked. “What does it look like when interest rates start to go higher?”

Frotman recently testified to the House Financial Services Committee to make his case. In written testimony, he stated: “The student debt crisis is more than a higher education policy issue. It is a significant — perhaps the most significant — consumer finance issue threatening our nation at this time.”

Aarthi is a writer for Yahoo Finance. Follow her on Twitter @aarthiswami.

Read more:

Americans — particularly millennials — are alarmingly late on car payments

Dimon: U.S. student loan debt is ‘now starting to affect the economy’

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, SmartNews, LinkedIn, YouTube, and reddit.