Studio City International Holdings (NYSE:MSC) Takes On Some Risk With Its Use Of Debt

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Studio City International Holdings Limited (NYSE:MSC) does carry debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Studio City International Holdings

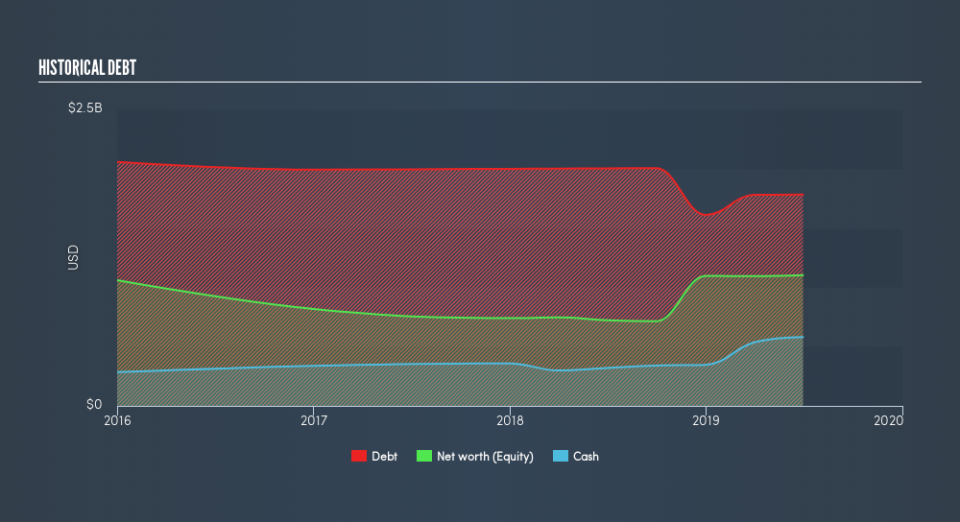

How Much Debt Does Studio City International Holdings Carry?

As you can see below, Studio City International Holdings had US$1.78b of debt at June 2019, down from US$2.00b a year prior. On the flip side, it has US$580.8m in cash leading to net debt of about US$1.20b.

A Look At Studio City International Holdings's Liabilities

According to the last reported balance sheet, Studio City International Holdings had liabilities of US$438.8m due within 12 months, and liabilities of US$1.45b due beyond 12 months. Offsetting these obligations, it had cash of US$580.8m as well as receivables valued at US$63.0m due within 12 months. So it has liabilities totalling US$1.25b more than its cash and near-term receivables, combined.

This deficit is considerable relative to its market capitalization of US$1.61b, so it does suggest shareholders should keep an eye on Studio City International Holdings's use of debt. This suggests shareholders would heavily diluted if the company needed to shore up its balance sheet in a hurry.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

While we wouldn't worry about Studio City International Holdings's net debt to EBITDA ratio of 3.9, we think its super-low interest cover of 1.00 times is a sign of high leverage. In large part that's due to the company's significant depreciation and amortisation charges, which arguably mean its EBITDA is a very generous measure of earnings, and its debt may be more of a burden than it first appears. It seems clear that the cost of borrowing money is negatively impacting returns for shareholders, of late. Fortunately, Studio City International Holdings grew its EBIT by 9.5% in the last year, slowly shrinking its debt relative to earnings. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Studio City International Holdings's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, Studio City International Holdings recorded negative free cash flow, in total. Debt is usually more expensive, and almost always more risky in the hands of a company with negative free cash flow. Shareholders ought to hope for and improvement.

Our View

To be frank both Studio City International Holdings's conversion of EBIT to free cash flow and its track record of covering its interest expense with its EBIT make us rather uncomfortable with its debt levels. But at least it's pretty decent at growing its EBIT; that's encouraging. We're quite clear that we consider Studio City International Holdings to be really rather risky, as a result of its balance sheet health. So we're almost as wary of this stock as a hungry kitten is about falling into its owner's fish pond: once bitten, twice shy, as they say. While Studio City International Holdings didn't make a statutory profit in the last year, its positive EBIT suggests that profitability might not be far away.Click here to see if its earnings are heading in the right direction, over the medium term.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.