Under the shadow of the largest bank merger since the financial crisis, large regional banks CEOs dodged questions on their interest in pursuing similar mergers in this quarter’s earnings calls.

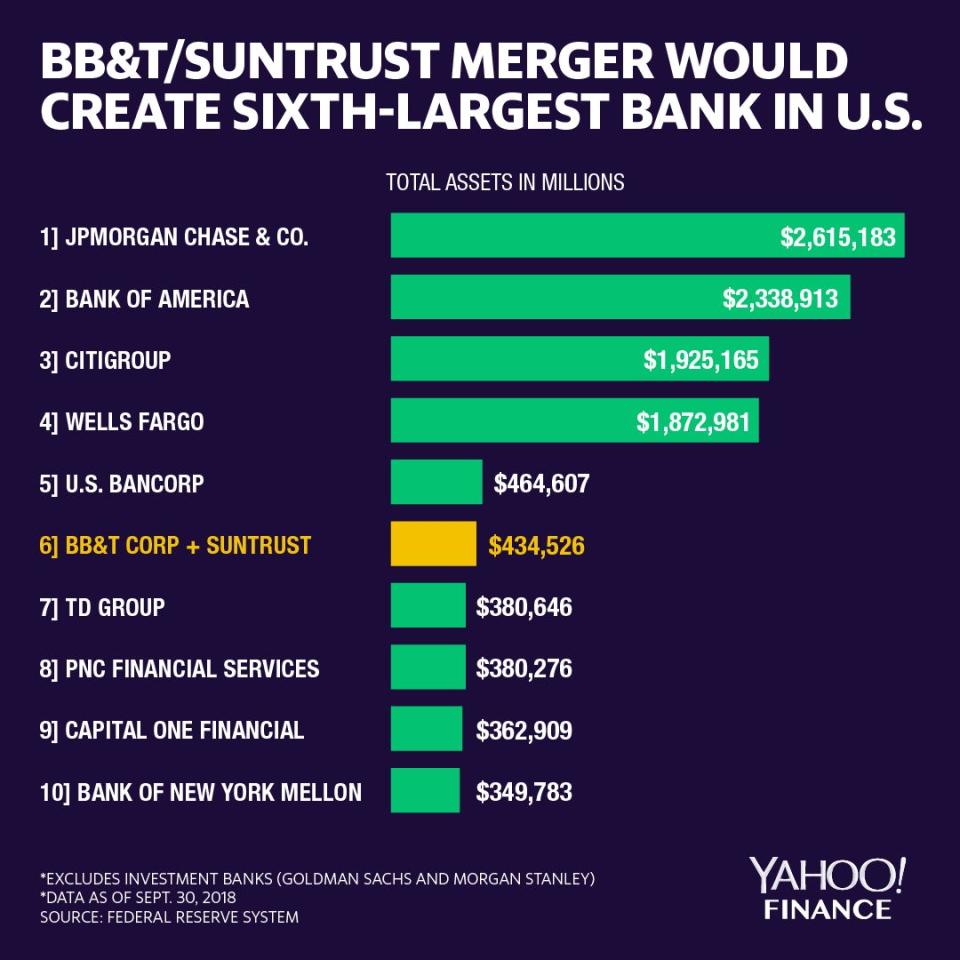

At the same time, they didn’t explicitly rule out interest in M&A. Banks with between $50 billion and $250 billion have been closely watched ever since the February announcement that southeastern powerhouses BB&T (BBT) and SunTrust (STI) were teaming up to build the sixth largest U.S. bank.

In Minneapolis, U.S. Bancorp (USB) CEO Andrew Cecere said April 17 the fifth largest U.S. bank will “consider all options for growth,” a common, non-committal response to analyst questions about M&A.

Other banks had more cleverly-crafted responses.

At Cleveland-based KeyCorp (KEY), CFO Donald Kimble said April 18 that a merger is “not a priority.” Kimble later added that the company, however, is “always looking at areas where we can add additional people, products and capabilities to align with our overall strategies.”

Comerica Inc. (CMA) management used a similar caveat in its April 16 earnings call, at first saying that the company is pleased with its existing team in the key markets of California, Texas, and Michigan.

“That doesn't say we would look at the possibility of an acquisition,” CEO Ralph Babb said April 16, before adding, “But it would be in those markets as it would have to fit from a number of different ways.”

Still, bank analysts say the $28.2 billion deal to couple BB&T and SunTrust will spur industry consolidation, hinting that the regional banks’ vague commentary could be masking boardroom deliberations. The BB&T and SunTrust deal, for example, was the result of years of discussions that came to fruition amid favorable regulatory changes and the need to build digital scale.

Former BB&T CEO John Allison, who headed the North Carolina bank from 1989 to 2008, told Yahoo Finance April 23 that he had tried to “work it out” with SunTrust during his time there but was unable to “put together all the cultural issues.”

“I think that’s going to spur some more acquisitions,” Allison said, applauding the deal for the scalability of tech and the opportunity to close branches.

‘Dusting off the playbook’

To be fair, the floodgates did not open immediately after BB&T and SunTrust in February announced their “merger of equals,” in which two companies of comparable size come together.

New regulatory changes signed into law by President Trump last year raised the threshold for extra regulatory scrutiny from $50 billion to $250 billion. In theory, those changes would bring regional banks in that range to the negotiating table on the promise of a deal that would not trigger added regulatory compliance costs.

Jay Langan, a partner at Deloitte who advises banks on M&A, told Yahoo Finance that banks are moving slowly, preferring to spend the early months of 2019 strategizing and researching possible deals for the second half of 2019. Some banks are taking the time to refresh themselves on the M&A market, with some buyers having been on the sidelines for the last 10 years.

“Institutional knowledge of deal making is probably a little bit rusty,” Langan said. “And they’re dusting off their playbooks and maybe rewriting it in some cases.”

Langan said he is not expecting many more mergers of equals; he sees $100 billion-sized banks targeting companies with between $20 billion and $50 billion.

The M&A market could also heat up in the fintech space, since Federal Reserve recently tweaked the definition of bank “control” that would make it easier for banks to buy fintech companies. Under the current framework, banks wanting to buy fintech firms risked forcing the startup to shed its nonfinancial ventures due to rules on what banks can and cannot do by charter.

Too big and too expensive?

Some worry that bank consolidation risks creating new “too big to fail” banks. On Capitol Hill, a wave of concern from the likes of California Democrat Maxine Waters and Massachusetts Democrat Elizabeth Warren raised questions over whether mergers were reducing competition and hurting consumers.

The Federal Deposit Insurance Corporation held its first public meeting to field comments on the BB&T and SunTrust merger Thursday morning in Charlotte, where the to-be-named merged company plans on planting its new headquarters.

SunTrust CEO Bill Rogers acknowledged the concerns over too big to fail, but insisted that the combined company would increase competition that challenges the “concentration of systemic risk at the top of the market,” likely referring to the big four banks JPMorgan Chase (JPM), Bank of America (BAC), Citigroup (C), and Wells Fargo (WFC).

“Let me assure you, in the case of this merger, bigger doesn’t mean riskier,” Rogers said in prepared remarks.

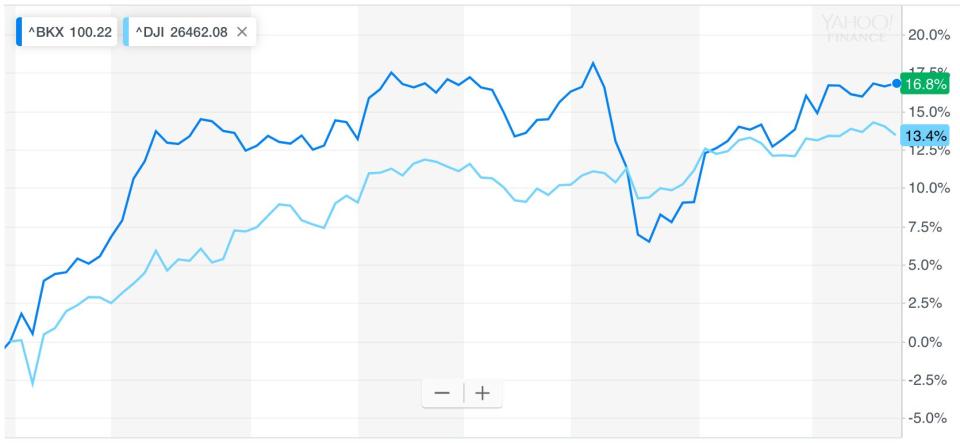

But there might be a market reason for the big banks not to merge anyway: huge price tags. Gregory McGahan, a partner focused on deals at PricewaterhouseCoopers, told Yahoo Finance that bank stocks are trading very high when looking at price to tangible book value — the favored metric for M&A valuation in the banking industry.

The BKW Nasdaq Bank Index (^BKX), which tracks the leading U.S. banks and thrifts, has climbed 17% since the beginning of the year, recovering most of the losses in the market-wide sell-off at the end of 2018. A PwC report released Thursday noted that the average price to tangible book value for all bank deals in the first quarter of this year was 1.58x.

“Pricing is just high,” McGahan said. “People are concerned about the back half of 2019 and if prices come down, it is better to wait.”

Brian Cheung is a reporter covering the banking industry and the intersection of finance and policy for Yahoo Finance. You can follow him on Twitter @bcheungz.

Bank investors face a 'conundrum' in an inverting yield curve

St. Louis Fed President on December rate hike: 'It didn't come off very well'

St. Louis Fed President 'hasn't lost confidence' yet in economy

NY Fed's Williams: Yield curve 'not telling us we're about to have a recession'

Congress may have accidentally freed nearly all banks from the Volcker Rule