T Rowe Price Equity Income Fund Goes 2-for-2 in Financial Services Sector

- By James Li

John Linehan, manager of the T Rowe Price Equity Income Fund (Trades, Portfolio), invests in companies expected to pay above-average dividends and trade below their intrinsic values. During the first quarter, the guru increased his stake in Wells Fargo & Co. (WFC) and US Bancorp (USB). Linehan also trimmed his position in Bank of America Corp. (BAC) and American Express Co. (AXP).

Warning! GuruFocus has detected 1 Warning Sign with WFC. Click here to check it out.

The intrinsic value of WFC

Wells Fargo

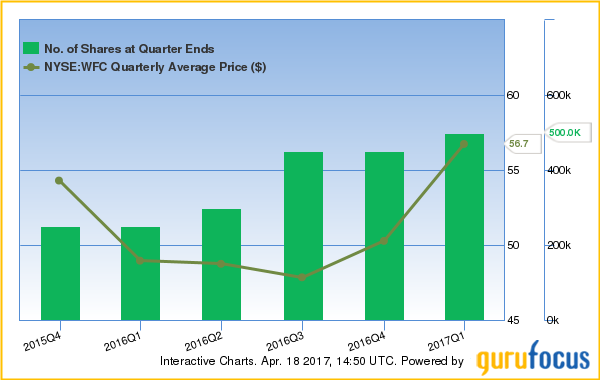

Linehan boosted his Wells Fargo position 27.30%, purchasing 2 million shares at an average price of $56.74. With this transaction, the manager increased his portfolio 0.51%.

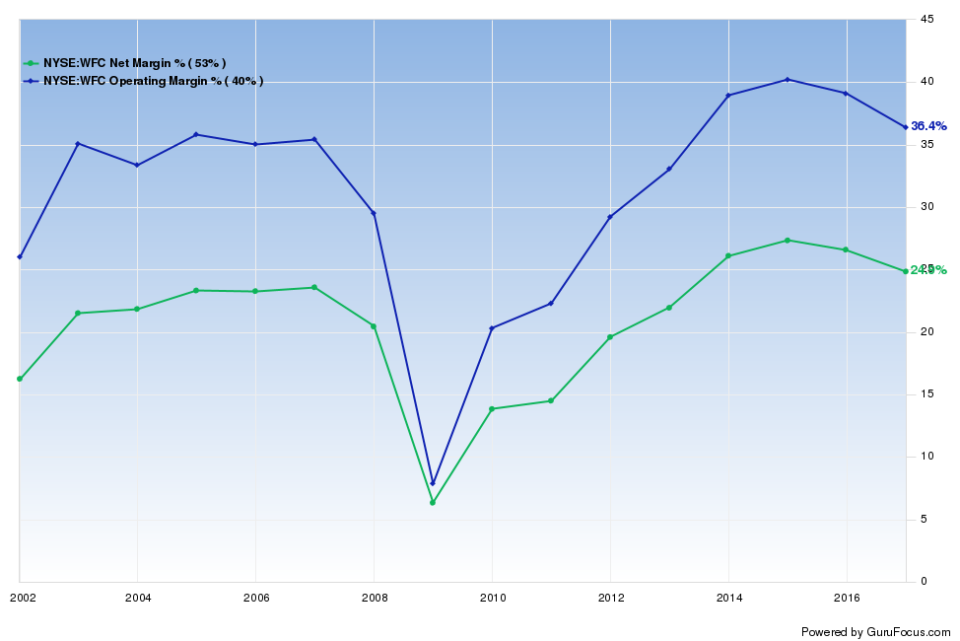

As discussed in a previous article, Wells Fargo produced solid earnings during the quarter. Even though the company's overall profitability ranks a modest 5 out of 10, the bank still has expanding operating margins and consistent revenue per share growth. Wells Fargo's operating and net margins are near a 10-year high and outperform 62% and 57% of global banks.

Jerome Dodson (Trades, Portfolio) and Manning & Napier Advisors Inc. also boosted its position in Wells; the former increased his position 11.11% while the latter added 5.29%.

US Bancorp

The T Rowe Price Group Inc. (TROW) fund manager increased his U.S. Bank position 124.1%, adding 2.755 million shares at an average price of $53.32. With this transaction, Linehan expanded his portfolio 0.65%.

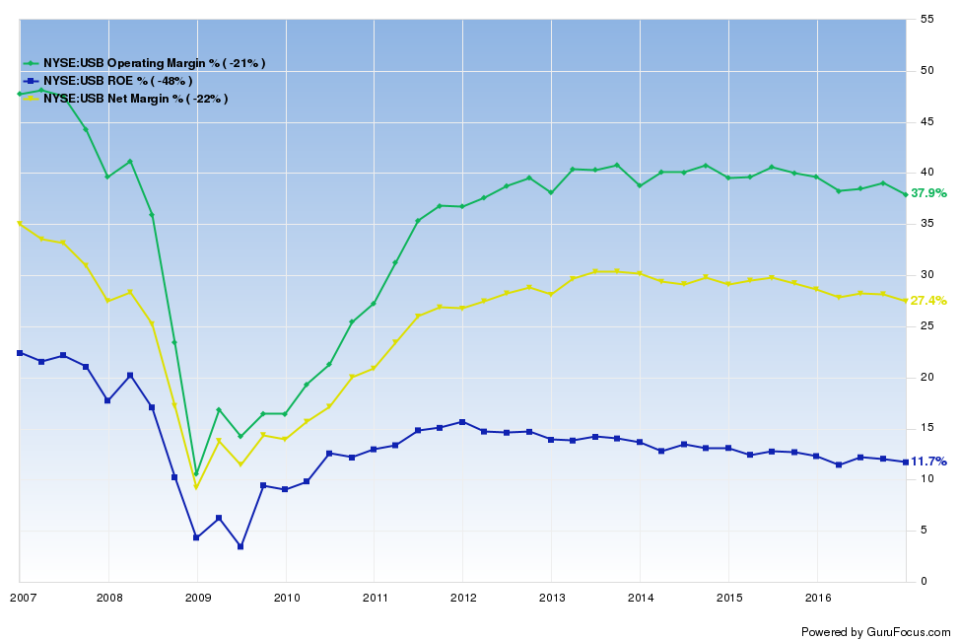

U.S. Bank has a modest financial strength rank of 5. Although U.S. Bank's interest coverage outperforms 80% of competitors, the company's interest coverage is slightly less than Ben Graham's threshold of 5. Additionally, the regional bank only has 33 cents in cash per $1 in debt.

Despite poor cash-debt ratios, U.S. Bank has a profitability rank of 6, suggesting moderately strong growth potential. Even though the company's operating and net margins leveled off since 2011, these margins still outperform over 66% of competitors.

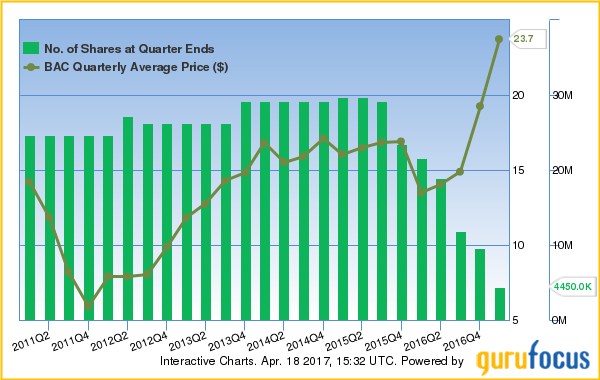

Bank of America

Linehan chopped 53.89% of his stake in Bank of America, selling 5.2 million shares at an average price of $23.73. With this transaction, the guru pared 0.52% of his portfolio.

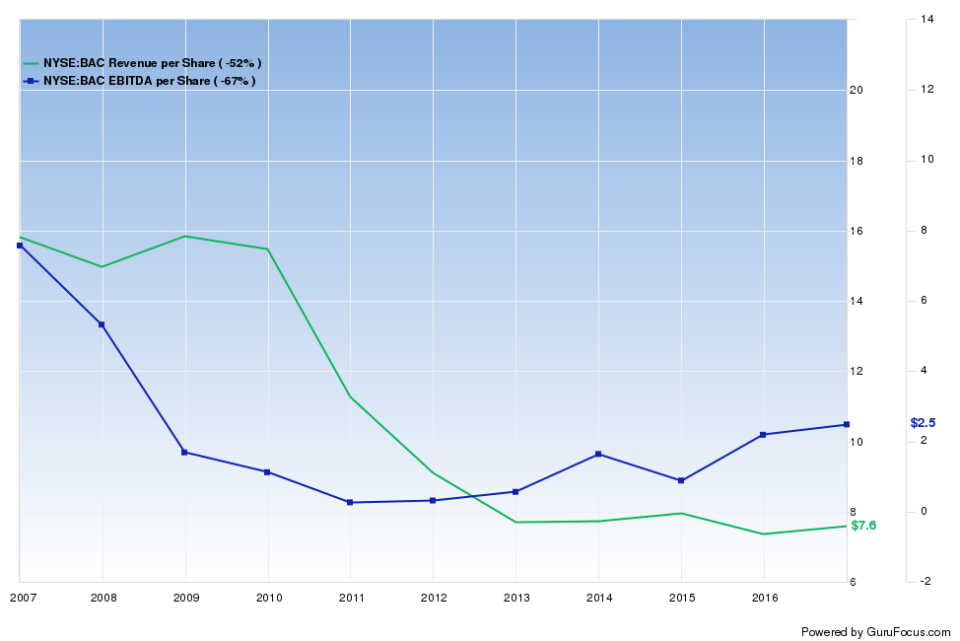

The North Carolina global bank has a profitability rank of 3, suggesting low growth potential. Although the company's operating and net margins are near a 10-year high, Bank of America has consistent revenue per share decline during the past 10 years. The company's three-year revenue growth of -0.70% underperforms 73% of competitors.

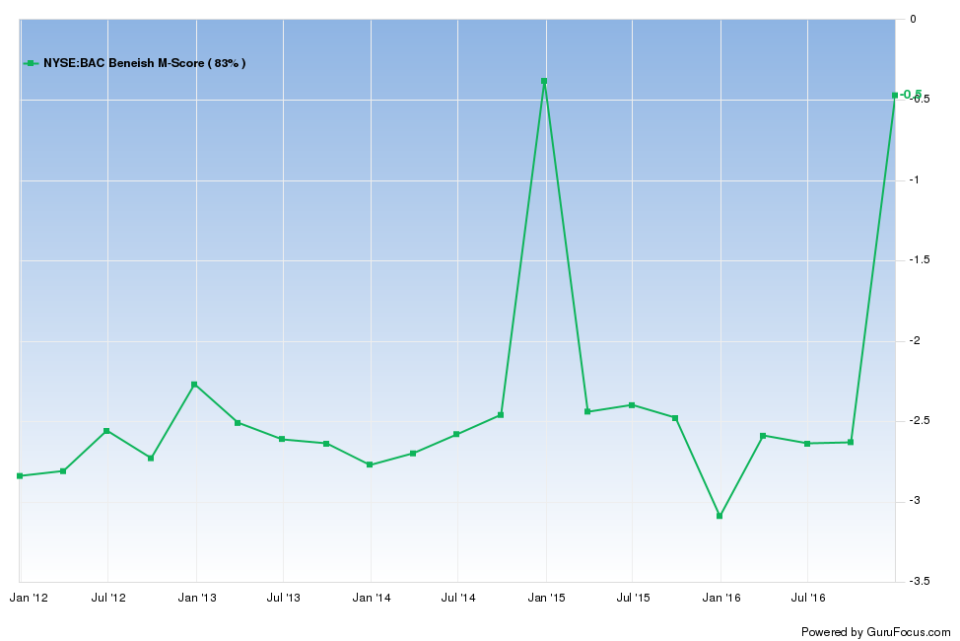

With a Beneish M-score of -0.47, Bank of America may have manipulated its earnings results. Figure 1 shows the detailed breakdown of the company's M-score for the past 10 quarters.

Figure 1: Bank of America Beneish M-score breakdown, past 10 quarters

Among the components of the Beneish score, Bank of America's days sales in receivables index (DSRI) is the most volatile, ranging from approximately 0.3062 to 3.4059 during the past 10 quarters. During fourth-quarter 2014 and fourth-quarter 2016, the bank may have inflated its revenues.

As the bank has decreasing growth potential, several gurus trimmed their Bank of America positions. Steven Romick (Trades, Portfolio) and the Yacktman Fund (Trades, Portfolio) sold 6.93% and 23.08% of their stakes in Bank of America.

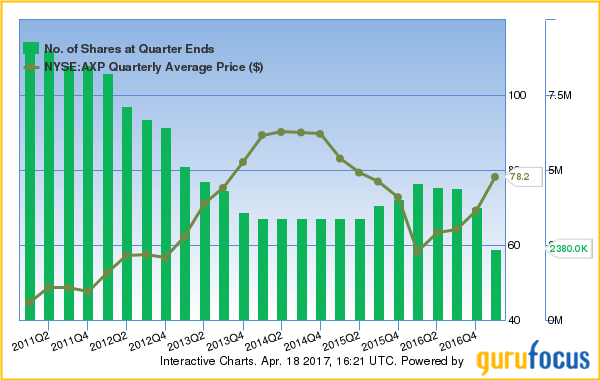

American Express

Linehan knocked off 36.70% of his stake in American Express, selling 1.38 million shares at an average price of $78.18. With this transaction, the guru trimmed 0.47% of his portfolio.

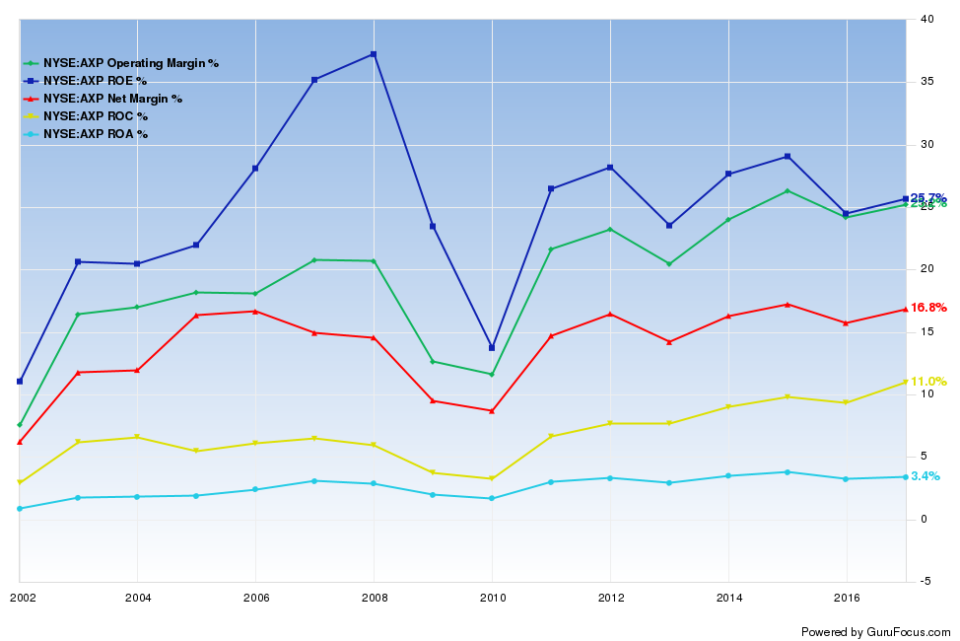

The New York financial services company has moderately strong growth potential with a profitability rank of 6 and a GuruFocus business predictability rank of 3.5 stars. While the company's operating and net margins outperform just 57% of competitors, the margins are near a 10-year high. Additionally, American Express' return on equity outperforms 88% of global credit services companies.

Despite high profitability and growth potential, American Express is moderately overvalued. Although the company trades below its Peter Lynch earnings line, the share price is near a two-year high. Additionally, American Express's price-book (P/B) ratio ranks lower than 82% of competitors.

As the company has declining value potential, Romick sold 41.29% of his stake in American Express.

Disclosure: I do not have positions in the stocks mentioned in this article.

Start a free seven-day trial of Premium Membership to GuruFocus.

This article first appeared on GuruFocus.

Warning! GuruFocus has detected 1 Warning Sign with WFC. Click here to check it out.

The intrinsic value of WFC