Should You Be Tempted To Sell Masonite International Corporation (NYSE:DOOR) Because Of Its P/E Ratio?

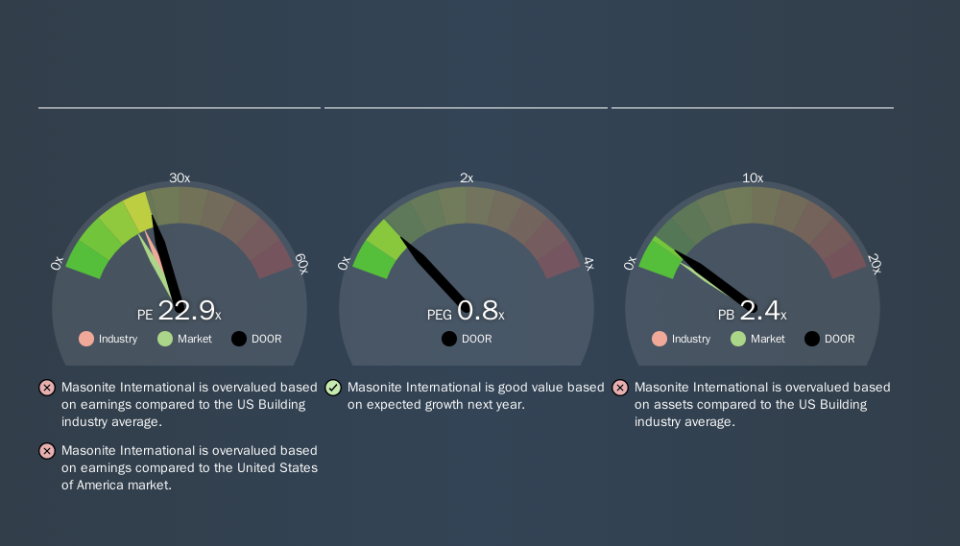

This article is written for those who want to get better at using price to earnings ratios (P/E ratios). We'll look at Masonite International Corporation's (NYSE:DOOR) P/E ratio and reflect on what it tells us about the company's share price. What is Masonite International's P/E ratio? Well, based on the last twelve months it is 22.94. That is equivalent to an earnings yield of about 4.4%.

Check out our latest analysis for Masonite International

How Do You Calculate A P/E Ratio?

The formula for price to earnings is:

Price to Earnings Ratio = Share Price ÷ Earnings per Share (EPS)

Or for Masonite International:

P/E of 22.94 = $57.20 ÷ $2.49 (Based on the trailing twelve months to June 2019.)

Is A High Price-to-Earnings Ratio Good?

A higher P/E ratio implies that investors pay a higher price for the earning power of the business. All else being equal, it's better to pay a low price -- but as Warren Buffett said, 'It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price.

Does Masonite International Have A Relatively High Or Low P/E For Its Industry?

We can get an indication of market expectations by looking at the P/E ratio. As you can see below, Masonite International has a higher P/E than the average company (19.7) in the building industry.

That means that the market expects Masonite International will outperform other companies in its industry. Shareholders are clearly optimistic, but the future is always uncertain. So investors should always consider the P/E ratio alongside other factors, such as whether company directors have been buying shares.

How Growth Rates Impact P/E Ratios

P/E ratios primarily reflect market expectations around earnings growth rates. Earnings growth means that in the future the 'E' will be higher. That means unless the share price increases, the P/E will reduce in a few years. And as that P/E ratio drops, the company will look cheap, unless its share price increases.

Masonite International's earnings per share fell by 55% in the last twelve months. But it has grown its earnings per share by 50% per year over the last three years.

Don't Forget: The P/E Does Not Account For Debt or Bank Deposits

One drawback of using a P/E ratio is that it considers market capitalization, but not the balance sheet. Thus, the metric does not reflect cash or debt held by the company. The exact same company would hypothetically deserve a higher P/E ratio if it had a strong balance sheet, than if it had a weak one with lots of debt, because a cashed up company can spend on growth.

Such expenditure might be good or bad, in the long term, but the point here is that the balance sheet is not reflected by this ratio.

How Does Masonite International's Debt Impact Its P/E Ratio?

Masonite International's net debt equates to 48% of its market capitalization. While it's worth keeping this in mind, it isn't a worry.

The Verdict On Masonite International's P/E Ratio

Masonite International has a P/E of 22.9. That's higher than the average in its market, which is 17.6. With modest debt but no EPS growth in the last year, it's fair to say the P/E implies some optimism about future earnings, from the market.

Investors have an opportunity when market expectations about a stock are wrong. People often underestimate remarkable growth -- so investors can make money when fast growth is not fully appreciated. So this free visual report on analyst forecasts could hold the key to an excellent investment decision.

But note: Masonite International may not be the best stock to buy. So take a peek at this free list of interesting companies with strong recent earnings growth (and a P/E ratio below 20).

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.