Will Thermo Fisher's (TMO) Q2 Earnings Surpass Expectations?

Thermo Fisher Scientific, Inc. TMO, the MA-based medical instruments manufacturer, is expected to beat expectations when it reports second-quarter 2017 results on Jul 26, before the market opens.

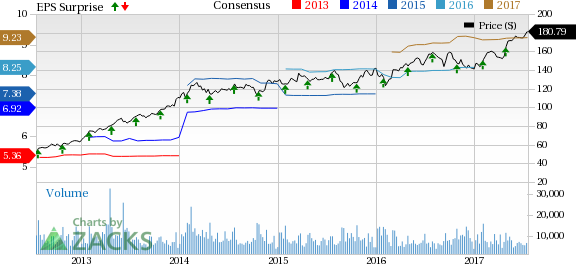

Last quarter, the company posted earnings of $2.08 per share, surpassing the Zacks Consensus Estimate by 3%. In fact, Thermo Fisher's earnings outpaced the Zacks Consensus Estimate in all of the past four quarters with an average beat of 2.3%. Let’s see how things are shaping up prior to this announcement.

Thermo Fisher Scientific Inc Price, Consensus and EPS Surprise

Thermo Fisher Scientific Inc Price, Consensus and EPS Surprise | Thermo Fisher Scientific Inc Quote

Why a Likely Positive Surprise?

Our proven model shows that Thermo Fisher is likely to beat on earnings because it has the right combination of two key ingredients.

Zacks ESP: Earnings ESP which represents the difference between the Most Accurate estimate and the Zacks Consensus Estimate, is +0.44%. This is a leading indicator of a likely positive earnings surprise. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Zacks Rank: Thermo Fisher currently carries a Zacks Rank #2 (Buy). Note that stocks with a Zacks Rank #1, 2 or 3 have a significantly higher chance of beating estimates. The Sell-rated stocks (#4 or 5) should never be considered going into an earnings announcement.

The combination of Thermo Fisher’s favorable Zacks Rank and positive ESP makes us confident in looking for an earnings beat this time around.

What is Driving the Better-Than-Expected Earnings?

The company’s focus to boost growth through implementation of strategies and strengthening of its product offerings is encouraging. These initiatives are likely to help it post solid results in the first quarter.

The company has already spent $750 million on research and development in 2016 and the same trend is expected through this year too. Some recently introduced noteworthy products include its new iCAP triple-quad mass spec system for clinical research in pharma Quality Assurance/ Quality Control (mass spectrometry and chromotography platforms); cloud-based application that connects electronic pipettes among individual users in the laboratories (within laboratory products); CarrierScan Assay, a microarray-based solution detecting over 6,000 genomic variations associated with 600 inherited diseases (within Genetic Sciences).

It also introduced new targeted assays for cancer research that run on Ion Torrent Next-Generation Sequencing instruments; new tests for autoimmune disease and drugs of abuse; and new Clariom Pico assays for more effective biomarker discovery. Notably last month, the US FDA had granted a premarket approval for the company’s Oncomine Dx Target Test. We expect all innovations and product launches to significantly contribute to the company’s top line in the second quarter itself.

The company’s aim to expand capabilities in the fast-growing Asia-Pacific zone as well as emerging markets should also lead to impressive results. Standout contributors in recent times are China, India and South Korea. With strategic investments to support key customer applications, Thermo Fisher hopes to maintain this bullish momentum throughout the rest of 2017.

Growth is likely to be seen in applied markets such as environmental and food safeties apart from life science. This apart, the company is currently betting on some key-focus areas with enormous opportunities. These are advancing precision medicine from mass spectrometry to targeted gene sequencing and structural biology.

The acquisition of FEI has already started generating synergies and largely contributing to the company’s analytical instruments portfolio from last quarter. It is also the highlight of the quarter to be reported.

Thermo Fisher anticipates realizing total synergies of approximately $80 million by the end of three years following the deal closure, with about $55 million of cost synergies and roughly $25 million of adjusted operating income benefits from revenue-related synergies. This should get reflected in second-quarter 2017 performance.

However, we are apprehensive about Thermo Fisher citing a foreign exchange headwind to the tune of $250 million on 2017 revenues (an impact of 1.5%) and 17 cents on adjusted EPS (around 2%). Also, an unfavorable macroeconomic condition continues to weigh heavily on Thermo Fisher’s stock. Plus, stiff competition continues to pose a threat to the stock’s value.

Stocks to Consider

Here are some companies you may consider as our model shows that they have the right combination of elements to come up with an earnings beat in the upcoming quarter:

Dextera Surgical Inc. DXTR has an Earnings ESP of +9.09% and a Zacks Rank #2. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Teleflex Incorporated TFX has an Earnings ESP of +1.06% and a Zacks Rank #2.

Stryker Corporation SYK has an Earnings ESP of +0.66% and a Zacks Rank #2.

5 Trades Could Profit "Big-League" from Trump Policies

If the stocks above spark your interest, wait until you look into companies primed to make substantial gains from Washington's changing course.

Today Zacks reveals 5 tickers that could benefit from new trends like streamlined drug approvals, tariffs, lower taxes, higher interest rates, and spending surges in defense and infrastructure. See these buy recommendations now >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Thermo Fisher Scientific Inc (TMO) : Free Stock Analysis Report

Teleflex Incorporated (TFX) : Free Stock Analysis Report

Dextera Surgical Inc. (DXTR) : Free Stock Analysis Report

Stryker Corporation (SYK) : Free Stock Analysis Report

To read this article on Zacks.com click here.