Should You Think About Buying Mediobanca Banca di Credito Finanziario S.p.A. (BIT:MB) Now?

Mediobanca Banca di Credito Finanziario S.p.A. (BIT:MB), operating in the financial services industry based in Italy, saw a decent share price growth in the teens level on the BIT over the last few months. With many analysts covering the mid-cap stock, we may expect any price-sensitive announcements have already been factored into the stock’s share price. But what if there is still an opportunity to buy? Let’s take a look at Mediobanca Banca di Credito Finanziario’s outlook and value based on the most recent financial data to see if the opportunity still exists.

View our latest analysis for Mediobanca Banca di Credito Finanziario

Is Mediobanca Banca di Credito Finanziario still cheap?

The stock seems fairly valued at the moment according to my relative valuation model. I’ve used the price-to-earnings ratio in this instance because there’s not enough visibility to forecast its cash flows. The stock’s ratio of 10.18x is currently trading slightly above its industry peers’ ratio of 8.58x, which means if you buy Mediobanca Banca di Credito Finanziario today, you’d be paying a relatively fair price for it. And if you believe Mediobanca Banca di Credito Finanziario should be trading in this range, then there isn’t really any room for the share price grow beyond what it’s currently trading. Is there another opportunity to buy low in the future? Since Mediobanca Banca di Credito Finanziario’s share price is quite volatile, we could potentially see it sink lower (or rise higher) in the future, giving us another chance to buy. This is based on its high beta, which is a good indicator for how much the stock moves relative to the rest of the market.

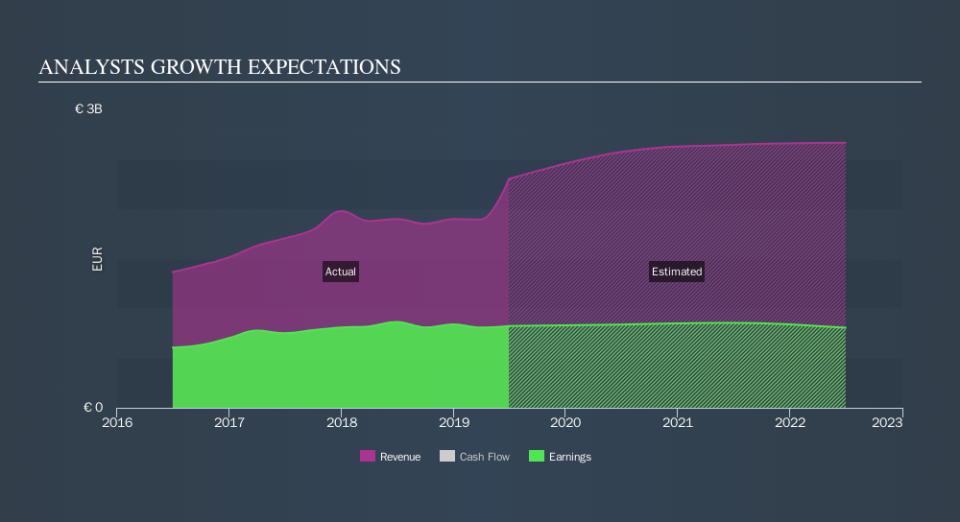

Can we expect growth from Mediobanca Banca di Credito Finanziario?

Investors looking for growth in their portfolio may want to consider the prospects of a company before buying its shares. Although value investors would argue that it’s the intrinsic value relative to the price that matter the most, a more compelling investment thesis would be high growth potential at a cheap price. Though in the case of Mediobanca Banca di Credito Finanziario, it is expected to deliver a negative earnings growth of -2.2%, which doesn’t help build up its investment thesis. It appears that risk of future uncertainty is high, at least in the near term.

What this means for you:

Are you a shareholder? MB seems fairly priced right now, but given the uncertainty from negative returns in the future, this could be the right time to de-risk your portfolio. Is your current exposure to the stock optimal for your total portfolio? And is the opportunity cost of holding a negative-outlook stock too high? Before you make a decision on MB, take a look at whether its fundamentals have changed.

Are you a potential investor? If you’ve been keeping an eye on MB for a while, now may not be the most advantageous time to buy, given it is trading around its fair value. The price seems to be trading at fair value, which means there’s less benefit from mispricing. In addition to this, the negative growth outlook increases the risk of holding the stock. However, there are also other important factors we haven’t considered today, which can help gel your views on MB should the price fluctuate below its true value.

Price is just the tip of the iceberg. Dig deeper into what truly matters – the fundamentals – before you make a decision on Mediobanca Banca di Credito Finanziario. You can find everything you need to know about Mediobanca Banca di Credito Finanziario in the latest infographic research report. If you are no longer interested in Mediobanca Banca di Credito Finanziario, you can use our free platform to see my list of over 50 other stocks with a high growth potential.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.