Tilray's (NASDAQ:TLRY) Earnings Need a Scratch Below the Surface

This article first appeared on Simply Wall St News.

Tilray, Inc.'s (NASDAQ: TLRY)story of 2021 has been the one of boom and bust (once again), as the stock repeated the performance from 2018 – albeit on a much smaller scale.

Although the stock gained on earnings results, digging deeper shows things are not what they seem.

Check out our latest analysis for Tilray

Second-quarter 2022 results:

EPS: US$0.013 (up from US$0.32 loss in 2Q 2021).

Revenue: US$155.2m (up 26% from 2Q 2021).

Net income: US$5.80m (up to US$98.6m from 2Q 2021).

Profit margin: 3.7% (up from a net loss in 2Q 2021).

Revenue missed analyst estimates by 9.3%, while earnings per share (EPS) exceeded analyst estimates. Over the next year, revenue is forecast to grow 19%, compared to a 16% growth forecast for the industry in the US.

Yet, looking deeper, the critics have highlighted the following:

Actual EBIDTA was negative without adjustments that removed about US$29M

Operating loss rose significantly Y/Y

Sales decreased over 10% Q/Q for cannabis and beverage sales

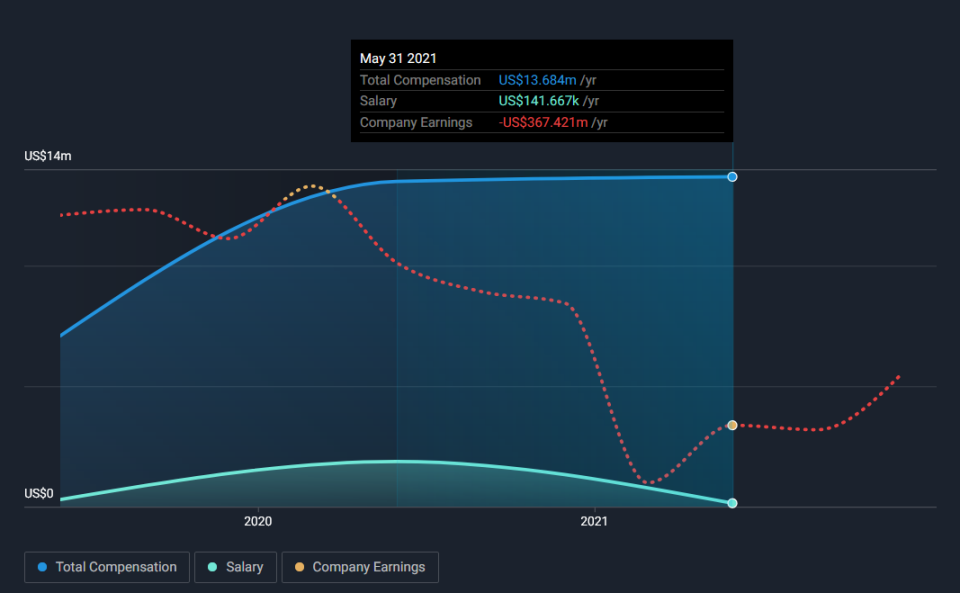

Furthermore, according to our data, CEO's compensation vastly exceeds the average for companies of similar size.

For 2021, the CEO's cash bonuses exceeded US$13m, with total compensation of nearly US$30m. This is around 20% of the quarterly revenues!

To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. Tilray expanded the number of shares on issue by 47% over the last year. That means its earnings are split among a greater number of shares.

To celebrate net income while ignoring dilution is like rejoicing because you have a single slice of a larger pizza, but ignoring the fact that the pizza is now cut into many more slices. You can see a chart of Tilray's EPS by clicking here.

A Look At The Impact Of Tilray's Dilution on Its Earnings Per Share (EPS).

Unfortunately, we don't have any visibility into its profits three years back, because we lack the data. And in focusing only on the last twelve months, we don't have a meaningful growth rate because it made a loss a year ago, too. One can observe that the dilution has a fairly profound effect on shareholder returns.

If Tilray's EPS can grow over time, that drastically improves the chances of the share price moving in the same direction. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

That might leave you wondering what analysts forecast in terms of future profitability. Lucky, you can click here to see an interactive graph depicting future profitability based on their estimates.

The Impact Of Unusual Items On Profit

On top of the dilution, we should also consider the US$77m impact of unusual items in the last year, which suppressed profit. While deductions due to unusual items are disappointing in the first instance, there is a silver lining.

When we analyzed most listed companies worldwide, we found that significant unusual items are often not repeated. And, after all, that's exactly what the accounting terminology implies. Tilray took a rather significant hit from unusual items through 2021. All else being equal, this would likely have the effect of making the statutory profit look worse than its underlying earnings power.

Our Take On Tilray's Profit Performance

To sum it all up, Tilray took a hit from unusual items, which pushed its profit down; without that, it would have made more money. Even so, the company has been careful in its approach to the latest earnings presentation, avoiding the painful points.

Unfortunately, the dilution means that shareholders now own a smaller proportion of the company (assuming they maintained the same number of shares). That will weigh on earnings per share, even if it is not reflected in net income.

Based on these factors, it's hard to tell if Tilray's profits are a reasonable reflection of its underlying profitability. In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. Every company has risks, and we've spotted 3 warning signs for Tilray you should know about.

In this article, we've looked at a number of factors that can impair the utility of profit numbers as a guide to a business. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity to indicate favorable business economics, while others like to "follow the money" and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity or this list of stocks that insiders are buying.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Stjepan Kalinic and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.