Top Rated LSE Stocks You Can Buy For Cheap

Stocks, such as Britvic, trading at a market price below their true values are considered to be undervalued. Investors can profit from the difference by investing in these stocks as the current market prices should eventually move towards their true values. If capital gains are what you’re after in your next investment, I’ve put together a list of undervalued stocks you may be interested in, based on the latest financial data from each company.

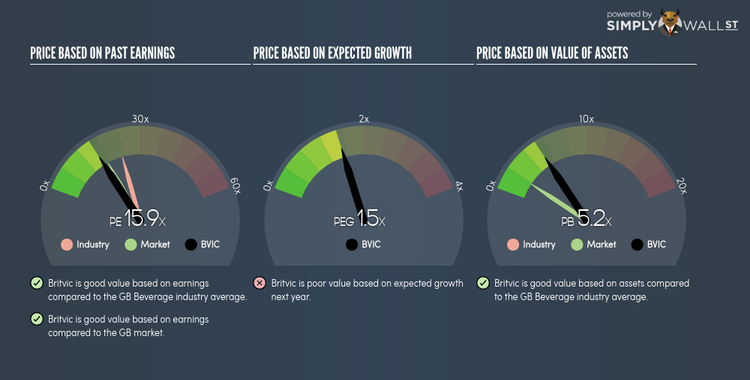

Britvic plc (LSE:BVIC)

Britvic plc, together with its subsidiaries, manufactures, markets, and distributes soft drinks primarily in the United Kingdom, the Republic of Ireland, France, and Brazil. Formed in 2005, and currently run by Simon Litherland, the company now has 4,672 employees and with the market cap of GBP £1.86B, it falls under the small-cap category.

BVIC’s stock is currently floating at around -26% beneath its actual value of £9.18, at the market price of £6.75, based on its expected future cash flows. This mismatch indicates a chance to invest in BVIC at a discounted price. Moreover, BVIC’s PE ratio stands at around 15.9x against its its beverage peer level of 23.2x, suggesting that relative to its peers, we can purchase BVIC’s shares for cheaper. BVIC also has a healthy balance sheet, with short-term assets covering liabilities in the near future as well as in the long run. The stock’s debt-to equity ratio of 200% has been diminishing over the past couple of years demonstrating BVIC’s ability to reduce its debt obligations year on year. Interested in Britvic? Find out more here.

3i Group plc (LSE:III)

3i Group plc is a private equity firm specializing in direct and fund of fund investments. Established in 1945, and now run by Simon Borrows, the company currently employs 241 people and with the company’s market capitalisation at GBP £8.95B, we can put it in the mid-cap category.

III’s stock is now trading at -41% less than its actual level of £15.58, at a price tag of £9.13, based on its expected future cash flows. This mismatch signals an opportunity to buy III shares at a discount. In terms of relative valuation, III’s PE ratio is currently around 7.3x relative to its capital markets peer level of 17x, implying that relative to its competitors, you can buy III for a cheaper price. III also has a healthy balance sheet, as near-term assets sufficiently cover liabilities in the near future as well as in the long run. Finally, its debt relative to equity is 9%, which has been falling for the past few years signalling its capacity to reduce its debt obligations year on year. Continue research on 3i Group here.

Epwin Group PLC (AIM:EPWN)

Epwin Group Plc manufactures and sells building products in the United Kingdom, rest of Europe, and internationally. Started in 1976, and currently run by Jonathan Bednall, the company size now stands at 2,592 people and with the company’s market cap sitting at GBP £111.19M, it falls under the small-cap category.

EPWN’s stock is currently trading at -55% below its actual value of £1.72, at a price of £0.78, according to my discounted cash flow model. This mismatch indicates a chance to invest in EPWN at a discounted price. Moreover, EPWN’s PE ratio stands at 6.4x while its building peer level trades at 12.4x, meaning that relative to its competitors, you can buy EPWN for a cheaper price. EPWN is also robust in terms of financial health, as short-term assets amply cover upcoming and long-term liabilities.

Dig deeper into Epwin Group here.

For more financially sound, undervalued companies to add to your portfolio, you can use our free platform to explore our interactive list of undervalued stocks.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.