Is Transocean a Buy?

After a painful late 2015 and early 2016 that saw crude oil prices fall to their lowest levels in the past decade, the oil industry has undergone a bit of a transformation. Gone are the "drill, baby, drill" days of $100 oil; instead, the most successful operators are the ones that have learned to practice fiscal discipline and live more within their cash flow.

No other segment of the industry has faced more hardship than offshore drillers. The past several years marked a low point in spending on offshore resource development, leading to a huge amount of consolidation, more than a few bankruptcies, and scrapping of old vessels by everyone who survived.

Of the survivors, Transocean (NYSE: RIG) has emerged stronger. Its fleet is newer and higher-spec, and over the past year, oil and gas producers have begun showing a willingness to spend money offshore again. That should bode well for Transocean's prospects. But is it a buy right now? Based on its book value, and what investors have typically been willing to pay, yes. But its cash flow multiple isn't nearly as cheap, and declining operating profits aren't exactly what investors want to see right now.

Image source: Getty Images.

Let's take a closer look at the company and its prospects and get to the bottom of whether it's worth buying today or not.

The book value argument says it's a buy, but...

Book value can be a really handy way to value a company. In short, it measures assets minus liabilities. Taking it a step further, tangible book value removes any intangibles (primarily goodwill) from the equation and focuses on hard assets like real property, cash, and in the case of an offshore driller, its drilling vessels.

In a general sense, if one is able to buy shares of a company for less than book value, it's cheap. The easiest way to determine if a stock sells for less than book value is the price-to-book-value ratio. Anything less than 1 means a stock trades for less than the book value of a company's assets. Here's Transocean:

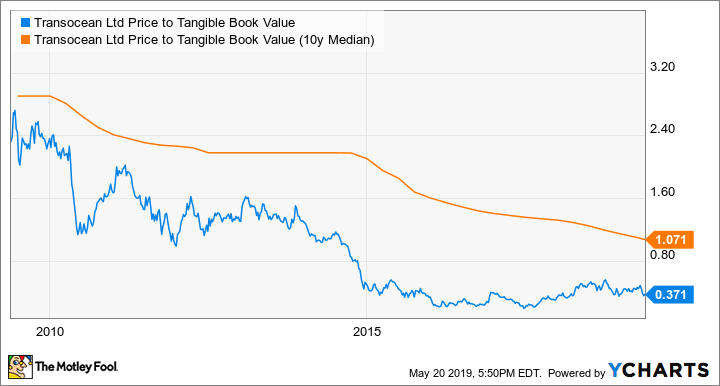

RIG Price to Tangible Book Value data by YCharts.

That's right -- its shares trade for 37% of book value at recent prices. In other words, if you bought every share at today's price, you'd buy the company for $0.37 on every dollar it values its assets for. Yet as you can also see, it's traded for a discount to book value for basically five years now, and the current valuation is sharply below the long-term median book value it has traded for.

So what gives? A couple of things. First off, book value for many offshore drillers, Transocean included, has been a bit of a moving number the past few years. Dozens of companies have had to scrap hundreds of vessels, resulting in billions of dollars of asset writedowns. For Transocean, its tangible book value peaked in 2017 above $15 billion as it was both scrapping old vessels while also adding a lot of new ones, then falling below $12 billion in 2018 as it continued to aggressively scrap uncompetitive vessels.

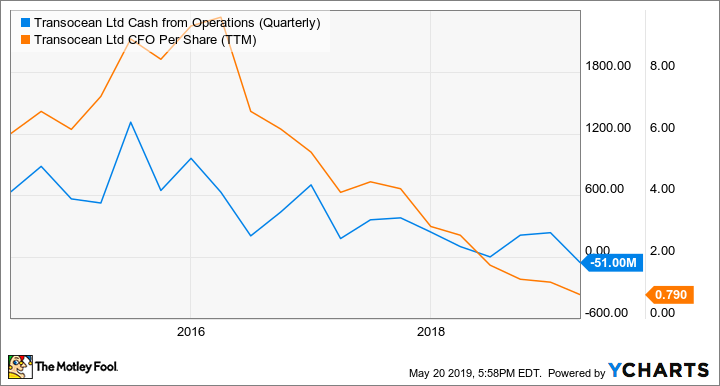

At the same time, the quality of its cash flow steadily deteriorated during the downturn:

RIG Cash from Operations (Quarterly) data by YCharts.

When you're a cash cow, investors will pay a premium to own a piece of the action. When cash flow dries up, the incentive to own the business goes out the window and book value becomes a footnote.

Transocean's cash flow has continued to diminish the past two years, even as it has removed more older vessels and expanded its high-spec drilling fleet:

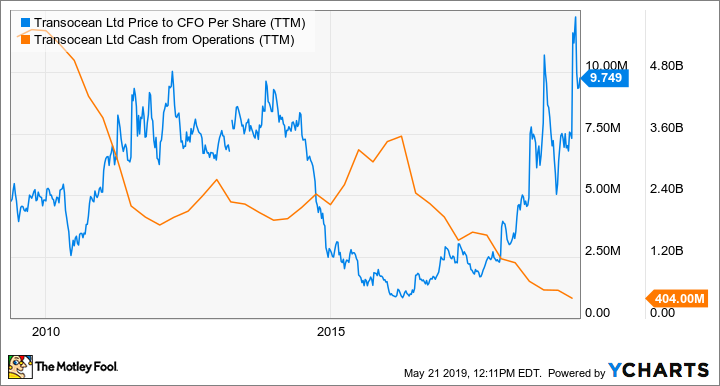

RIG Price to CFO Per Share (TTM) data by YCharts.

Shares now trade for nearly 10 times cash from operations. By this measure, Transocean's stock is now the most expensive it's been in a decade.

Expensive or cheap? It depends on what happens next

I'm sure it's infuriating for many investors when the analysis uncovers this dichotomy: The same stock assessed under two different measures is either expensive or cheap. The only way to determine which is most likely the correct measure is to project what happens going forward.

On the book value side, it looks like Transocean has largely finished clearing old, nonviable assets out of its fleet. That means less writing down of asset values, while still taking on a few new builds that will add to the company's book value. This trend is corresponding with a strengthening of demand for harsh-condition and ultra-deepwater drilling, the tier where Transocean has added the most new capacity to its fleet and should be able to leverage into higher operating results.

But in the near term, it's possible that the company's cash flow could feel a bit of a pinch. On the first quarter-earnings call, CFO Mark Mey said that reactivation costs related to its acquisition of Ocean Rig would be higher than initial estimates. These cash expenses will largely be treated as operating costs, not capital expenditures, and that will take a bite out of operating cash flow this year. Moreover, Transocean will incur operating expenses for these vessels it must cover before they commence drilling activities under new contracts.

However, the short-term pain is due to something that will generate long-term gain, as the company is putting these idle vessels back to work. That should make a marked improvement in cash flow, likely later in 2019 and early in 2020.

On balance, Transocean looks like a solid buy

Based on its asset valuation, strong balance sheet, and the trajectory I expect to see its cash flow take over the next year, my analysis is that Transocean is worth buying today. But this isn't a pure "cheap stock" value play, because the company's cash flow dipped into the negative in the first quarter, and it has work to do to continue turning those results around.

But with a long history of solid operating results even through the downturn, the best fleet in the industry, and a steady tightening of supply and ramping up of demand for its services, my expectation is investors who buy shares of Transocean at current prices should be rewarded over the next few years.

More From The Motley Fool

Jason Hall owns shares of Transocean. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.